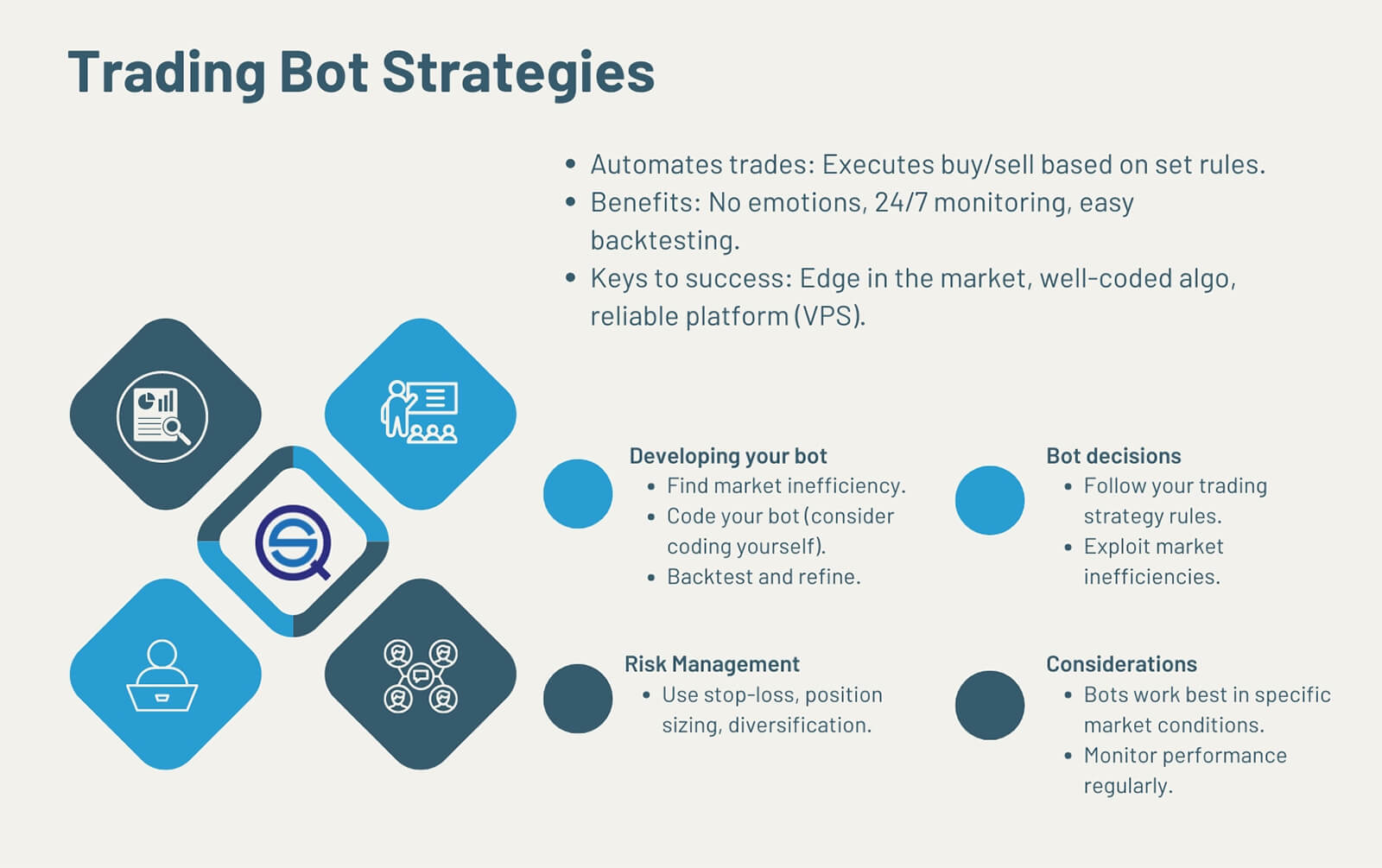

- Choose a programming language (Python is most common for beginners; Node.js, Go, or Rust for performance-critical bots)

- Connect to an exchange API (Binance, Bybit, Kraken, or a DEX aggregator like Jupiter on Solana)

- Define a trading strategy (RSI, moving average crossover, arbitrage, or AI-driven signals)

- Implement risk controls: stop-loss, position sizing, and maximum drawdown limits

- Backtest on historical data before running with real capital

- Deploy on a VPS server located near the exchange's data center to minimize latency

Building a basic bot costs between $10,000–$20,000. An AI-powered or high-frequency trading bot typically ranges from $40,000 to $50,000+, depending on complexity and required infrastructure.

Crypto markets don't sleep. A price move that takes three seconds to form can take a human trader thirty seconds to notice — and another ten to act on. That gap is where bots live. They execute without hesitation, follow rules without deviation, and scale across dozens of pairs simultaneously. For traders, that means capturing opportunities that would otherwise disappear. For developers and businesses, it means building systems where automation is a measurable competitive advantage.

This guide covers the full technical path: from architecture and language selection to strategy implementation, DEX sniper bots, AI signal systems, deployment, and realistic cost breakdowns — based on our engineering experience building production-grade trading bots.

How Crypto Trading Bots Work

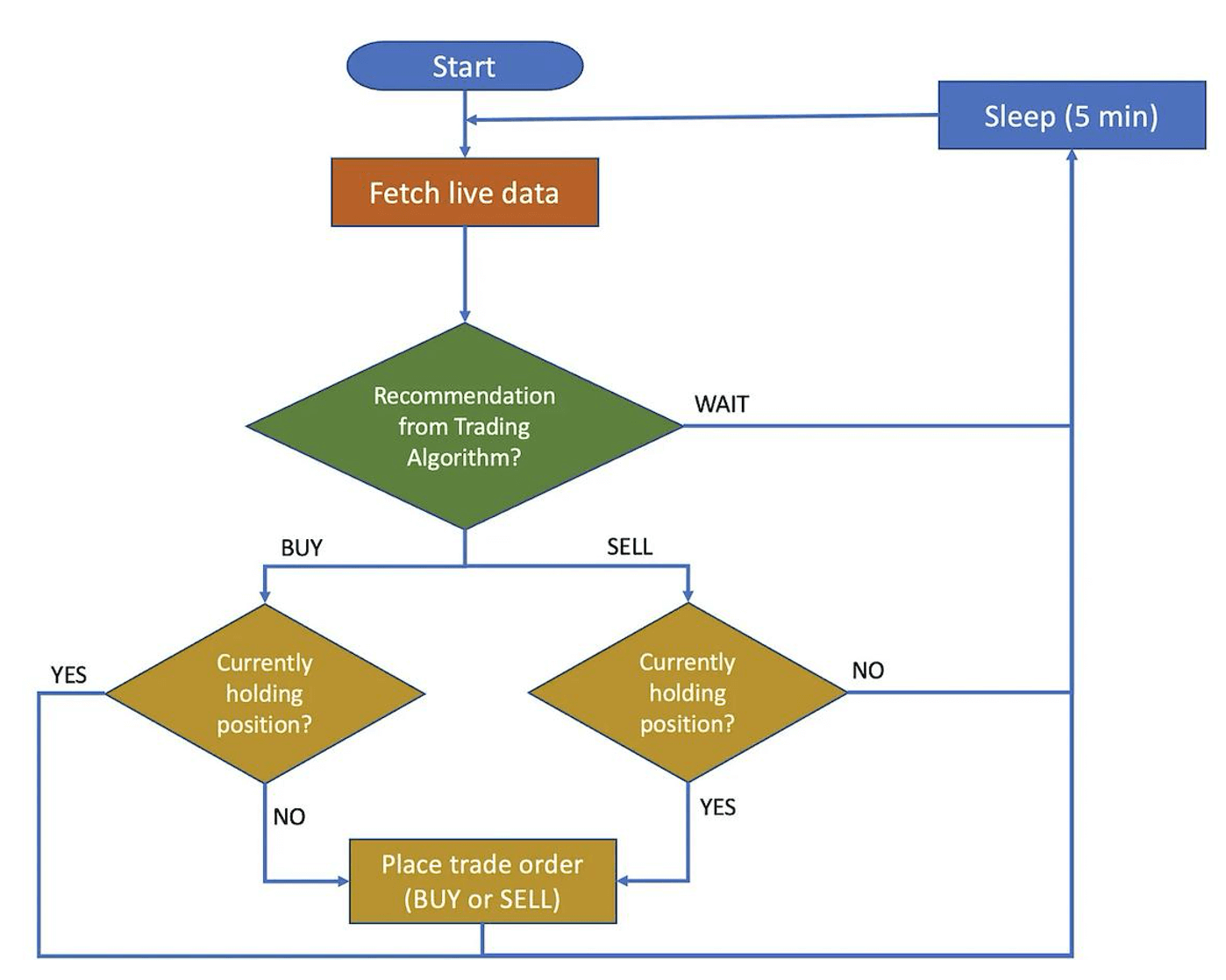

At the core, a crypto trading bot is a service that continuously polls or streams data from an exchange via its API, evaluates that data against a set of rules, and places orders when conditions are met. The exchange API is the gateway: the bot authenticates, receives market data (prices, order book, volume), and sends order instructions back.

Most bots operate in a tight loop. For example: if RSI drops below 30, send a market buy order; if price rises 5% above entry, send a limit sell. More advanced systems combine multiple indicators, on-chain data, or even live news feeds. The fundamental principle stays the same — the bot doesn't interpret, it executes the logic you've defined.

This matters because markets move 24/7. A volatility spike at 3 AM on a Sunday is indistinguishable to a bot from one at 2 PM on a Monday. It executes the same logic either way. No fatigue, no second-guessing, no deviation from the plan.

Key Features Every Trading Bot Must Have

No matter how complex the strategy, every production-grade bot is built on the same functional foundation. Missing any of these components turns the bot from a tool into a liability.

- Real-time data feed. The bot must receive live prices, order book depth, and volume with minimal delay. A data lag of even a few seconds renders most intraday strategies ineffective — the signal has already expired by the time the bot sees it.

- Order execution engine. Placing, modifying, and canceling buy/sell orders on the exchange quickly and reliably. This is the operational core of the bot — everything else feeds into it.

- Strategy module. The rule set that drives decisions. Whether it's a simple RSI trigger, a moving average crossover, or a multi-factor model with confidence thresholds, this module is where your trading logic lives.

- Risk controls. Stop-loss, take-profit, maximum position size, maximum daily drawdown. Without hard limits, a bug or a volatile market can drain an account faster than any manual trader could intervene.

- Backtesting engine. Before any real capital is involved, the strategy runs against historical data. If it couldn't survive the last six months, it won't survive tomorrow.

- Notification system. Alerts via email or push notifications — and particularly via Telegram trading bots, which have become the de-facto standard for real-time trade reporting. You always know what the bot is doing, even when you're not watching the screen.

The real constraint was the exchange: rate limits, account verification tier, and server ping. Rate limit issues we resolved by upgrading the account's verification level or reaching the required trading volume threshold — most exchanges accommodate this with a direct support request.

Ping is a different matter entirely: only a VPS geographically close to the exchange's data center meaningfully reduces it, and no amount of code optimization compensates for network latency.

Choosing the Right Tech Stack

Language selection for a trading bot is primarily a question of your team's existing skills and the bot's performance requirements. There is no universally "best" language — there are appropriate and inappropriate choices for specific use cases.

- Python is the default starting point for most teams. The ecosystem is mature: libraries like

pandas,NumPy,python-binance, andccxtdramatically reduce development time for standard CEX integrations. The trade-off is raw throughput — Python is not the right choice for high-frequency trading that requires sub-millisecond execution. - JavaScript / Node.js handles asynchronous I/O efficiently, which matters for bots that maintain multiple WebSocket connections simultaneously. It's also a natural fit if the bot includes a real-time web dashboard.

- Go delivers near-C performance with cleaner concurrency primitives than Python's threading model. Increasingly common for bots that need to process hundreds of signals per second without a heavy runtime.

- Rust is the performance ceiling — zero garbage collection, predictable memory layout, and compiler-enforced safety. The right choice for high-frequency or MEV-adjacent systems where microseconds matter. Higher learning curve and longer development time.

- C# / Java are the enterprise tier — used when the bot is part of a larger institutional platform with existing .NET or JVM infrastructure, compliance requirements, or multi-team development.

For DEX bots on Solana specifically, the ecosystem has standardized largely on TypeScript (for the Solana web3.js SDK) and Rust (for on-chain program interactions where latency is critical). Python-based DEX bots exist but face structural disadvantages in speed-sensitive scenarios like token sniping. If your starting point is a centralized exchange, our separate guide on creating a trading bot for Binance covers the full CEX API integration workflow in detail.

Building and Testing Your Strategy

The API connection is the easy part. Defining what the bot does once connected is the actual engineering challenge.

Standard entry points for strategy development:

- RSI (Relative Strength Index): Buy when RSI drops below 30 (oversold), sell when it crosses above 70 (overbought). Simple to implement, widely understood, and a reasonable starting point for testing the full bot pipeline end-to-end.

- Moving Average Crossovers: Buy when the short-term MA (e.g., 9-period) crosses above the long-term MA (e.g., 21-period); reverse on the opposite crossover. Effective in trending markets, generates false signals in ranging ones.

- Scalping: High-frequency, small-margin trades that capitalize on bid-ask spread or micro-volatility. Requires fast execution and low fees — not viable for manual trading but exactly what automated systems excel at.

Backtesting is non-negotiable. A strategy that looks profitable on a chart is not the same as a strategy that survives live execution with slippage, fees, and latency. Run your logic against at least 6–12 months of historical data with realistic transaction cost assumptions. Walk-forward validation — testing on sequential out-of-sample periods — is more reliable than a single train/test split, which can introduce look-ahead bias.

After backtesting passes, don't scale immediately. Paper trade first (simulate orders without real capital), then go live with position sizes small enough that the first 50 trades are effectively paid tuition. Only after consistent behavior in live conditions does scaling make sense.

DEX Sniper Bots and New Token Automation

A category of bots that operates on fundamentally different logic from indicator-based systems: DEX sniper bots. Instead of reacting to price movements, these bots react to events — specifically, the appearance of new liquidity pools or token listings on decentralized exchanges.

The core logic: the bot maintains a local database of all tokens available on the aggregator. On each cycle, it compares the live token list against the database. Any token that doesn't exist in the local store is new — and triggers an immediate buy order. The sell condition is defined as a fixed percentage gain from the purchase price.

Two infrastructure details that determine whether the bot works at all in practice:

- Gas reserve management. The bot must hold back a fixed percentage of the wallet balance to cover transaction fees. In Solana-based implementations, reserving 10% of available funds for gas is a practical baseline. Below a minimum working balance (approximately $15 for Solana), the bot cannot execute transactions after accounting for network fees.

- Graceful stop logic. When the bot receives a stop command, only the buy script should halt — token tracking and database updates should continue. This allows the bot to restart cleanly without re-seeding the entire token database from scratch, which would cause it to treat all existing tokens as "new" on the next run.

Arbitrage Bots: CEX↔DEX and Multi-DEX Architecture

Arbitrage bots exploit price discrepancies across markets. The concept is simple; the execution is not. Three categories of arbitrage are common in crypto bot development:

- CEX↔CEX arbitrage: Buy on Exchange A where the price is lower, sell on Exchange B where it's higher. Speed and simultaneous execution are critical — the window closes in seconds.

- CEX↔DEX arbitrage: Monitor price discrepancies between a centralized exchange (e.g., Bybit) and an on-chain protocol. Adds gas cost and on-chain transaction finality to the equation.

- Atomic / multi-DEX arbitrage: Execute a full cycle across multiple decentralized exchanges within a single transaction block. Eliminates counterparty risk but requires smart contract interaction and MEV-awareness.

From our engineering experience building a CEX↔DEX arbitrage system, three technical challenges consistently determine profitability in production:

| Challenge | Problem | Technical Solution |

| Gas price | Slow transaction confirmation loses the arbitrage window; low gas = low miner priority | Dynamic gas multiplier: increase priority fee when an arbitrage opportunity is detected, tuned per network congestion |

| Slippage | Actual execution price deviates from calculated profit due to order book depth | Classify tokens by liquidity tier (high/medium/low); calculate both "theoretical arbitrage price" and "realistic price including slippage" before execution |

| Pool liquidity | Large orders move the price before or during execution | Cap position size relative to pool depth; optionally integrate AMM or MEV logic for larger positions |

Deployment and Risk Management

Going live is the beginning of the actual work, not the end of development. Deployment introduces a category of risks that no backtest can replicate: real exchange behavior under load, network interruptions, unexpected order fills, and your own psychology under drawdown.

Start with minimal capital. Run the bot with position sizes small enough that the first 30–50 trades are effectively a paid audit of live behavior. Does execution timing match the backtest? Does the bot handle partial fills correctly? Does it recover cleanly after a WebSocket disconnect? Only stable behavior at small scale justifies scaling capital.

Essential infrastructure controls:

- Stop-loss at the position level and the account level. A per-trade stop-loss limits individual losses; a maximum daily drawdown limit stops the bot entirely if cumulative losses exceed a threshold. Both are required.

- Parallel paper trading log. Run a simulated version of the bot alongside the live version. Divergence between the two reveals execution issues that wouldn't show up in metrics alone.

- VPS near the exchange data center. Home internet connections introduce variable latency. A VPS in the same region as the exchange's matching engine reduces execution variance significantly — especially relevant for scalping and sniper bots.

- Multi-provider resilience. Crypto data APIs and exchange APIs fail without warning. In our experience, providers can be intermittently unavailable for hours or, in some cases, weeks. Architecting the bot with a fallback provider array — where all sources share the same data contract — lets the system switch automatically without touching business logic. Single-provider dependencies are a reliability risk, not just a technical inconvenience. The same principle applies to your exchange connectivity: review crypto exchange security architecture to understand what redundancy looks like at the infrastructure level.

A failure mode that's common even among experienced developers: manually overriding the bot after a sequence of losing trades. The reasoning is usually "I know the market is different right now." But that decision destroys the consistency that makes automation valuable. If the bot's logic is wrong, fix the logic — don't bypass it. If the logic is right, trust it through the drawdown. The only correct response to a bot that's losing is to either run the numbers and update the strategy, or pause it entirely and re-evaluate. Selective overrides produce the worst of both worlds: human emotional timing combined with algorithm execution speed.

Advanced Features: AI-Driven Signal Systems

Beyond indicator-based strategies, a growing category of production bots integrates machine learning and LLM-based analysis for signal generation. These systems don't replace traditional bots — they extend them with the ability to process unstructured signals (news, regulatory events, social sentiment) that rule-based systems can't handle.

In one of our projects, a client initially requested "an AI bot for trading signals." Scoping the architecture quickly revealed why a single-model approach wouldn't hold up — and why building a proper LLM-powered system requires combining multiple components rather than relying on a single model:

- Pure LLM systems can't learn between sessions — model weights are frozen. Every decision starts from zero.

- Pure ML models handle structured numerical features well but are blind to unstructured context: a regulatory announcement, a hack disclosure, or a macro event.

- Rule-based systems don't adapt when market regime changes.

The architecture that addressed all three: a hybrid system combining six specialized LLM agents (Technical, Sentiment, On-Chain, News, Macro, Synthesizer) with an XGBoost direction predictor, a regime classifier, and a vector memory layer built on pgvector for historical pattern retrieval. The Synthesizer agent receives outputs from all five analytical agents, ML predictions, and retrieved historical analogs, then produces a final weighted signal with full reasoning.

| Component | Role | Technology |

| Direction Predictor | Predicts 24h price direction (up/down/neutral) on 40–60 structured features | XGBoost with walk-forward validation |

| Regime Classifier | Labels current market state: trending up/down, ranging, high volatility | Random Forest on price/volume features |

| Vector Memory | Retrieves similar historical market configurations before each decision | pgvector on PostgreSQL 16 + TimescaleDB |

| LLM Agents | Processes unstructured signals: news, sentiment, on-chain behavior, macro context | Claude API (Sonnet for analysis, Haiku for classification) |

| Learning Loop | Evaluates past signals against realized price moves; reweights agent contributions weekly | Celery jobs + PostgreSQL audit trail |

Walk-forward validation gives lower numbers precisely because it accurately simulates live deployment: each model version is trained on data available at prediction time, and tested only on data it hasn't seen.

The system also needs 25–30% of ongoing maintenance allocated to data quality issues — provider API changes, exchange outages, and scoring model revisions from sentiment data sources are routine, not exceptional.

Popular Strategies: Scalping, Arbitrage, and Momentum

Strategy selection defines the bot's behavior, risk profile, and infrastructure requirements. No single strategy works indefinitely — market conditions shift, edges get arbitraged away, and volatility regimes change. Here's the operational reality of the three most common approaches:

- Scalping. Dozens to hundreds of trades per day, each targeting a small margin. Risk per trade is low; aggregate exposure accumulates through volume. Requires fast execution, low fees (fee tier matters significantly at this frequency), and reliable order fills. Not viable to execute manually — exactly the use case automation was built for. Best suited for liquid pairs with tight spreads.

- Arbitrage. Exploits price gaps between markets. Simple in theory, constrained in practice by fees, latency, slippage, and the speed of competing bots targeting the same opportunity. Works best with significant capital and infrastructure optimized for execution speed. Margins on CEX arbitrage have compressed substantially as the strategy has become more widely automated.

- Momentum / Trend Following. Enters positions early in a directional move, exits near the peak. Higher per-trade profit potential than scalping, but higher exposure to sudden reversals. Bots add value here primarily by enforcing the exit discipline that human traders consistently fail to maintain. A related category worth considering is copy trading platforms, where the bot mirrors the positions of verified successful traders rather than executing its own signal logic.

In practice, many production deployments run multiple bots simultaneously — each operating its own strategy on a subset of the total capital. A scalper handles one set of pairs; an arbitrage bot monitors cross-exchange discrepancies; a momentum bot takes longer-duration trend positions. This portfolio approach diversifies strategy risk without requiring a single bot to do everything.

Cost of Development and Factors That Influence Price

Development cost for a crypto trading bot spans a wide range because "trading bot" covers fundamentally different products at different ends of the spectrum. For a detailed cost breakdown by component and team type, see our dedicated crypto trading bot cost guide for 2026.

- $10,000–$20,000: A functional single-exchange bot with a defined strategy, basic risk controls, Telegram notifications, and a simple management interface. Appropriate for testing a specific trading thesis or automating a strategy that's already proven manually. Python-based, small team, 4–8 weeks.

- $25,000–$40,000: Multi-exchange support, multiple simultaneous strategies, custom backtesting engine, web dashboard with real-time P&L, and basic portfolio management. Suitable for a trader scaling from personal use to managing third-party capital.

- $40,000–$80,000+: AI-driven signal generation, high-frequency execution architecture, on-chain DEX integration, compliance features, or a SaaS platform serving multiple traders. Rust or Go backend, cloud infrastructure, dedicated DevOps.

Estimate 15–25% of the initial development cost annually for maintenance on a production bot. This is not optional — an unmaintained bot will break, usually at the worst possible time (high volatility, important market event) when the underlying exchange has made a breaking API change.

Stack selection also drives cost significantly. A Python prototype built by a small team is faster and cheaper to ship. An enterprise-grade system in Rust with cloud deployment, custom dashboards, multi-region failover, and compliance logging is a fundamentally different budget category.

Wide Functionality vs. Focused Specialization

Multi-functional bots and specialized bots represent different risk/reward tradeoffs in development and operation, not a hierarchy where one is objectively better.

A multi-functional bot — one that handles multiple strategies, connects to several exchanges, and includes advanced analytics — offers flexibility. The trade-off is complexity: more code surface area means more potential failure points, longer debugging cycles, and higher maintenance overhead. When something breaks during a volatile market, a complex system takes longer to diagnose.

A specialized bot does one job with maximum reliability. A scalper that only scales, or a DEX sniper that only snipes, is easier to reason about, faster to audit, and simpler to maintain. The limitation is coverage — a portfolio of strategies requires running multiple bots rather than one.

Many experienced operations end up running several narrow bots in parallel, each handling its domain, rather than investing in one comprehensive system. This architecture also allows independent failure: if the arbitrage bot goes down, the scalper continues operating.

Conclusion

A crypto trading bot is infrastructure, not a product that runs itself. Its value is determined by the quality of the strategy it executes, the reliability of its execution, and the discipline with which you manage it. A well-built bot with a marginal strategy loses money efficiently. A well-built bot with a validated strategy scales returns that no manual trader could match in speed or consistency.

The path from idea to production: define your strategy in precise, testable rules → build and backtest → paper trade → live trade at minimal size → scale. Each step is a filter. Most strategies don't survive all five. The ones that do are worth building infrastructure around. If you're evaluating more advanced exchange-level architecture for your platform — including order matching at scale — our matching engine technical guide covers the engineering fundamentals in depth.

FAQ

What programming language is best for building a crypto trading bot?

Python is the most practical starting point for most teams — mature libraries, fast development, and wide documentation. For performance-critical bots (high-frequency trading, DEX snipers), Go or Rust are better choices due to faster execution and lower memory overhead. Node.js is a solid option if the bot requires real-time WebSocket handling or a built-in web interface. The key factor is what your team already knows — rewriting a working Python bot in Rust makes sense only after the strategy has proven itself profitable.

How much does it cost to build a crypto trading bot?

A basic single-exchange bot with a defined strategy and risk controls costs $10,000–$20,000. A multi-exchange bot with a web dashboard and multiple strategies runs $25,000–$40,000. An AI-powered or high-frequency system with custom infrastructure typically starts at $40,000 and can reach $80,000+. Add 15–25% of the initial cost annually for maintenance — exchange API changes and security updates are ongoing requirements, not optional extras.

What is backtesting and why is it necessary before deploying a bot?

Backtesting runs your strategy logic against historical price data to evaluate how it would have performed. It's necessary because a strategy that looks good on a chart often fails when you account for transaction fees, slippage, and execution timing. Walk-forward validation — testing on sequential out-of-sample data periods — gives more reliable results than a single train/test split, which can produce misleadingly high accuracy through look-ahead bias. Treat any backtest showing 70%+ win rate with significant skepticism until validated with this method.

Can a trading bot work on decentralized exchanges (DEX)?

Yes, and DEX bots have unique architecture requirements compared to CEX bots. Instead of REST/WebSocket API calls, they interact with on-chain smart contracts and liquidity pools. DEX sniper bots track new token listings and execute within seconds of a new pool appearing. Arbitrage bots exploit price gaps between DEX protocols. The main technical challenges are gas cost management, slippage from pool depth, and transaction finality time — all of which must be modeled precisely for the bot to be profitable rather than just fast.

What are the main risks of running an automated crypto trading bot?

The primary technical risks are API changes that break execution silently, network interruptions during open positions, and bugs in order sizing logic that can rapidly drain capital. The primary strategic risk is overfitting: a strategy tuned too precisely on historical data fails on live markets. Operationally, the most common mistake is manually overriding the bot after a drawdown — this destroys execution consistency and typically produces worse outcomes than letting the bot run the defined strategy through its natural variance.

What is a market-making bot and when does it make sense to build one?

A market-making bot provides liquidity by continuously placing both buy and sell orders around the current market price, profiting from the bid-ask spread. It requires significant capital, precise programming to manage inventory risk, and robust controls to survive volatility spikes that can wipe out spread profits. Market-making makes economic sense for teams operating at high volume on liquid pairs, or as a service to exchange operators who need tighter spreads. It's not a strategy for small capital — the edge is thin and competition from institutional market makers is intense.