Most traders who explore crypto arbitrage hit the same wall: by the time they spot a price gap between two exchanges and click through to execute, the spread is gone. The market doesn't wait. That's the entire case for automation — not as a nice-to-have, but as a hard prerequisite for this strategy to work at all.

This guide covers how to build a crypto arbitrage bot in 2025 — not just the concept, but the actual engineering decisions: which architecture fits which strategy, where bots fail in production, how to handle slippage and API rate limits, and what it realistically costs to build something that works. We draw on direct project experience across CEX, DEX, and hybrid arbitrage systems.

Whether you're a solo developer validating a strategy or a startup building a SaaS trading product, the decisions you make at the architecture stage determine whether you ship something profitable or something that looks good in backtesting and bleeds money in production.

What Is a Crypto Arbitrage Bot?

At its core, a crypto arbitrage bot is software that does one thing better than any human: it watches prices continuously and reacts without hesitation. Arbitrage itself is simple — buy a coin where it's cheaper, sell it where it's more expensive, pocket the spread. The hard part is speed. By the time a trader manually executes across two exchanges, the opportunity is typically gone.Bots solve this by connecting directly to exchange APIs, pulling real-time order book data, and firing trades the moment a profitable spread clears the fee threshold. No hesitation, no emotion, no second-guessing.

For businesses, the arbitrage bot isn't just a trading utility. It's the core engine for P2P trading platforms, SaaS tools for professional traders, and white-label products that startups can launch without building a full exchange. The bot is both the technology and the product.

How Do Crypto Arbitrage Bots Work?

Strip away the abstraction and a crypto arbitrage bot runs a tight loop: pull price data from exchange APIs, compare order books across markets, check whether the visible spread covers trading fees and execution costs, and fire two orders simultaneously if the math clears.The simplest version — inter-exchange arbitrage — buys an asset on the exchange where it's cheaper and sells on the exchange where it's priced higher. Triangular arbitrage is more complex: the bot chains three currency conversions within a single platform or protocol, exploiting pricing inefficiencies across pairs rather than platforms. Funding rate arbitrage opens simultaneous long and short positions on the same asset across different perpetual futures markets to capture rate differentials. Time arbitrage exploits the latency difference in price update speeds between exchanges.

The common thread across all these strategies: the bot doesn't sleep, doesn't hesitate, and doesn't miss a price update. In a game where execution speed is measured in milliseconds, that consistency is the entire edge.

How to Develop a Crypto Arbitrage Bot: Key Steps

Building a crypto arbitrage bot isn't primarily a coding challenge — it's an architecture challenge. The teams that ship profitable bots start by locking in three decisions before writing any code: which arbitrage strategy they're targeting, which exchanges they'll connect to, and what their infrastructure looks like. Every technical decision downstream follows from those three.

Step 1: Define Your Arbitrage Strategy

Strategy choice isn't just a trading question — it determines your entire technical stack. A bot designed for inter-exchange arbitrage between two CEXs looks completely different from one built for triangular arbitrage on a single DEX protocol, or for DEX sniper execution on new pool listings.Lock in the strategy first. Then design the system around its specific latency requirements, capital flow, and risk profile.

Step 2: Choose Your Architecture Model

Beyond strategy, you need to choose your bot's income model. This determines complexity, capital requirements, and potential ceiling.In one of our projects — a bot designed for cross-chain arbitrage between a centralized exchange and a THORChain-based DEX — the initial spread calculations looked consistently profitable on paper. In practice, three cost layers destroyed those margins before a single trade closed.

1. Gas price competition. To guarantee execution speed on the DEX side, the bot had to submit transactions with above-average gas fees — effectively bidding against other bots for block inclusion priority. This cost isn't fixed; it spikes during volatile periods, exactly when spreads look most attractive.

2. Liquidity-adjusted slippage. We categorized all monitored assets into three tiers — high, medium, and low liquidity — and built a dual-price model into the decision logic. Each opportunity was evaluated at two prices: the nominal arbitrage price (visible on the order book) and the realistic execution price (adjusted for expected slippage given current pool depth). Only opportunities where both prices showed profit cleared the execution threshold.

3. Pre-positioning cost. Cross-platform arbitrage requires asset balances pre-positioned on both sides. Dynamic rebalancing between CEX and DEX adds latency and withdrawal fees that are invisible in spread analysis but very visible in P&L reports. After full cost accounting, pure CEX↔DEX strategies showed lower net profitability than intra-platform strategies — despite appearing more attractive at the surface level.

| Architecture | Income Source | Key Risk | Technical Complexity | Best For |

|---|---|---|---|---|

| Standard Arbitrage Bot | Spread difference only | Transfer latency, exchange rate limits | Low–Medium | MVP, personal trading, SaaS entry-level |

| Arbitrage Bot + AMM | Spread + LP fees + portfolio rebalancing | Impermanent loss on volatile pairs | Medium–High | DeFi-focused platforms, Solana/ETH ecosystems |

| Arbitrage Bot + AMM + MEV | Spread + LP fees + mempool value extraction | Regulatory exposure, high infrastructure cost | Very High | Institutional operations, high-capital strategies |

| DEX Sniper Bot | Early entry on new pool listings | API rate limits, ping latency, rug pull risk | Medium | New token launch strategies, Solana ecosystem |

When Standard Arbitrage Isn't Enough: AMM and MEV Integration

A standard arbitrage bot has one income stream: the spread. Integrating with AMM liquidity pools opens a second: trading fees earned as a liquidity provider from the same capital base.The AMM+MEV combination is the highest-ceiling architecture, but also the most technically and legally complex. MEV strategies involve capturing value from transaction ordering in the mempool — front-running or back-running user transactions. On Ethereum this is an established practice; on Solana the mechanics differ due to the fee market structure. Verify the regulatory position in your jurisdiction before building MEV components. Our recommendation for most projects: start with intra-platform arbitrage or Arbitrage + AMM on a single chain. CEX↔DEX strategies are seductive on paper but consistently underperform when all costs are modeled correctly.

Choosing the Right Exchanges for Your Crypto Arbitrage Bot

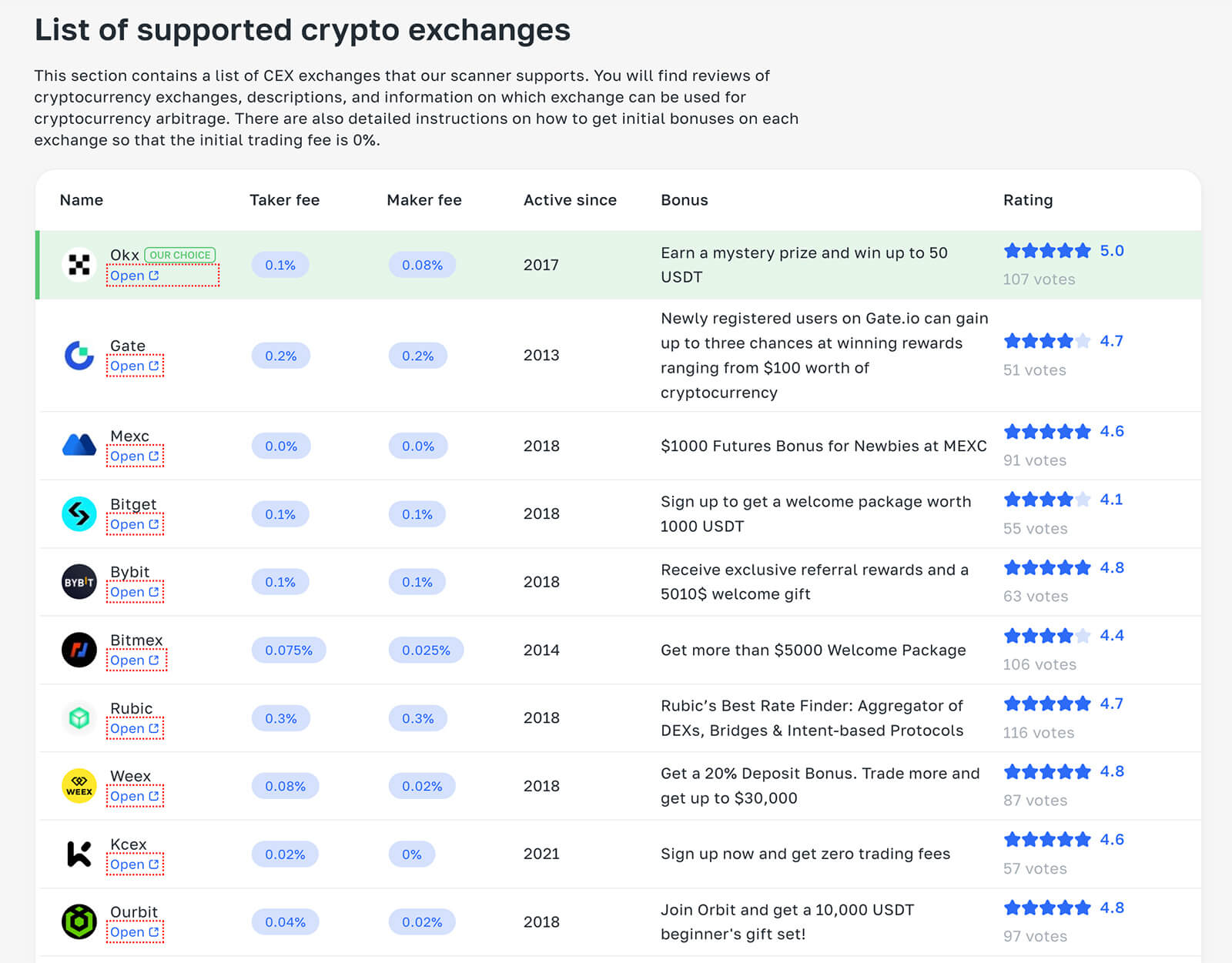

A crypto arbitrage bot is only as smart as the exchanges it connects to. You can write the cleanest code in the world, but if the platforms you're pulling data from are slow, illiquid, or full of restrictions, profits disappear before the trade closes.Start with jurisdiction. Binance is the global volume leader but operates under significant restrictions in the US. Kraken and Coinbase carry regulatory trust and solid API infrastructure but charge higher fees. OKX and KuCoin offer competitive spreads and deeper DEX connectivity. Smaller regional exchanges show attractive spreads on paper but carry counterparty risk and thin order books that move against you on execution.

Three API parameters determine whether an exchange is worth integrating:

- Rate limits. How many API calls per second does the exchange allow? Arbitrage bots are high-frequency by nature. If limits are too low, you miss windows. Hit them repeatedly and the exchange throttles or bans your key.

- WebSocket support. REST polling adds latency on every cycle. Exchanges with WebSocket streams for order book updates enable event-driven architecture — the bot reacts to price changes instead of asking for them on a timer.

- Order book depth. Thin books look profitable at the top but move against you on execution. Always evaluate spreads at your actual trade size, not at best bid/ask.

Most production teams settle on a core of 3–5 CEXs (Binance, OKX, KuCoin, Kraken) plus 1–2 DEXs (Uniswap on Ethereum, Raydium on Solana) for cross-market spread detection. More exchanges means more spread opportunities — but also more servers, more API keys, more failure points, and more compliance surface area.

Programming Language and Infrastructure for Your Crypto Arbitrage Bot

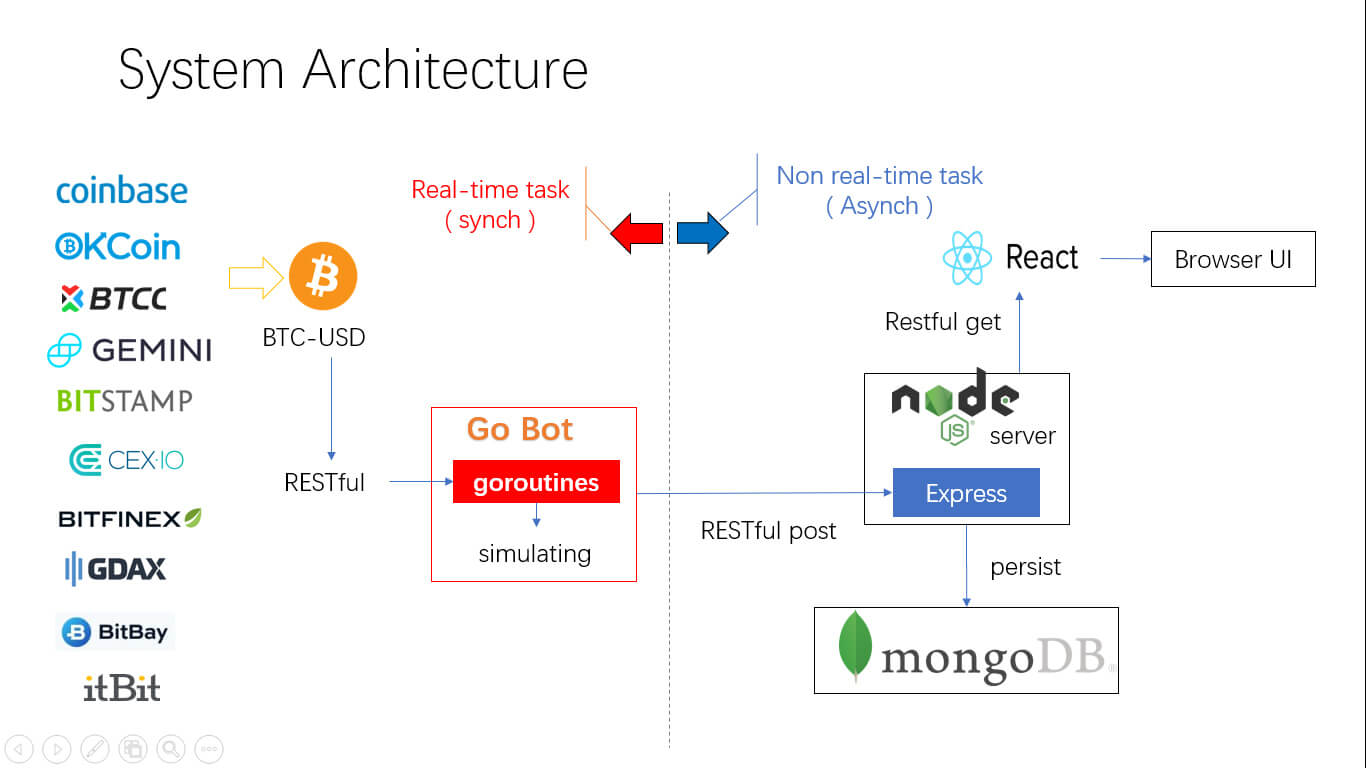

Here's the thing about building a crypto arbitrage bot: the language debate is real but often overstated. Here's the actual tradeoff matrix:Python is the standard choice for teams that need to move fast. The ecosystem is deep: ccxt handles multi-exchange API abstraction, asyncio handles concurrent API calls, pandas handles data analysis. Python's weakness is raw execution speed — but for most inter-exchange arbitrage strategies, network latency to the exchange dominates over local processing time anyway.

Rust or C++ make sense when you're running intra-chain strategies where execution speed is measured in microseconds and you're competing directly against other bots on the same chain. On Solana, where block times are 400ms and transaction ordering matters, a Rust-based execution engine provides a measurable edge over a Python equivalent.

Hybrid architectures are common in mature systems: Python for strategy logic, data processing, and dashboard backend; Rust or Go for the execution layer that fires actual orders. The strategy layer needs to be correct. The execution layer needs to be both fast and correct.

Infrastructure: The Latency Problem You Can't Code Around

Server geography is the infrastructure decision that most teams make wrong once and never repeat. From one of our production builds — a DEX sniper bot designed to execute in the first seconds of a new liquidity pool listing on Solana:Rate limits are negotiable. In early testing, the bot hit throttling thresholds during high-activity periods and missed entry windows on new listings. Resolution path: escalate API access tier with the exchange. This is achievable either through higher verification level or by demonstrating sufficient trading volume. Both paths worked across different integrations.

Ping latency is not negotiable. Network round-trip time between your server and the exchange's matching engine is fixed by physical infrastructure. No amount of code optimization changes it. The only mitigation is co-location: deploying in the same data center region as the exchange's infrastructure.

For US-based deployments targeting major CEXs, AWS us-east-1 and Google Cloud us-central1 consistently deliver the lowest latency profiles. The performance difference between a 200ms and 800ms order execution time was the difference between profitable entries and failed transactions on time-sensitive opportunities — a 4x latency gap that produced near-zero conversion on new pool listings.

Cloud vs. dedicated is a secondary question. Cloud wins on flexibility, managed uptime, and easy scaling — correct for most arbitrage products at launch. Dedicated servers win on latency consistency when you've validated that the exchange's data center is co-located and you need sub-millisecond predictability. Don't pay for dedicated hardware until you've confirmed the latency improvement is measurable in your specific strategy.

Securing Your Crypto Arbitrage Bot

In crypto, profits vanish the second security slips. A crypto arbitrage bot connects to real exchanges, handles API keys, and moves actual money — if attackers find a way in, they won't just break your code, they'll drain your accounts.The non-negotiable baseline:

- API key permissions. Every exchange key used by the bot must be scoped to trading-only — no withdrawal permissions, ever. A compromised trading key loses you open positions. A compromised withdrawal key loses you everything.

- Key storage. Never in plaintext, never in environment variables that get logged. Use a secrets manager (AWS Secrets Manager, HashiCorp Vault) or at minimum encrypted storage with keys isolated from the application codebase.

- 2FA on every account. Non-negotiable baseline. Hardware keys (YubiKey) are stronger than authenticator apps for accounts managing significant capital.

- Cold storage separation. Keep the majority of assets offline. The bot's operational wallet holds only the capital needed for active trading — losing a hot wallet to a breach shouldn't mean losing the business.

- Dependency audits. Third-party libraries in your bot's stack are an attack surface. Compromised npm or PyPI packages have drained crypto projects before. Audit your dependencies on a regular schedule.

For projects above $50K in managed capital, budget for a dedicated security audit before going live — specifically white-hat penetration testing on the API integration layer, not just a generic code review.

Building the Control Panel for Your Crypto Arbitrage Bot

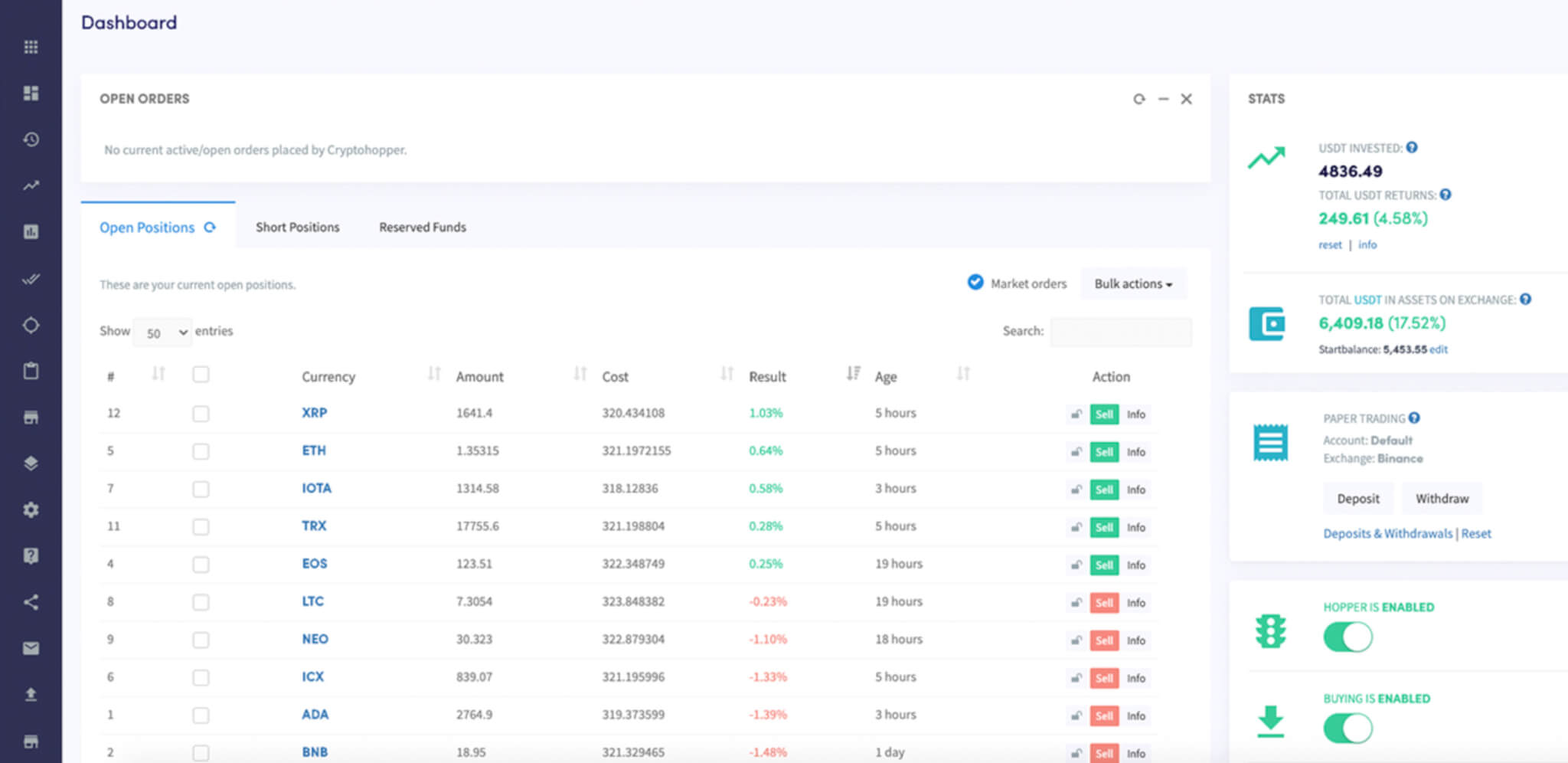

Behind every production-grade crypto arbitrage bot is a control panel that does more than display charts. It's the command center where traders see what the crypto bot is doing, verify it's working correctly, and intervene when they need to.Five components every production dashboard needs:

- Live trade feed. Real-time log of every order: pair, exchange, side, size, status, execution price vs. expected price. Your primary debugging tool and your traders' primary trust signal.

- Fee-adjusted P&L tracking. Gross spread captured, fees paid (trading fees, gas, withdrawal), net profit per trade and cumulative. Without fee adjustment, the dashboard lies to you about whether the bot is profitable.

- Exchange connection health. Status indicators for every API connection — latency and error rate in real time. When a connection degrades, you need to know before the bot starts missing trades.

- Strategy controls with emergency stop. Adjust spread thresholds, position size limits, and active pairs without redeploying code. Emergency stop that halts all trading in one click — this is the most important button on the dashboard.

- Backtesting interface. Historical performance simulation against real exchange data — for strategy validation before going live and for diagnosing performance drops after market conditions shift.

For the frontend stack, the build-vs-buy decision comes down to timeline. Frameworks like Start Bootstrap or Creative Tim accelerate delivery for standard layouts. Custom builds make sense when the UI is a product differentiator — for white-label SaaS where clients see the dashboard as part of what they're paying for.

Design for two user types simultaneously: a beginner who needs clear status indicators and safe defaults, and an advanced trader who needs granular controls, raw data export, and configurable alerts. A dashboard that serves only one of them will lose the other.

Testing Your Crypto Arbitrage Bot Before Going Live

Launching a crypto arbitrage bot without testing is rolling dice with real money. Smart teams treat testing as a multi-stage gate.Stage 1 — Backtesting. Run the strategy against historical order book data. This validates the logic: does spread detection fire at the right thresholds? Does fee modeling correctly reduce gross spreads to net margins? If a strategy isn't profitable in backtesting with realistic fee assumptions, it won't be profitable live. Caveat: backtesting can't model slippage on thin books or execution latency accurately — it shows directional validity, not precise P&L prediction.

Stage 2 — Paper trading. Connect to live data feeds but execute no real orders. The bot runs its full decision loop against simulated balances. This stage catches logic bugs that backtesting misses: race conditions, incorrect order routing, balance reconciliation errors, edge cases in fee calculation. Run paper trading for at minimum one full week across different market conditions.

Stage 3 — Stress testing. Push infrastructure beyond expected load. Can the bot handle order book update rates from five simultaneous exchanges without falling behind? What happens when an API call times out mid-trade? Does it correctly handle a partial fill? Failure modes discovered in stress testing are cheap. Failure modes in production are not.

Stage 4 — Security testing. API key handling, encrypted storage, injection testing on any user-facing inputs. For bots managing external capital, engage an external auditor. The cost is small relative to the exposure.

Only after passing all four stages should real capital enter the equation — and even then, start with a fraction of intended operating capital and scale up as live performance data confirms the backtest assumptions.

The Real Cost of Building a Crypto Arbitrage Bot

So how much money do you actually need to put a crypto arbitrage bot into the market? The answer depends on scope.If you're after the basics — a bot that links to a couple of exchanges, scans price spreads, and executes simple trades — you can get it done for $10,000–$20,000. That's the entry point for traders who want automation without heavy overhead.

A mid-tier build, the kind most startups go for, runs closer to $20,000–$40,000. At this level, your crypto arbitrage bot supports multiple strategies, risk controls, and comes with a dashboard where users can track performance and backtest.

| Strategy | General Principle | Example of Bot Operation |

|---|---|---|

| Inter-exchange arbitrage | Bot buys a coin on one exchange and sells it on another at a higher price. | Bot detects a $100 gap on ETH between OKX ($3,000) and Binance ($3,100). Buys 1 ETH on OKX, sells on Binance. Gross profit: $100 USDC minus fees. |

| Triangular arbitrage | The bot profits from pricing inefficiencies across 3 currency pairs within a single exchange or protocol. | Bot converts 55,000 USDC → 1 BTC → 110 BNB → 56,000 USDC in a single atomic sequence. Net gain: ~1,000 USDC minus commission fees. |

| Funding Rate Arbitrage | The bot captures funding rate differentials for the same asset across multiple perpetual futures markets. | Bot detects XRP funding rate 0.05% on platform A vs. 0.03% on platform B. Opens long on A and short on B. Profit locked in from rate differential regardless of price direction. |

| Time arbitrage | The bot exploits price update latency differences between exchanges. | Exchange A updates BTC/USD every 5 minutes; Exchange B every 10 minutes. When A shows $56,000 while B still reflects $55,000, the bot executes before B catches up. |

If the goal is a full platform — dozens of exchange integrations, mobile apps, AI-driven analysis, subscription tiers, and institutional-grade security — the budget jumps to $40,000–$80,000+.

The costs that catch teams off guard post-launch: cloud server fees scale with exchange connections and trade volume; API costs increase as you upgrade tiers for higher rate limits; security audits are recurring, not one-time; and any strategy update touching execution logic requires a full re-test cycle. Build these into your operating budget from day one.

costs to develop

your crypto bot

FAQ: Building a Crypto Arbitrage Bot

What programming language is best for building a crypto arbitrage bot?

Python is the standard choice — deep library support (ccxt, asyncio, pandas), fast iteration, and sufficient performance for inter-exchange strategies where network latency dominates over local processing time. Rust or C++ make sense for intra-chain strategies on fast blockchains like Solana where microsecond execution differences matter. Many production systems use a hybrid: Python for strategy logic, Rust or Go for the execution engine.

How much does it cost to build a crypto arbitrage bot?

A basic bot connecting 2–3 exchanges with simple spread detection runs $10,000–$20,000. A mid-tier build with multiple strategies, risk controls, and a dashboard is $20,000–$40,000. A full SaaS platform with mobile apps, AI analytics, and institutional security runs $40,000–$80,000+. Post-launch costs — servers, API upgrades, audits, updates — typically add 20–40% annually to your initial build cost.

What is the difference between CEX and DEX arbitrage bots?

CEX bots trade on centralized exchanges via REST/WebSocket APIs — faster order matching, higher liquidity, but withdrawal fees and transfer latency erode cross-exchange margins. DEX bots interact directly with smart contracts on-chain — no withdrawal delays within a chain, but gas fees and on-chain latency introduce different cost layers. CEX↔DEX hybrid strategies carry the highest visible spreads but also the most hidden execution costs; our project experience consistently shows they underperform intra-platform strategies when all costs are fully modeled.

What is slippage and how does it affect arbitrage bot profitability?

Slippage is the difference between the expected execution price and the actual fill price, caused by insufficient order book depth at your trade size. A spread that looks profitable at the top-of-book price may be unprofitable after slippage. Production-grade bots model slippage explicitly — evaluating each opportunity at both the nominal spread price and the realistic execution price adjusted for pool depth. Only trades that show net profit after slippage and fees should execute.

Can I build a crypto arbitrage bot for DEXs like Uniswap or Raydium?

Yes. On Ethereum-based DEXs, the bot interacts with AMM smart contracts directly — no API key required, but gas fees and MEV competition are significant factors. On Solana (Raydium, Jupiter), the fee market is different and throughput is higher, but WebSocket pool monitoring and server co-location near Solana validators become the critical infrastructure decisions. DEX-only strategies eliminate withdrawal latency but require solid on-chain infrastructure and smart contract interaction logic.

How long does it take to build a crypto arbitrage bot?

A basic bot: 6–10 weeks. A mid-tier product with dashboard and multi-exchange support: 3–5 months. A full SaaS platform: 6–12 months depending on feature scope. The testing phase — backtesting, paper trading, stress testing, security audit — typically adds 4–8 weeks on top of development and should not be compressed regardless of timeline pressure.