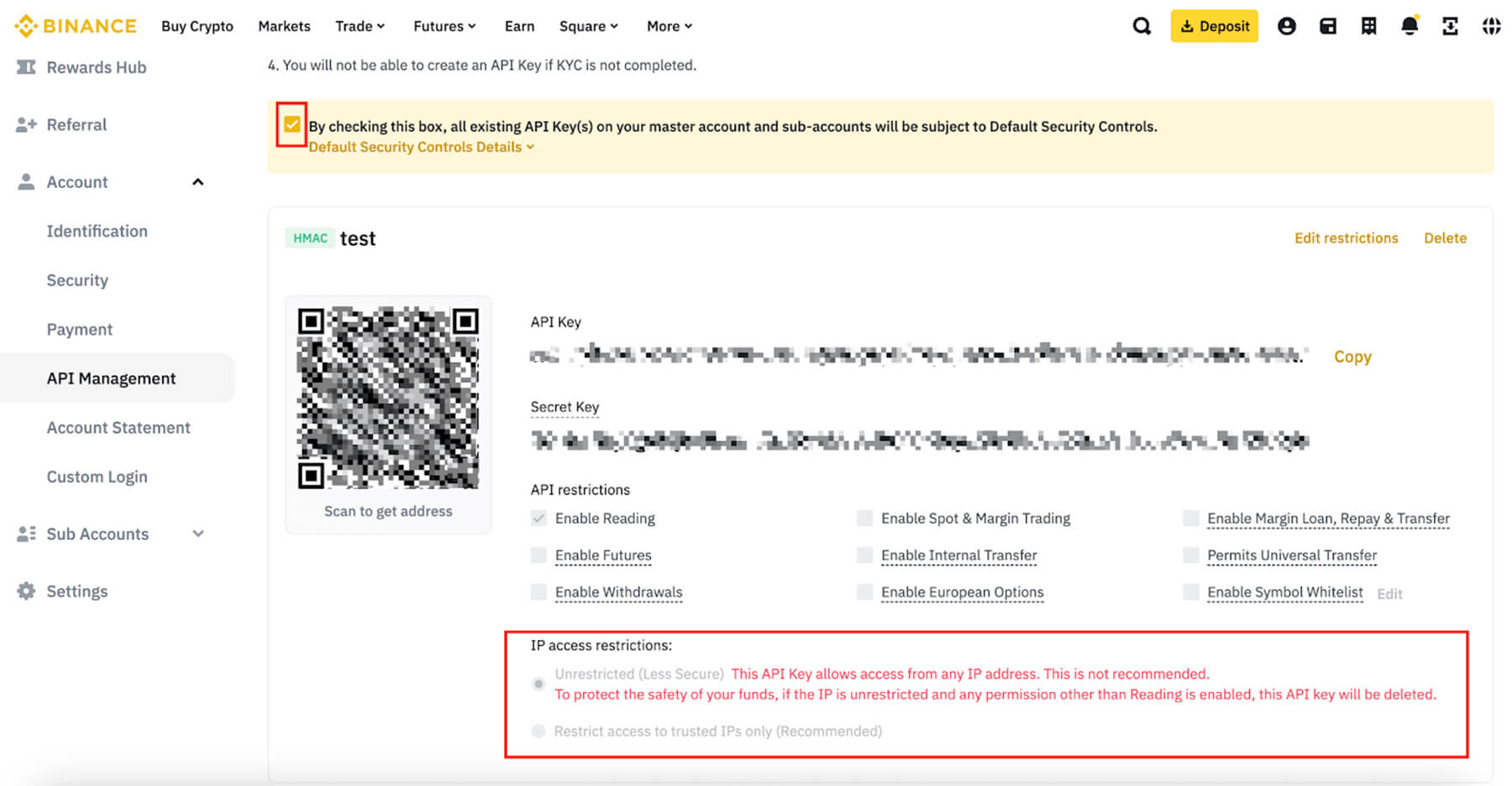

- Generate API keys in Binance Account → API Management. Enable trading permissions; disable withdrawals.

- Choose a language. Python with the

python-binancelibrary is the standard starting point. Node.js is preferred for real-time dashboards and Telegram integration. - Connect and test. Fetch your account balance or current BTC/USDT price via API — if data returns, the connection works.

- Add a strategy. RSI (buy below 30, sell above 70) or Moving Average crossover are the simplest starting points. Add order placement logic once the signal fires.

- Backtest before going live. Run the strategy on 3–6 months of historical data using Binance's Klines API or a library like

backtrader. - Deploy on a VPS close to Binance servers (AWS ap-northeast-1) to minimize latency. Start with $10–$20 per trade and monitor for at least 2 weeks before scaling.

Binance explicitly allows trading bots under its Terms of Service. Key technical constraints: API rate limits are weight-based (not just request count), WebSocket is preferred over REST for streaming data, and withdrawals require a separate explicit key permission.

What Is a Binance Trading Bot and How Does It Actually Work?

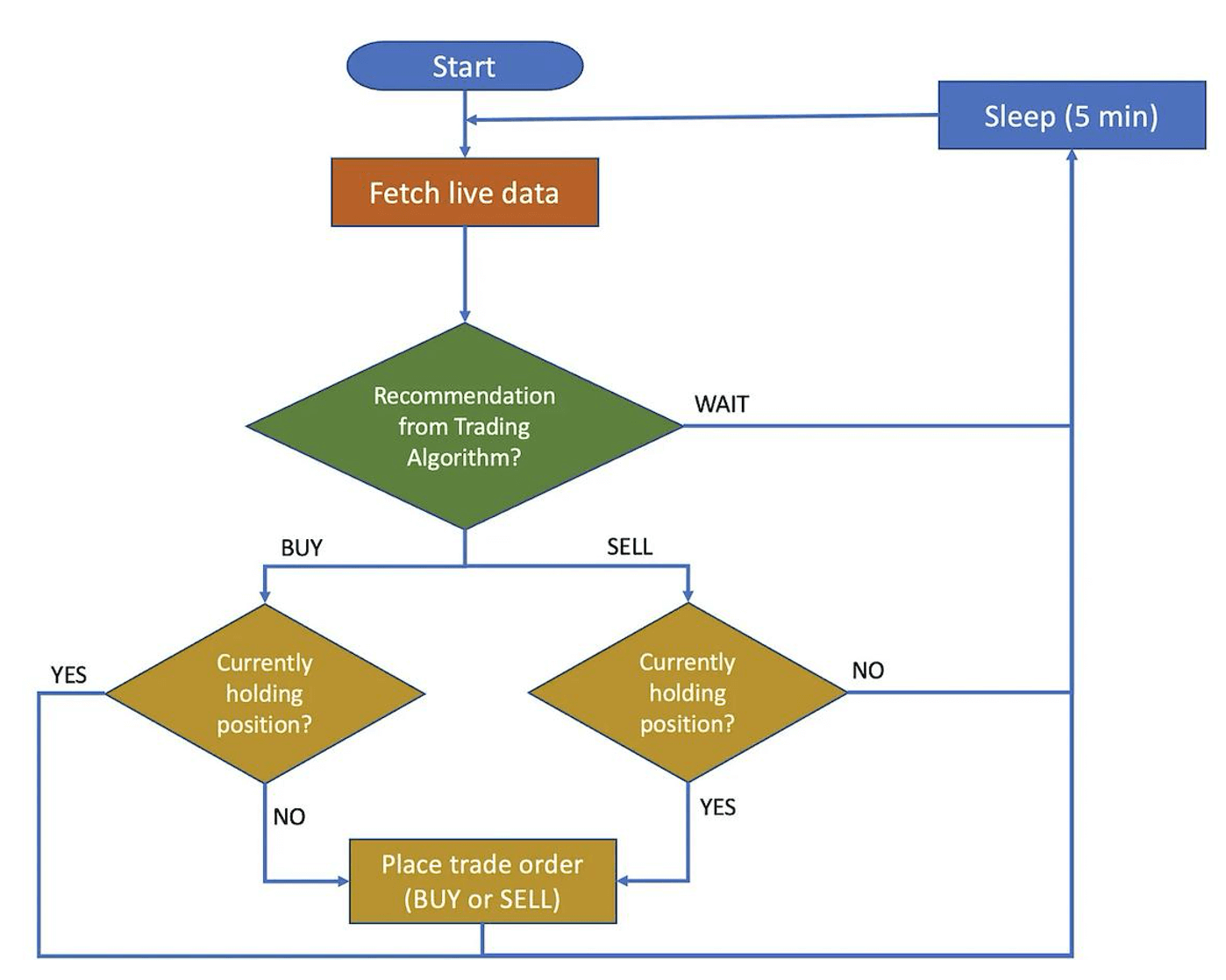

A Binance trading bot is a piece of software that communicates with the exchange through its API and executes orders on your behalf — checking prices, placing or canceling trades, and managing balances without any manual input. You define the logic once; the bot repeats it every time conditions are met.From an architectural standpoint, every Binance bot — regardless of complexity — performs the same three operations in a loop: fetch market data → evaluate strategy logic → send order. The speed and reliability of each of these steps determines whether the bot is profitable in production or only on paper.

| Bot Level | Architecture | Hard Limits | Best For |

|---|---|---|---|

| Simple bot | Single script, REST API polling | 1–2 pairs, no failover, ~5–10 req/sec | Personal use, learning |

| Multi-strategy bot | Separate monitor + execution services, DB for logs, WebSocket feeds | Several pairs in parallel, basic failover | Serious personal use, early SaaS |

| Trading platform / SaaS | Node.js business logic + Python AI layer + vector DB, multi-tenant, CI/CD | Hundreds of accounts, full API key isolation | Commercial product |

Binance API: Keys, Permissions, and Security Architecture

To do anything useful on Binance, your bot needs an API connection. Binance exposes two endpoint categories with fundamentally different access levels.Public endpoints — market data only: current prices, order books, 24h volume, candlestick history. No authentication required. Private endpoints — account-level actions: creating orders, canceling them, reading balances, and — if you explicitly allow it — withdrawing funds. Most production bots never enable the withdrawal permission, and they should not.

When you generate an API key pair in Binance → Account → API Management, you get two strings: the API Key (public identifier) and the Secret Key (never transmitted, used only for HMAC signature generation on your side). The exchange never sees the secret key — it only validates the signature produced by it.

1. Enable only the permissions the bot actually needs (trading = yes, withdrawals = no).

2. Whitelist your VPS IP address in Binance API settings — this prevents key use from any other machine.

3. Never store keys in code. Use environment variables or a secrets manager (AWS Secrets Manager, HashiCorp Vault).

4. Rotate keys after any suspected exposure, team member departure, or infrastructure change.

5. Monitor your API key activity log in Binance regularly — unauthorized calls appear there before they do damage.

6. Use separate key pairs for separate bots or strategies — if one key is compromised, others remain unaffected.

From our experience building trading systems: most production incidents involving exposed keys trace back not to code vulnerabilities, but to keys committed to git repositories or shared in Slack messages during development.

For deeper reading on keeping the API layer protected, see our dedicated guide on crypto exchange security practices — many of the same principles apply at the bot infrastructure level.

Step-by-Step Guide: Building Your Binance Bot

Step 1: Create a Binance account and generate API keys

Go to your Binance profile → API Management → Create API. Name the key, complete 2FA verification, and save both strings securely. Enable "Enable Spot & Margin Trading". Leave "Enable Withdrawals" unchecked. Optionally restrict access to your server's IP address — this single step eliminates the risk of key theft from most attack vectors.

Step 2: Set up your development environment

For Python: installpython-binance, pandas (for data manipulation), and python-dotenv (for environment variable management). Store your keys in a .env file, never hardcoded:

pip install python-binance pandas python-dotenv

# .env file

BINANCE_API_KEY=your_public_key_here

BINANCE_SECRET_KEY=your_secret_key_here

For Node.js: install node-binance-api or the official @binance/connector package. Node is particularly well-suited when you plan to combine your bot with a real-time dashboard or a Telegram bot for trade notifications — the async event model handles WebSocket streams cleanly.

Step 3: Establish the connection

The "hello world" moment — fetch your account balance or current BTC/USDT price. If data returns without error, the connection is live. This is also where you validate that your key permissions are set correctly — a trading bot trying to use a read-only key will fail here, not in production.from binance.client import Client

from dotenv import load_dotenv

import os

load_dotenv()

client = Client(os.getenv("BINANCE_API_KEY"), os.getenv("BINANCE_SECRET_KEY"))

# Connection test

price = client.get_symbol_ticker(symbol="BTCUSDT")

print(price) # {'symbol': 'BTCUSDT', 'price': '67243.50'}

# Account balance check

info = client.get_account()

print(info['balances'][:3])

Step 4: Implement a trading strategy

Start with RSI — it is the most straightforward signal to code and test. Fetch historical candlestick data viaget_historical_klines(), calculate RSI using pandas or the ta library, and trigger a market order when the threshold is crossed:

import pandas as pd

import ta

klines = client.get_historical_klines("BTCUSDT", Client.KLINE_INTERVAL_1HOUR, "30 days ago UTC")

df = pd.DataFrame(klines, columns=['time','open','high','low','close','volume',...])

df['close'] = df['close'].astype(float)

df['rsi'] = ta.momentum.RSIIndicator(df['close'], window=14).rsi()

latest_rsi = df['rsi'].iloc[-1]

if latest_rsi < 30:

order = client.order_market_buy(symbol='BTCUSDT', quoteOrderQty=50)

elif latest_rsi > 70:

order = client.order_market_sell(symbol='BTCUSDT', quantity=0.001)

Step 5: Backtest before touching real funds

Skipping backtesting is the single most common mistake. Run your strategy against 3–6 months of historical Klines data and track what the P&L would have been. A strategy that loses money on historical data will not magically start winning in production. Pay particular attention to drawdown periods — how deep did the strategy go into loss before recovering? That number determines how much capital you need to withstand normal variance without hitting a forced stop.For more rigorous backtesting, use backtrader with Binance historical data, or run the strategy against Binance Testnet — a paper-trading environment with real API structure but no real funds at risk.

Step 6: Handle API rate limits before going live

This is the step most tutorials skip entirely, and it is where real-world deployments break. Binance uses a weight-based rate limit system — each endpoint call costs a different number of "weight units," and the total resets every minute. A polling-based bot that checks 10 pairs every second will exhaust its limit in under 2 minutes.Practical solutions:

Switch from REST polling to WebSocket streams for price data — a single WebSocket connection can stream dozens of pairs simultaneously with zero weight cost.

Use client.get_exchange_info() once at startup to cache symbol data instead of fetching it on every cycle.

Implement exponential backoff with jitter for HTTP 429 (rate limit) and 418 (IP ban) responses.

For high-frequency strategies, contact Binance support to apply for elevated rate limits — verification tier upgrades or reaching minimum trading volume thresholds are the two standard paths.

Step 7: Deploy on VPS with latency in mind

Running your bot on home Wi-Fi introduces unpredictable latency spikes that will cost you on time-sensitive entries. For production deployments, use a VPS in the same data center region as Binance's matching infrastructure. Binance.com's primary nodes run on AWS in the ap-northeast-1 (Tokyo) region — a VPS there typically delivers 5–15ms round-trip latency vs. 80–200ms from European or US-East cloud instances.For strategies where execution speed is critical (scalping, new-listing snipers), that 100ms difference is the margin between a filled order and a missed trade. From our practical experience: latency is the one variable that neither the developer nor support can fix once the infrastructure decision is made — it is purely a function of physical proximity to the exchange's servers.

Step 8: Go live with minimum capital

Start with $10–$20 per trade. Observe at least two full weeks of live behavior before increasing position size. Watch for three specific failure modes: order placement errors (wrong quantity precision), partial fills that leave open positions, and missed sell signals during high-volatility periods when the bot falls behind on data processing.Trading Bot Strategies for Binance: RSI, Grid, Arbitrage, and AI Signals

The bot is just the execution layer. The strategy is everything. Here are the main approaches, ranked by implementation complexity:

RSI (Relative Strength Index) — the standard entry point. Buy when RSI < 30 (oversold), sell when RSI > 70 (overbought). Works on any timeframe; 1h and 4h give fewer false signals than 1m. Risk: performs poorly in strong trending markets where RSI stays in overbought/oversold territory for extended periods.

Moving Average Crossover — buy when the short-term MA (e.g., 20-period) crosses above the long-term MA (e.g., 50-period); reverse for sell. Widely used because it is trend-following and filters out noise. Risk: significant lag — by the time the signal fires, a portion of the move has already happened.

Grid Trading — place a ladder of buy orders below current price and sell orders above it at fixed intervals. The bot profits from oscillation within the range. Particularly effective in sideways, ranging markets. Risk: a strong breakout in either direction leaves the bot holding a losing position at range edge.

Scalping — dozens of small trades per hour, each targeting 0.1–0.5% profit. Impossible to execute manually; bots are built for this. The challenge is fees: at 0.1% per trade (Binance standard), a round trip costs 0.2%, meaning your average win needs to consistently exceed that or the strategy is net negative.

Arbitrage — exploit price differences between pairs, exchanges, or CEX↔DEX combinations. Sounds straightforward; in practice it involves three compounding challenges covered in the section below. For a detailed technical breakdown of building a standalone arbitrage system, see our guide on crypto arbitrage bot development.

Arbitrage on Binance: Three Layers of Technical Complexity

Arbitrage strategies deserve a dedicated section because the gap between the theoretical concept and production-ready implementation is larger here than with any other approach.Challenge 1: Gas price and transaction priority (DEX/CEX↔DEX arbitrage). On-chain transactions compete for block inclusion. To execute before competitors, your bot must dynamically assess current gas market conditions and set a premium accordingly. A static gas price parameter will cause either overpaying consistently or losing the race for inclusion during network congestion.

Challenge 2: Slippage by liquidity category. Not all tokens behave the same on execution. A workable approach classifies tokens into at minimum three liquidity tiers — high, medium, and low — each with different acceptable slippage parameters. Without this categorization, a bot will execute trades at significantly worse prices than the theoretical entry point, eroding theoretical profit margins entirely.

Challenge 3: MEV and front-running. On DEX environments, simple arbitrage bots become visible in the mempool before execution. MEV (Maximal Extractable Value) bots detect incoming transactions and insert their own ahead of them. This is not a solvable code problem — it requires architectural responses: private transaction relays (Flashbots on Ethereum), commit-reveal schemes, or evolving to AMM-integrated strategies that are less vulnerable to front-running by design.

The classic trap: the bot shows excellent backtesting results, but in production, slippage and gas costs make the same strategy unprofitable. The fix is not better backtesting — it is adding live Testnet validation with real transaction competition before committing to live deployment.

CEX↔DEX arbitrage (e.g., Binance Spot vs. an on-chain DEX) adds another variable: bridge transaction latency and price movement during block confirmation time. In volatile markets, a 15-second bridge confirmation can turn a profitable arbitrage into a loss.

The realistic architecture progression for production arbitrage: simple arbitrage bot → arbitrage + AMM integration → arbitrage + AMM + MEV protection. Each step roughly doubles the development scope.

AI-Powered Trading Signals: Multi-Agent Architecture

A new category of trading systems has emerged that goes beyond rule-based bots: LLM agent orchestration for signal generation. This is architecturally distinct from a classic RSI or MA bot — the value proposition is explainability and continuous improvement, not just execution speed.The key architectural distinction between a demo and a production-grade system:

- Single LLM call — generates a signal with no traceable reasoning chain. Non-deterministic, hard to debug, impossible to improve systematically.

- Multi-agent system — separate agents for market data analysis, signal processing, and trade decision; each with its own role, system prompt, and access to shared memory. Produces explainable outputs: "signal triggered because RSI crossed 30 AND volume deviated 2σ from 7-day average AND historical pattern match confidence = 0.84".

The technical stack that has proven itself in practice for trading AI systems: Node.js for business logic, API layer, and database interaction + Python for LLM orchestration (LangGraph, CrewAI) + PostgreSQL + PgVector as a vector database for RAG-based market history retrieval. This separation allows scaling the AI layer independently of the core backend without vendor lock-in to a specific LLM provider.

For a complete technical walkthrough of building AI-driven signal generation for trading products, see our guide on creating an AI trading bot.

Backtesting: The Difference Between a Strategy and a Theory

Backtesting is not optional. It is the minimum validation gate before a strategy is allowed to touch real funds. The goal is not to find a "perfect" strategy — it is to understand the realistic performance envelope: average win rate, average drawdown, maximum consecutive losses, and Sharpe ratio.Two tools for Binance backtesting in Python:

- backtrader — mature framework, supports custom data feeds (including Binance Klines), commission models, and position sizing. Generates full performance reports.

- pandas + manual simulation — faster to set up for simple strategies, but requires more custom code for realistic commission and slippage modeling.

The most important backtesting discipline: out-of-sample validation. Optimize your parameters on 70% of historical data. Test the result on the remaining 30% without further modification. If performance degrades sharply on the held-out period, the strategy is over-fitted — it has memorized past data rather than learned a repeatable pattern. A strategy that only works on the data it was trained on will fail in production.

From Bot to Product: SaaS Architecture and Monetization Paths

Once a bot produces consistent results, there are two directions: keep it as a private tool, or build it into a commercial product. The architecture decisions differ significantly between these paths.Personal use bot: A single-tenant setup where your keys are hardcoded (in a .env file), strategy logic is monolithic, and failure recovery is manual. Perfectly adequate for trading your own capital.

SaaS trading bot: Multi-tenant by definition. Each user's API keys must be encrypted at rest (AES-256) and isolated in execution — one user's bot crashing must not affect others. This requires a proper microservices architecture: separate key vault service, separate strategy execution workers, a monitoring layer, and a user-facing dashboard. The white label crypto trading bot model is the fastest path to market if you want to launch without building the entire infrastructure stack from scratch.

Strategy marketplace: Users build and publish strategies; others subscribe to them. Revenue model is commission on each subscription. This is the highest-complexity model but creates the strongest network effects — the platform becomes more valuable as the strategy library grows.

Key features that differentiate a commercial bot from a personal one: WebSocket-based real-time notifications (Telegram or email), multi-exchange support, a full trade history with P&L reporting, and configurable risk parameters per user account. If you are evaluating the commercial path, our detailed breakdown of crypto trading bot development costs covers realistic budgets and timelines for each architecture tier.

Risks, Limitations, and What to Monitor in Production

A Binance bot running in production has four failure categories that need active monitoring:Market volatility beyond strategy parameters. A strategy calibrated on 2023 ranging markets may produce catastrophic drawdowns during a 2024-style trending period. Bots do not adapt — they execute their rules regardless of regime. Add a volatility circuit breaker: if ATR (Average True Range) exceeds a threshold, the bot pauses and notifies you.

Technical failures. Internet drops, VPS downtime, unhandled API exceptions — any of these can leave the bot in an undefined state: holding a position it cannot sell, or sending duplicate orders. Every production bot needs: exception handling on every API call, state persistence to database (not just memory), and a watchdog process that restarts the bot if it crashes.

Over-optimization (curve fitting). A strategy optimized to minimize loss on historical data will often have been tuned to specific past conditions that will not repeat. The symptom is high backtesting performance combined with poor live performance. The fix is out-of-sample validation, described above.

Binance API changes and rate limit violations. Binance updates its API periodically. Breaking changes in response formats or new deprecation of endpoints will crash bots that have not been maintained. Rate limit violations that produce HTTP 418 responses result in IP bans — recovery requires waiting out the ban period or switching IP.

What to Do Next: Your Pre-Launch Checklist

Before deploying any bot with real capital, work through this checklist:- API keys created with correct permissions (trading yes, withdrawals no), IP-whitelisted

- Keys stored in environment variables, not in code or git repository

- Strategy backtested on minimum 3 months of historical data with out-of-sample validation

- Strategy validated on Binance Testnet (paper trading) for at least 1 week

- WebSocket data feeds in place (not REST polling) for any price monitoring loop

- Rate limit handling implemented (429/418 response codes caught with backoff)

- All API calls wrapped in try/except with database logging of failures

- State stored in persistent database (not in-memory) so restarts are safe

- VPS deployed in ap-northeast-1 (or nearest to your exchange's infrastructure)

- Volatility circuit breaker configured

- Monitoring alert set for any unhandled exception or unexpected position state

- Starting capital limited to an amount you can afford to lose entirely during validation

If you are building a bot for commercial purposes — multi-user SaaS, strategy marketplace, or a copy trading layer on top — the architecture complexity increases significantly. Our team has delivered production trading systems across DEX, CEX, and hybrid architectures. For a full technical and commercial assessment of your specific use case, see the crypto trading bot development services page.

FAQ: Binance Trading Bots

Is it legal to use a trading bot on Binance?

Yes — Binance explicitly provides API access for automated trading and does not prohibit bots in its Terms of Service. The restriction is behavioral, not categorical: aggressive request spamming, market manipulation attempts, or API abuse will result in rate limiting or account suspension. A bot that trades within normal API usage guidelines is fully permitted.

Do I need to know how to code to build a Binance bot?

Basic Python knowledge is sufficient for a rule-based bot. The

python-binancelibrary abstracts most of the API complexity, and RSI or MA strategies require fewer than 100 lines of code in their simplest form. For no-code options, third-party platforms like 3Commas or Pionex offer bot configuration without programming — the trade-off is limited strategy customization and dependency on their infrastructure and business model.What is a realistic profit expectation from a Binance trading bot?

There is no reliable benchmark — performance depends entirely on strategy, risk parameters, market conditions, and how actively the bot is maintained. A well-calibrated RSI or grid strategy on a ranging market might produce 2–5% monthly returns with controlled drawdown. The same bot on a trending market can produce significant losses. Anyone promising fixed or "guaranteed" returns from a trading bot is selling a fiction, not a product.

What is the best strategy to start with?

RSI-based signals or Moving Average crossovers on 1h or 4h candles. They are straightforward to implement, their logic is easy to debug, and there is extensive historical data to backtest against. Avoid arbitrage or scalping as first strategies — both require infrastructure-level optimizations (latency, rate limits, slippage handling) that add complexity before you have validated your core bot mechanics.

Can I run multiple strategies on the same bot?

Yes, but this requires moving to a microservices architecture. Each strategy should run as an independent worker process with its own data feed and order queue. Coupling multiple strategies in a single script creates shared state problems: a hang in one strategy's data fetch loop will block order execution for all others. This is the inflection point where a "simple bot" becomes a "multi-strategy platform" with corresponding architectural overhead.

How do I handle API rate limits in production?

Switch price monitoring from REST polling to WebSocket streams — this eliminates the majority of weight consumption. Cache static data (exchange info, symbol filters) at startup rather than fetching per cycle. Implement proper 429/418 response handling with exponential backoff. For high-frequency strategies, apply for elevated rate limits through Binance's VIP program or via direct API support contact — the standard path is reaching minimum 30-day trading volume thresholds.