- RWA tokenization market reached $27.5B on-chain TVL by end of Q1 2026, growing 30% in a single quarter

- Tokenized US Treasuries crossed $13B in April 2026 — a 7,400% increase since January 2023

- Institutional RWA projects grew 800% from 2023 to 2025; over 200 active projects today

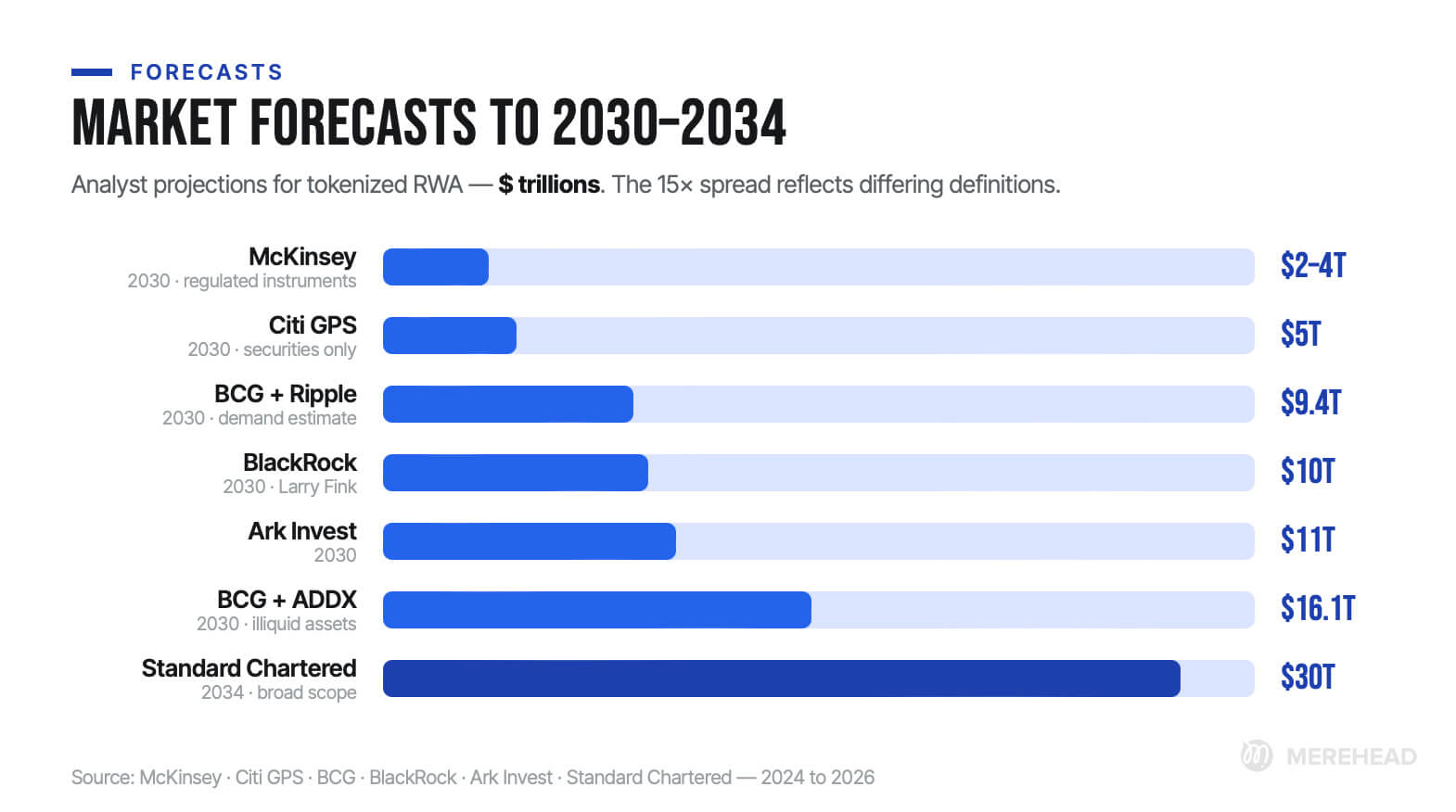

- Long-term market forecasts range from $2T (McKinsey) to $30T (Standard Chartered) by 2030–2034

- 86% of institutional investors already have or plan exposure to digital assets (EY, 2025)

- Compliant RWA MVP development starts at $120K–$250K; enterprise-grade platforms exceed $1M

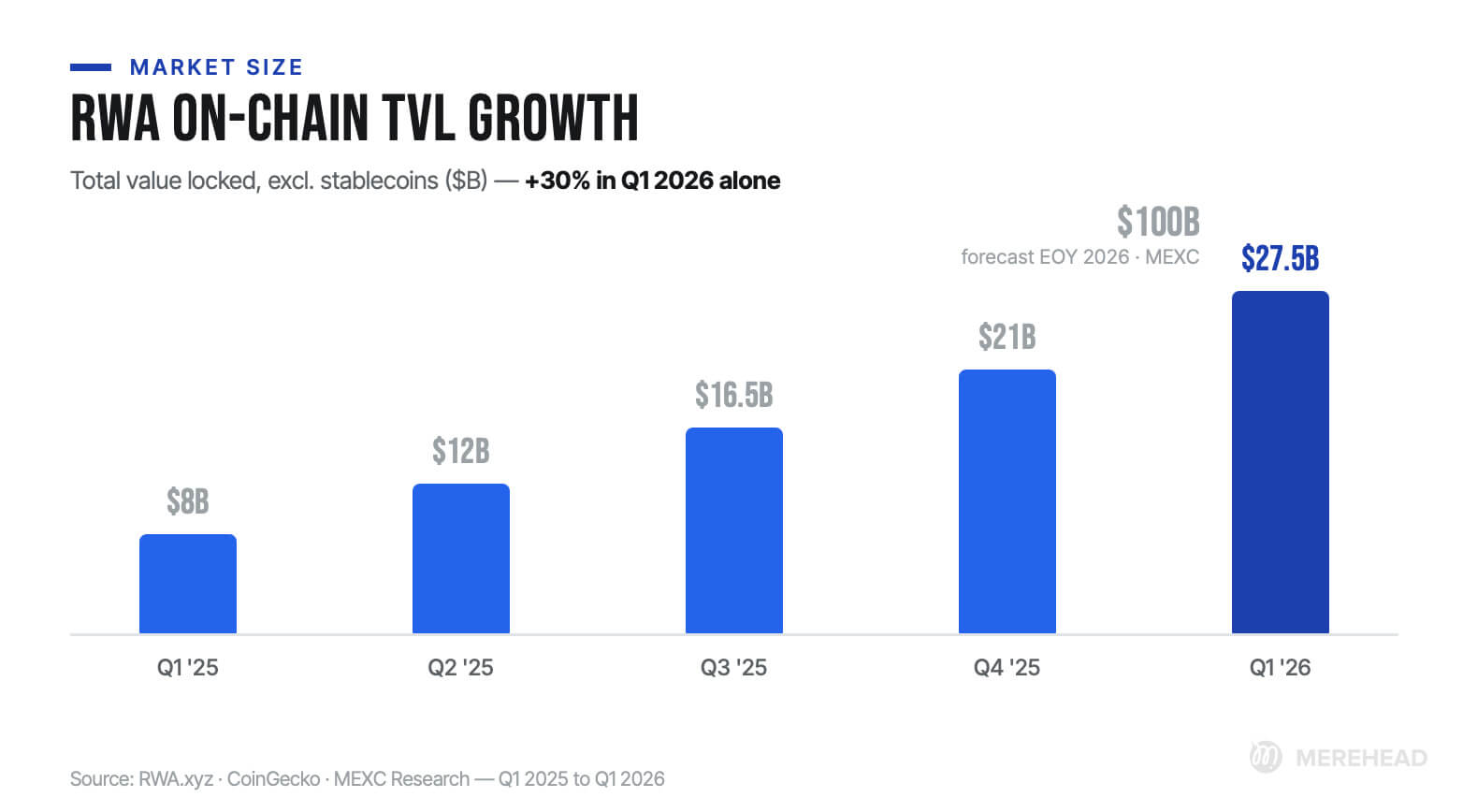

$27.5 billion. That is the volume of real-world assets tokenized on-chain as of Q1 2026, excluding stablecoins, according to RWA.xyz data. Not a whitepaper projection. Capital that has already passed through smart contracts, oracle price feeds, and compliance frameworks. The market added 30% in a single quarter. Tokenized US Treasuries crossed $13 billion for the first time in April.

Whether you are a CFO evaluating alternatives to traditional money market funds or a CTO scoping the architecture of a tokenization platform — this article gives you numbers, not marketing copy. We break down where the real-world assets market stands today, where analysts from BCG to BlackRock see it heading, and why tokenized real estate has become the priority vertical for institutional capital.

Key RWA Tokenization Statistics: Quick Overview

Before going into asset class detail, here is a consolidated snapshot of market scale at the start of 2026:

| Metric | Value | Source / Date |

|---|---|---|

| Total on-chain TVL (excl. stablecoins) | $27.5B | RWA.xyz, April 2026 |

| Institutional RWA project growth since 2023 | +800% | CoinLaw, Feb 2026 |

| BlackRock BUIDL peak AUM | $2.88B | Mid-2025 |

| Tokenized US Treasuries + MMF (mid-2025) | $7.5B | RedStone, Jun 2025 |

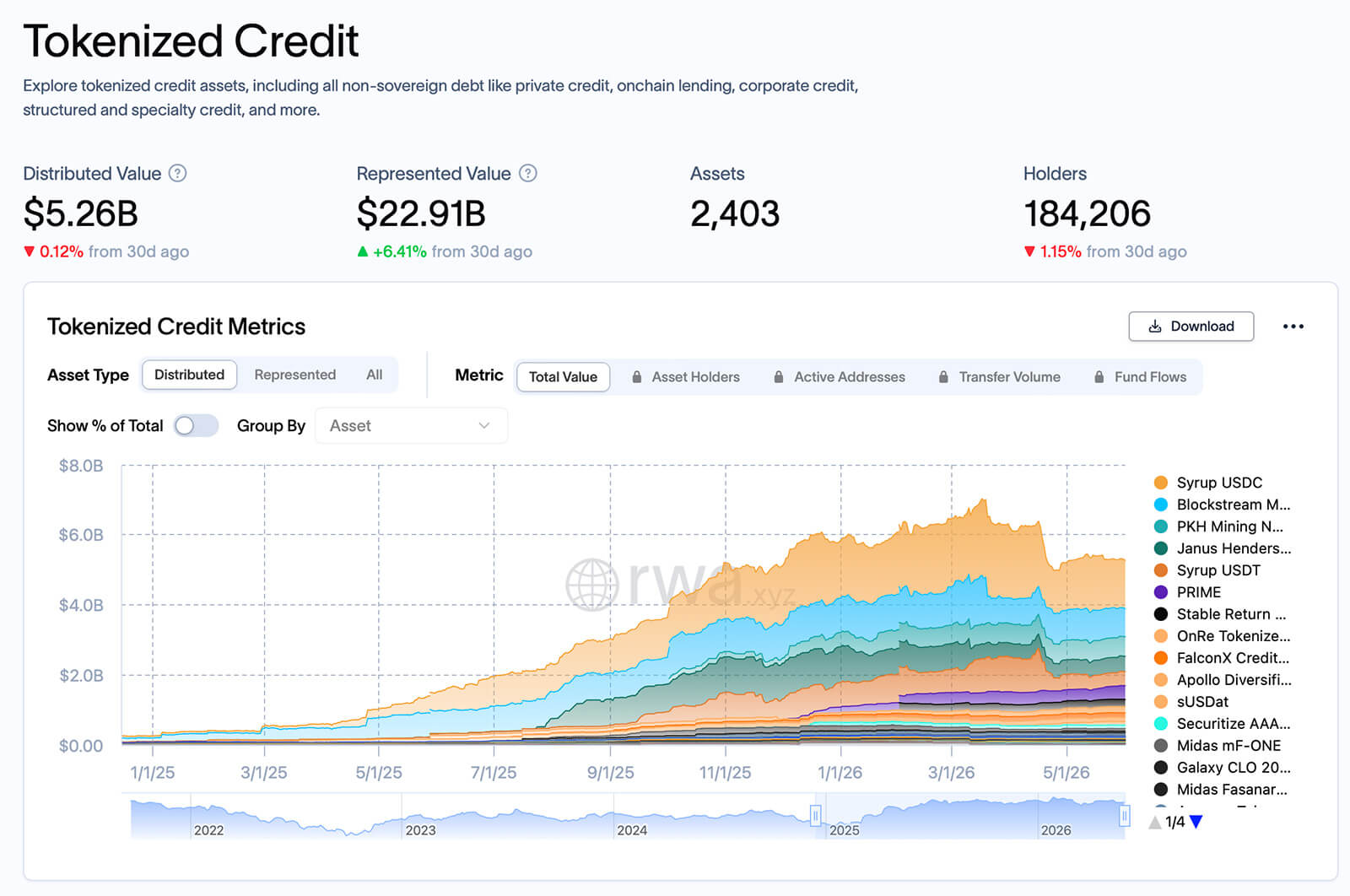

| Private credit on-chain TVL | $5B (on-chain); $18–19B incl. platform-locked | RWA.xyz, Mar 2026 |

| Tokenized real estate market (2025 est.) | $3.8B | CAGR 21–24% to 2034 |

| Long-term market projections | $16–30T | BCG, Standard Chartered, 2030–2034 |

| Institutional investors with digital asset exposure | 86% | EY, 2025 |

| Ondo Finance TVL (Jan 2026) | $2.5B+ | Largest tokenized Treasuries platform |

| Total RWA protocol TVL forecast by end of 2026 | $100B | MEXC Research |

The answer differs by jurisdiction, asset class, and the sophistication of the team building the infrastructure.

RWA Tokenization Market Size & Growth

What DeFiLlama and RWA.xyz Data Actually Show

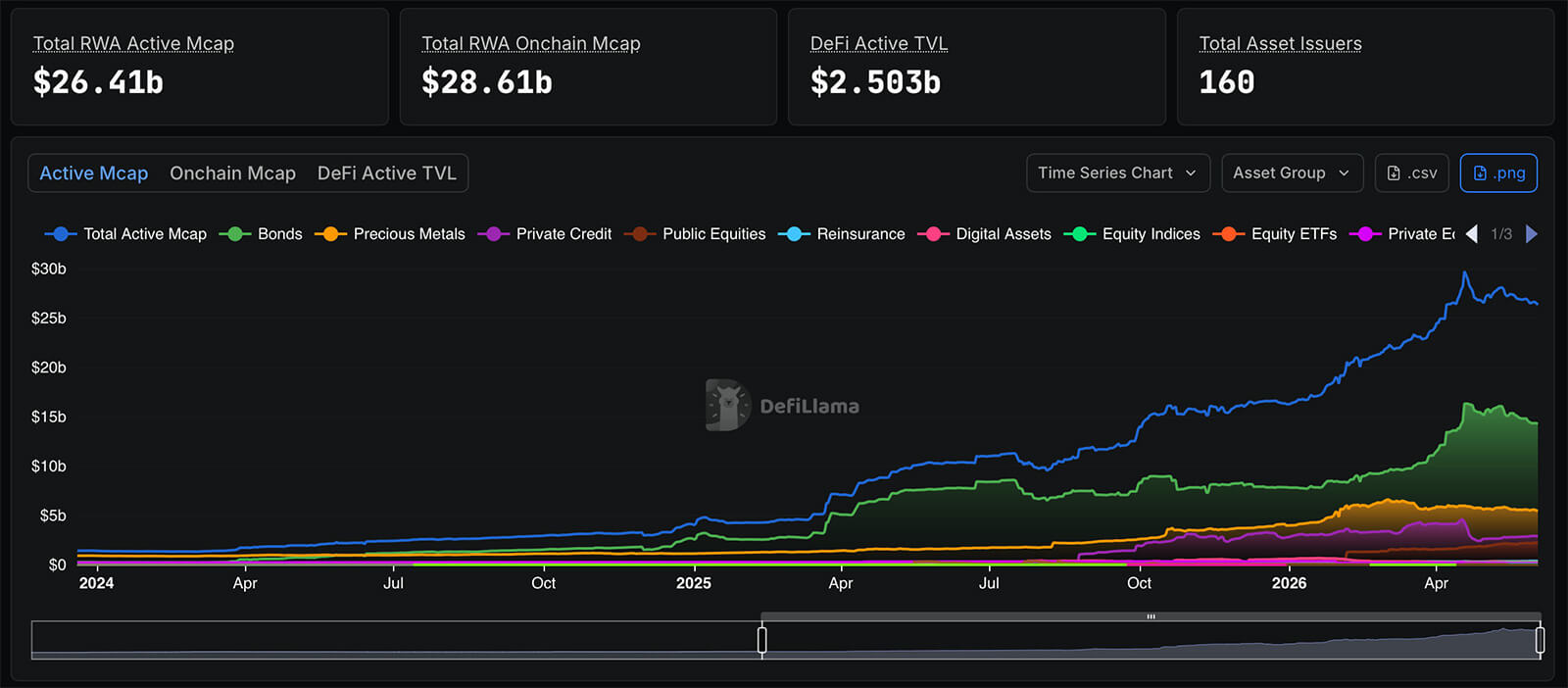

The RWA market is approaching $30B on-chain — but only $2.47B of that constitutes active DeFi TVL, meaning value actually deployed inside lending protocols and collateral pools. The remainder exists inside permissioned wrappers: closed corporate registries not visible to public trackers, yet fully real from an underlying asset perspective.

CoinGecko pegged tokenized RWA market capitalization at $19.32B at end of March 2026 — a 256.7% increase over fifteen months from the $5.42B baseline in early 2025. RWA.xyz, using a broader methodology that includes permissioned registries, measured ~$27.5B TVL at end of Q1 2026. For reference, the full-year 2025 took the market from roughly $6B to over $27.5B. That means Q1 2026 alone is compounding faster than most preceding annual periods.

Forecasts to 2030

| Source | Forecast | Horizon | Methodology |

|---|---|---|---|

| BCG + ADDX | $16.1T | 2030 | Tokenizable illiquid assets; ~50x from 2022 base |

| Standard Chartered | $30.1T | 2034 | Broad scope including trade finance |

| McKinsey & Company | $2–4T | 2030 | Financial instruments with clear regulatory status only |

| Citi GPS | up to $5T | 2030 | Conservative; tokenized securities only |

| Ripple + BCG | $18.9T | 2033 | ~53% CAGR; includes deposits and stablecoins |

| Roland Berger | $10T+ | 2030 | Regulated financial assets |

| World Economic Forum | $24T | 2027 | All asset classes; industry survey |

The spread — $3T to $30T — reflects not contradictory data but fundamentally different definitions of "tokenizable assets." Roland Berger counts only regulated financial instruments with an established legal standing. BCG and WEF include everything from infrastructure to fine art. Every forecast assumes regulatory clarity and infrastructure maturity as preconditions. None of them are bets on technology alone.

Global asset management is a $400T+ market. Even McKinsey's conservative $4–5T estimate implies tokenized assets growing from a fraction of a percent to 1–1.5% of the total — an outcome realistic within five years at current institutional adoption rates.

RWA Tokenization by Asset Class

The market is not a single curve. Six asset classes are at materially different stages of maturity — in secondary market liquidity, regulatory standing, and depth of institutional participation. As of early 2026, private credit leads by TVL, US Treasuries by institutional legitimacy, and real estate by long-term addressable market.

| Asset Class | On-chain TVL / Market Cap | Key Platforms | Growth Trajectory |

|---|---|---|---|

| Private Credit | ~$18.9B (active originations: $33.7B) | Centrifuge, Maple Finance, Goldfinch | Largest segment by TVL |

| US Treasuries / Bonds | ~$12.9B | BUIDL (BlackRock), BENJI, Ondo (OUSG) | +7,400% since Jan 2023 |

| Commodities (Gold) | ~$7.3B market cap (Apr 2026) | Paxos Gold (PAXG), Tether Gold (XAUT) | +289% in 2025 |

| Real Estate | ~$3.7–3.8B | RealT, Elevated Returns, SolidBlock | CAGR 21% to 2035 |

| Equities / Stocks | ~$487M–$2.7B | Ondo Global Markets, Backed Finance | $2.09M → $487M in 9 months |

| Art & Collectibles | $30–50M (est.) | Masterworks, Fractional.art | Early stage |

Private Credit: Largest Segment by Aggregate Value

Active on-chain private credit exceeded $18.91B as of November 2025 per rwa.xyz data, with cumulative originations reaching $33.66B. Leading platforms — Maple Finance, Centrifuge, and Goldfinch — structure senior secured loans, SMB financing, and accounts receivable in token form. Smart contracts automate yield distribution, cutting servicing overhead by up to 70% compared to traditional mechanisms.

For the institutional investor, this segment offers yields 200–400 basis points above comparable public credit instruments, with short origination cycles. The key risk is limited secondary market liquidity: most positions are held to maturity.

US Treasuries: The Flagship of Institutional Tokenization

The segment stood at ~$8.9B at the start of 2026, crossed $10B on February 11 for the first time, and reached $13.53B by April 12, 2026. The appeal mechanics are straightforward: US Treasuries are a standardized instrument with clear regulatory status, minimal valuation dispersion, and obvious utility for DeFi protocols that need yield-bearing collateral instead of volatile crypto assets. Goldman Sachs and BNY Mellon are tokenizing money market funds alongside BlackRock and Fidelity, targeting operational efficiency and settlement compression.

In one of our projects — a crypto payment processing platform built for a European client — we faced a similar architectural challenge: how to structure a multi-currency system that handles both on-chain crypto flows and traditional payment rails simultaneously. The infrastructure we built used a microservices architecture with modular blockchain connectors for BTC, ETH, USDT (ERC-20, TRC-20), Solana, and BNB Chain — exactly the kind of multi-chain stack that institutional tokenization platforms now require as a baseline. When the client asked whether integrating exchange APIs (Binance, Kraken, Huobi) required a separate contract, our answer was yes: exchange connectors and bot integrations have distinct rate-limiting and auth logic, and shipping them in a single sprint inflates risk without proportional value.

Commodities, Equities, and Other Classes

The commodity segment grew 289% in 2025 and reached a market cap of $7.3B by April 2026. Behind that number is effectively a single asset: gold accounts for approximately 70% of the total, with Tether Gold (XAUT) and Paxos Gold (PAXG) holding roughly 90% of the segment between them. Spot trading volume for tokenized gold in Q1 2026 reached $90.7B — already exceeding all of 2025 ($84.6B). Oil, metals, and agricultural commodities remain peripheral: physical custody is harder, and regulation has not caught up.

Tokenized equities are less a single dominant asset and more an infrastructure race. Coinbase, Robinhood, Kraken, and BitGo have launched or announced tokenized stocks, but volume is universally constrained by jurisdictional carve-outs and accreditation requirements.

Real estate and art sit at the opposite end of the maturity spectrum from Treasuries: the addressable market is massive, and the regulatory foundation is either complex or largely absent. Art is in the pilot phase — more projects than real capital.

Real Estate Tokenization Statistics

Real estate is the most obvious candidate for tokenization across all asset classes: a $326T+ global market historically defined by low liquidity and a high entry threshold. These are precisely the two structural characteristics that tokenization eliminates first.

Market Size and Projections

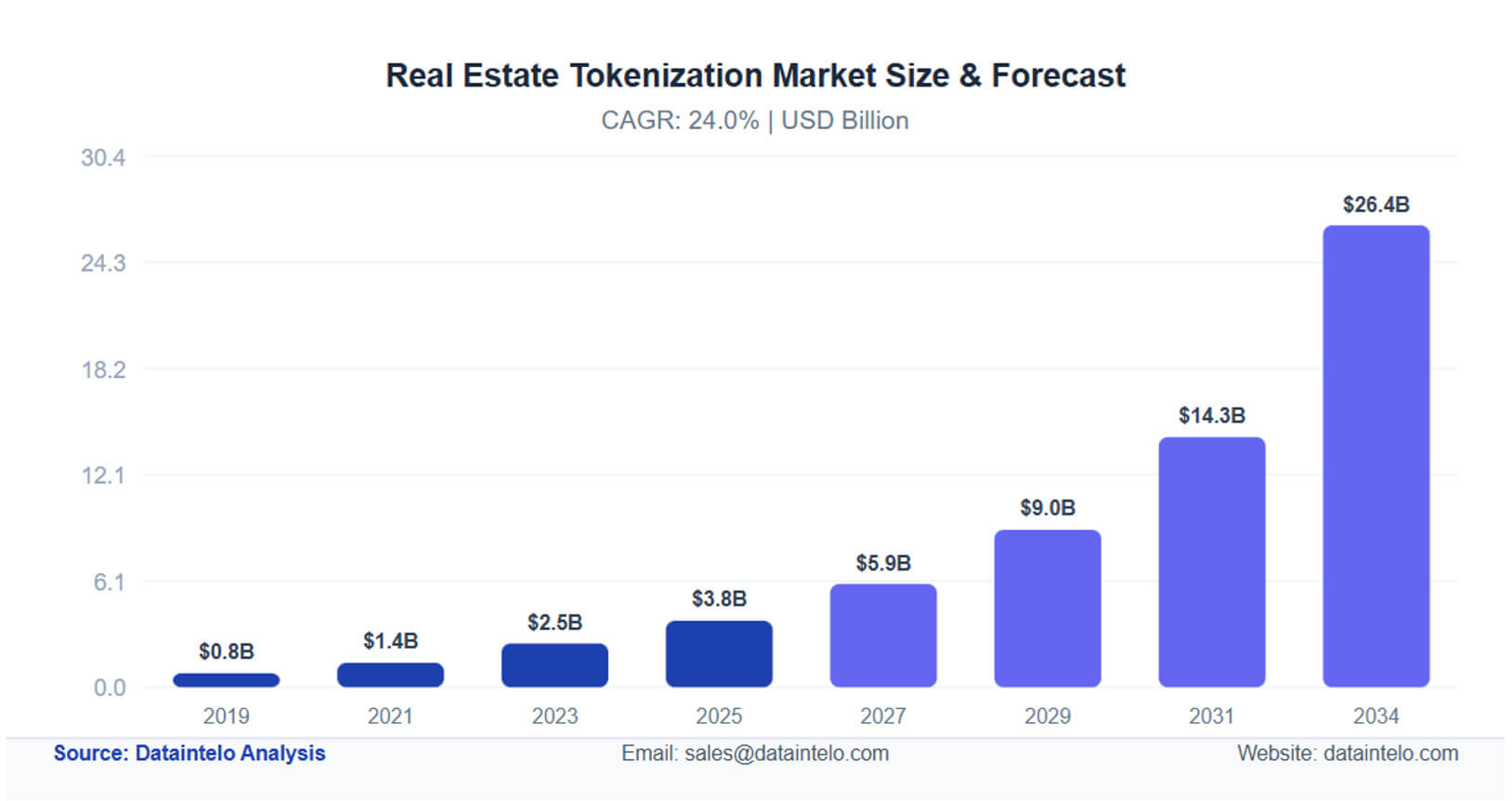

The tokenized real estate market was approximately $2.78B in 2024. The 2026 projection is $4.7B+: new issuance in the commercial segment, plus the first regulatory approvals in Europe and Asia, are providing concrete momentum. Long-horizon forecasts for 2035 are around $16.51B at a ~21% CAGR.

Longer-range estimates diverge more sharply. ScienceSoft projects $3T by 2030 — roughly 15% of the global real estate market under management. Deloitte looks further out: tokenized private real estate funds could reach $1T by 2035, capturing around 8.5% of the combined market. Both forecasts assume regulatory maturity in key jurisdictions — which is itself not guaranteed.

We have direct reference data on this: one of our clients — a US-based developer building a real estate tokenization platform — came with an architecture that needed to support NFT/token-based property ownership, fiat and crypto deposits, instant on-chain exchange, and a rental income distribution system across token holders.

The admin panel required granular role management, wallet controls, and a mechanism for the administrator to log rental revenue per property and trigger automatic pro-rata distribution. We scoped the full stack: website, web admin, iOS and Android apps, smart contracts on Binance Smart Chain, KYC/AML/2FA/anti-phishing, Zendesk integration, and a credit card payment gateway — delivered in three months.

That timeline is realistic for a focused scope; complexity grows fast once you add secondary market trading or cross-jurisdictional compliance. For teams navigating that complexity, our step-by-step guide to real estate tokenization covers the key decision points from legal wrapper to smart contract deployment.

Entry Threshold and Investor Profile

The defining feature of tokenized real estate versus traditional formats is the radical compression of the entry barrier. RealT — one of the oldest platforms — has tokenized over 970 properties in the US and sells tokens from $50. 88% of the platform's users have invested less than $5,000. Income-generating commercial properties in the US, UK, and UAE generate distribution yields of 5–9% annually with additional token appreciation potential.

For comparison: equity REITs in 2025 returned approximately 3.5–4% dividend yield. Dubai REITs delivered 6–8% — above the global average. Tokenized assets in the best jurisdictions formally compete with the upper end of REIT yields, while also offering fractional ownership and shorter settlement cycles.

In the EU, MiCA 2024 and the DLT Pilot Regime form the baseline legal framework; Switzerland and Germany lead in regulated platforms. Singapore's MAS licenses and Project Guardian provide the clearest institutional infrastructure in APAC. Dubai's Phase 2 regulatory program and the US SEC sandbox are establishing the most advanced compliance frameworks for property token issuance.

The legal wrapper selection is not a formality — it determines which investors can participate, what secondary trading is permissible, and how distributions are taxed.

Institutional RWA Adoption Statistics

Three years ago, institutional conversations about tokenization happened in "we are exploring" mode. Today they happen with measurable AUM, live products, and working settlement systems. Active institutional RWA projects have exceeded 200, growing 800% since 2023. Institutional investors constitute 86% of survey respondents on digital asset allocation. 2025 was the inflection point: both TradFi incumbents and crypto-native participants entered direct competition for positions in the tokenization stack, differentiating on regulatory standing, asset coverage, and distribution reach.

Banks Building RWA Infrastructure

JPMorgan's blockchain division — originally launched as Onyx in 2020 and rebranded to Kinexys in November 2024 — has processed over $1.5T in transactions: intraday repo, cross-border payments, and tokenized asset settlements. Average daily volume exceeds $2B. In December 2025, JPMorgan launched MONY, a tokenized money market fund on Ethereum with $100M in initial capital, allowing qualified investors to subscribe and redeem in USDC.

Siemens has established a sequential precedent for corporate issuers. Following its €60M digital bond on Polygon in 2023, the company issued €300M ($330M) on the permissioned SWIAT blockchain in September 2024 under ECB DLT settlement trials. Settlement took minutes instead of the standard T+2. The World Bank placed a 200M Swiss franc bond through SIX Digital Exchange — the first digital bond settled using central bank digital money under the Swiss National Bank's Project Helvetia III.

Asset Managers and Tokenized Products

BlackRock BUIDL launched in March 2024 and attracted $245M in its first week. AUM crossed $1B by March 2025 and reached $2.88B by mid-2025. By end-2025, the fund had distributed over $100M in cumulative dividends and was accepted as collateral on Binance, Deribit, and Crypto.com — the first precedent of a tokenized TradFi product achieving operational status inside crypto infrastructure.

Franklin Templeton BENJI — launched in 2021 as the world's first US mutual fund to use a public blockchain for ownership recordkeeping — managed approximately $846M AUM as of April 2026, with 99.5% of the portfolio in US government securities, cash, and repos. Goldman Sachs and BNY Mellon are tokenizing money market funds in coordination with BlackRock and Fidelity. Securitize, serving funds from Apollo, Hamilton Lane, KKR, and VanEck, managed combined AUM exceeding $4B by October 2025.

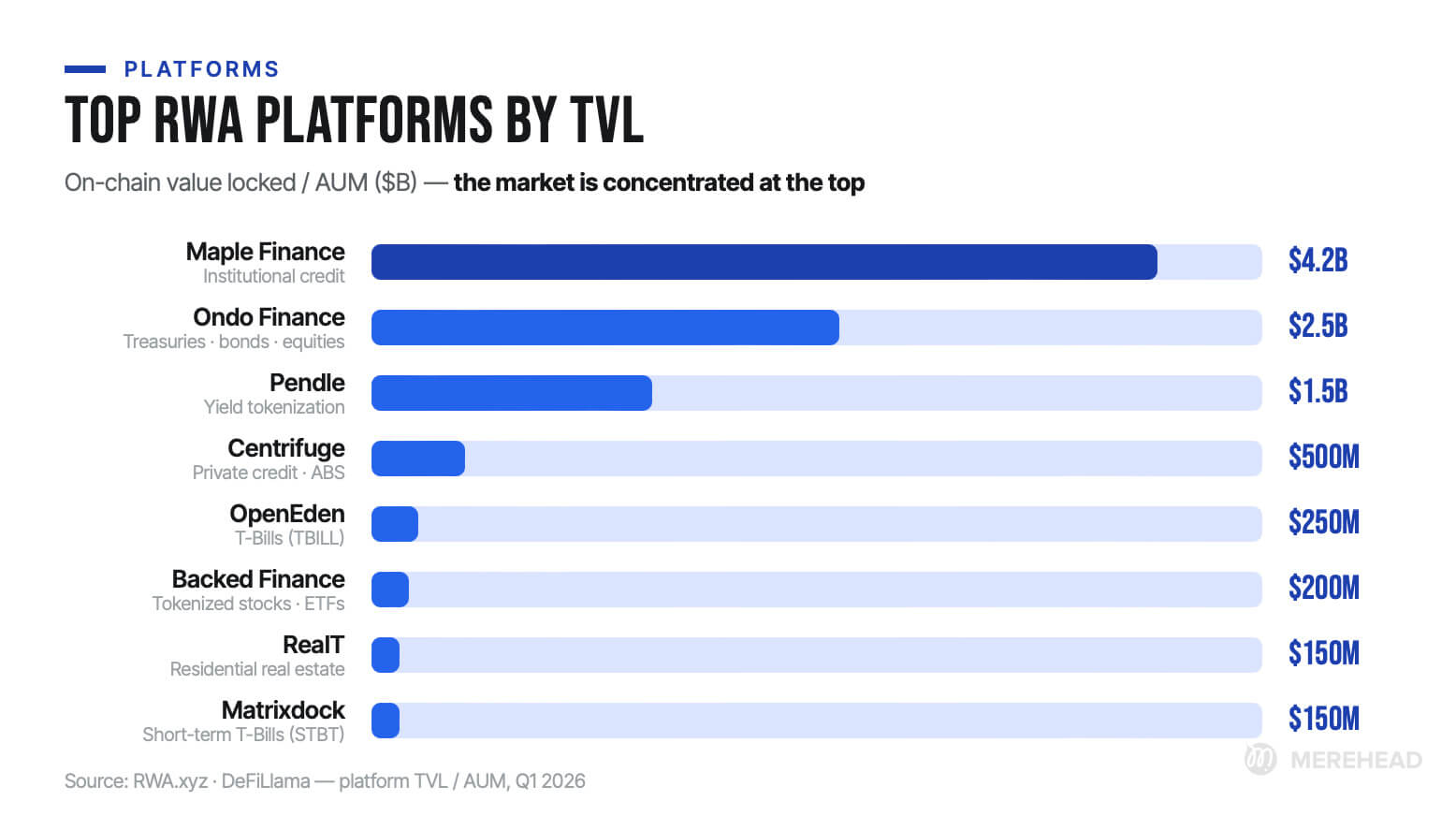

Top RWA Tokenization Platforms

Ten players account for the majority of measurable on-chain TVL. The market is concentrated at the top and diversified in the middle.

| Platform | TVL / AUM | Asset Types | Blockchain | Launch |

|---|---|---|---|---|

| Ondo Finance | $2.5B+ | US Treasuries, bonds, equities | Ethereum + 7 networks | 2021 |

| Maple Finance | $4.2B+ AUM | Institutional credit, syrupUSDC | Ethereum, Solana, Arbitrum | 2021 |

| Centrifuge | ~$500M | Private credit, invoices, ABS | Centrifuge Chain, Ethereum | 2017 |

| RealT | ~$150M | US residential real estate | Ethereum, Gnosis | 2019 |

| Backed Finance | ~$200M | Tokenized stocks, ETFs | Ethereum | 2021 |

| Pendle | $1.5B+ | Yield tokenization (RWA+DeFi) | Ethereum, Arbitrum | 2021 |

| OpenEden | ~$250M | T-Bills (TBILL token) | Ethereum | 2022 |

| Matrixdock | ~$150M | Short-term T-Bills (STBT) | Ethereum | 2023 |

Maple Finance posted 66.4% AUM growth in Q3 2025 — from $2.6B to $4.19B — at a 99% loan repayment rate, a rare figure for the institutional credit market. Ondo Finance grew from $40M TVL to $1.6B by September 2025, holding approximately 17% of the tokenized US Treasuries market.

Which Blockchains Dominate

Ethereum holds 60–70% of all tokenized RWA by TVL. The arguments are standard: EVM infrastructure maturity, DeFi ecosystem depth, the largest number of institutional integrations. But the picture is shifting. Ondo Finance is deployed on more than seven networks. Maple Finance runs pools on Solana and Arbitrum. BlackRock BUIDL was live on nine networks by November 2025.

Stellar maintains niche leadership in the MMF segment: Franklin Templeton BENJI holds the majority of its $846M AUM on this network, benefiting from low transaction costs and fast final settlement. Solana is gaining institutional share faster than any other alternative. Polygon and Arbitrum attract platforms with active secondary turnover where gas economics matter for small-transaction volume.

The practical implication for teams selecting infrastructure: multichain is no longer an optional feature for platforms targeting institutional capital — it is a baseline requirement. This directly mirrors what we built in our payment processing project, where the decision to support BTC, ETH, USDT (ERC-20 and TRC-20), Tron, Solana, and BNB Chain simultaneously was driven by the client's requirement to serve partners operating across different blockchain ecosystems. The architecture used independent blockchain connectors per network, each with its own node integration and wallet management logic — an approach that scales considerably better than a single-chain design retrofitted for multichain later.

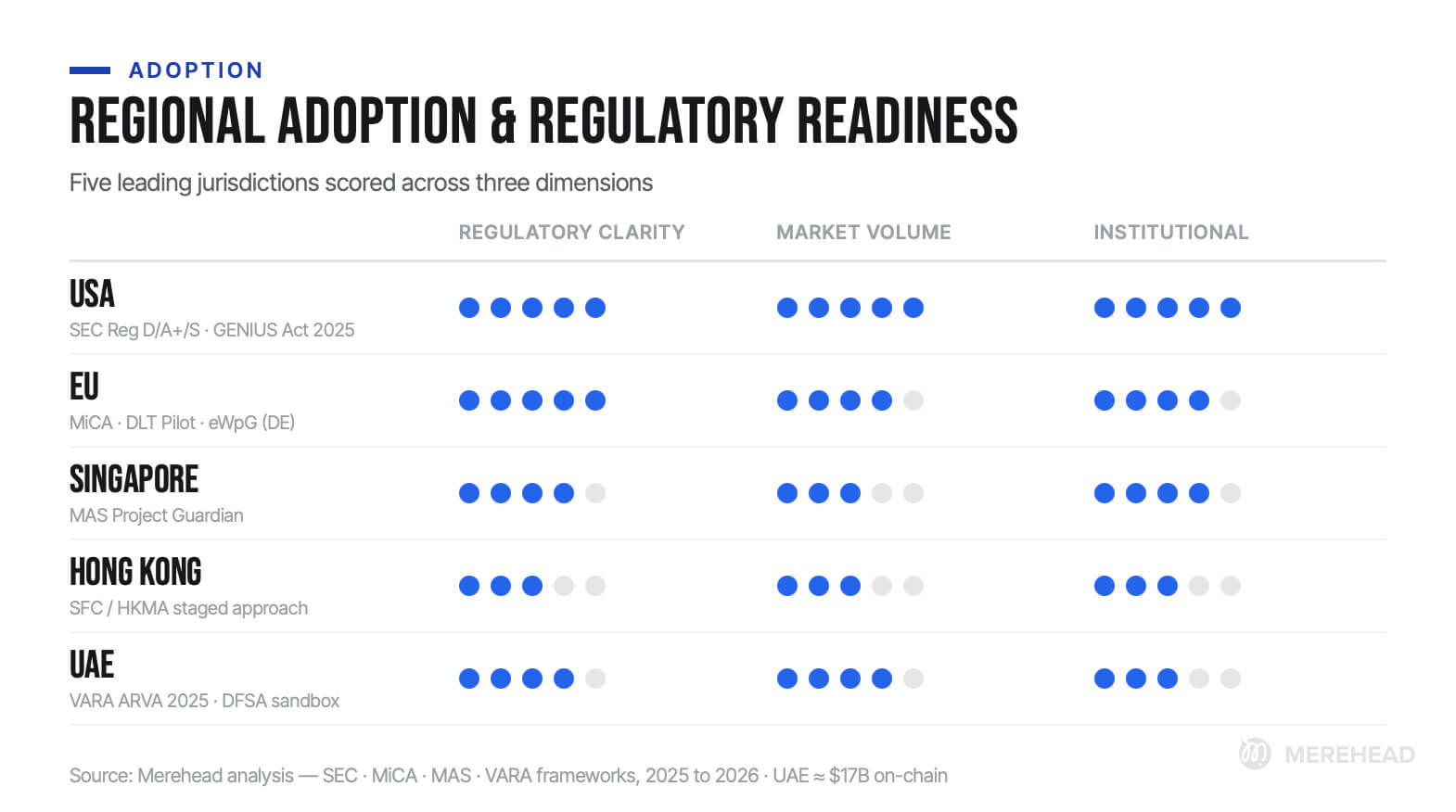

RWA Adoption by Region

Regulatory environment affects adoption velocity as much as technology.

Rules vary sharply across jurisdictions, materially complicating cross-border issuance planning.

| Region | Regulatory Framework | Key Players | RWA Volume / Status |

|---|---|---|---|

| USA | SEC Reg D/A+/S, GENIUS Act 2025 | BlackRock, Ondo, Securitize, JPMorgan | Largest market by AUM |

| EU | MiCA 2024, DLT Pilot Regime, eWpG (DE) | Siemens, SIX Digital Exchange, Backed Finance | Most mature legal framework |

| Singapore | MAS Project Guardian, MAS licenses | DBS, HSBC SG, DigiFT, iSTOX | APAC leader, cross-border pilots |

| Hong Kong | SFC/HKMA staged approach | HashKey, OSL, HKMA digital bonds | Institutional APAC hub |

| UAE (DIFC/ADGM) | VARA ARVA rules 2025, DFSA sandbox | DIFC fintech cluster (1,500+ firms), FAB | ~$17B on-chain RWA (2025) |

The US leads globally by institutional volume. JPMorgan processed over $1T in tokenized repo transactions through its Onyx platform in 2025. The DTCC announced production launch for tokenized securities in July 2026, with full deployment in October.

In Europe, MiCA, the DLT Pilot Regime, and ELTIF 2.0 together have formed a regulatory foundation that makes large-scale compliant tokenization practically viable for the first time. The pivotal 2026 decision — whether the European Commission converts the DLT Pilot Regime to a permanent mode — will substantially determine the pace of institutional rollout in the region.

The UAE has carved out a distinct niche. In May 2025, VARA introduced the Asset-Referenced Virtual Assets (ARVA) category — the world's first purpose-built legal status for tokenized real-world assets. On-chain value of UAE-linked tokenized RWA reached approximately $17B by end-2025; real estate leads that flow. The focus on Islamic finance and sharia-compliant structures creates a niche with minimal global competition. Teams targeting that market should read our dedicated guide on launching a crypto business in Dubai under VARA licensing.

Structural Barriers: What the Data Shows

Market growth does not mean structural barriers have disappeared. The 2025–2026 data identifies four persistent obstacles.

Regulatory fragmentation remains barrier number one. According to a CACEIS survey, 58% of asset owners named regulatory constraints as the primary obstacle to crypto asset investment. Despite progress in the US, Singapore, UAE, and Hong Kong, there is still no global harmonization of regulatory approaches. For institutions operating across multiple jurisdictions simultaneously, this translates directly into additional compliance costs.

Secondary market liquidity — the gap between declared TVL and actual trading activity. Academic research from Macquarie University based on rwa.xyz data found that most RWA tokens show low trading volumes, long holding periods, and limited investor participation despite theoretical 24/7 availability.

Smart contract security is becoming critical as institutional AUM grows. Token standards like ERC-3643 are advancing interoperability and compliance enforcement. Custodial solutions, AML/KYC integrations, and smart contract audits are becoming priority budget lines. This maps directly to our experience: in the real estate tokenization project we built, the compliance layer — investor whitelisting, 2FA, AML integration, anti-phishing protections — consumed a disproportionate share of both scope definition time and QA cycles. It was the correct prioritization.

Education gap is institutional, not just retail. Many investors remain unfamiliar with the technical risks of tokenized assets: smart contract exposure, custodial architecture, on-chain settlement mechanics. This reduces confidence in participation even when liquid instruments are available.

For teams building tokenization infrastructure, the implication is that compliance architecture is not a back-end detail — it is the product. Skimping on the compliance layer in the MVP to hit a launch date is one of the most reliable ways to require a full rebuild twelve months later.

RWA Forecasts: 2026–2030

There is no consensus number — and that is normal for an early-stage market where analysts measure fundamentally different things.

| Source | Forecast | Horizon | Publication Year |

|---|---|---|---|

| BCG + ADDX | $16.1T (business opportunity) | 2030 | 2022 |

| BCG + Ripple | $9.4T (demand); $18.9T by 2033 | 2030 / 2033 | 2025 |

| Standard Chartered | $30T | 2034 | 2023 |

| McKinsey & Company | $2–4T | 2030 | 2024 |

| BlackRock (Larry Fink) | $10T | 2030 | 2024 |

| Ark Invest | $11T+ | 2030 | 2026 |

| TD Cowen | up to $100T (all on-chain assets) | 2030 | 2025 |

BCG's updated projection with Ripple (2025) presents a more moderate but defensible trajectory: demand for tokenized RWA reaching ~$9.4T by 2030 and approximately $19T by 2033 — around 10% of global GDP. BCG identifies three phases: low-risk adoption (MMF, corporate bonds), institutional expansion (private credit, structured finance), and broad penetration into real estate and the real economy.

Every forecast — from McKinsey to Standard Chartered — agrees on two baseline conditions. First: regulatory clarity in key jurisdictions (permanent DLT Pilot regime in EU, federal security token framework in the US, cross-APAC standard alignment). Second: technological maturity — cross-chain interoperability, token standardization around ERC-3643, and reliable custodial infrastructure for institutional-grade products.

McKinsey's lower-bound estimate of $2T implies a 65x increase from current on-chain TVL. Even the most cautious analyst is betting on an order-of-magnitude market expansion.

Building RWA Tokenization Platforms: Technical and Cost Reality

Market statistics are useful for sizing the opportunity. For teams building into that opportunity, what matters more is what an RWA platform actually consists of — and what it costs.

The technical stack is built on four layers:

Tokenization layer — smart contracts to ERC-3643 or ERC-1400 standards with compliance rules enforced at the code level, mint/burn logic, and investor whitelist management.

Compliance layer — KYC/AML integrations (Onfido, Chainalysis KYT), automated transfer restrictions, regional investor restrictions. In both projects we described above — the real estate platform and the crypto payment processor — the compliance layer was the single most scope-intensive component. In the payment processing project, AML logic for incoming transactions included risk-level assessment and return routing for high-risk operations without significant financial cost to the business. That is a non-trivial engineering problem that looks deceptively simple in a feature list.

Oracle integration — price feeds and verified off-chain asset valuation data (Chainlink, RedStone, API3). Without reliable oracles, neither correct pricing nor liquidation triggers are possible.

Custody layer — institutional-grade private key storage (Fireblocks, Anchorage, Copper) or multi-sig for lower-capital projects.

| Platform Tier | Budget Range | Timeline | Scope |

|---|---|---|---|

| Compliant MVP | $120K–$250K | 10–16 weeks | Single asset class, single jurisdiction, core feature set |

| Mid-tier platform | $250K–$500K | 4–6 months | Multiple asset classes, extended compliance, admin panel |

| Enterprise-grade | $500K–$1M+ | 6–12 months | Multichain, integrated secondary market, institutional audit |

| Legal & compliance overhead | $200K–$800K | Parallel track | Legal structuring, SPV/LLC setup, regulatory filings |

Smart contract audits and legal compliance frequently form the largest single cost item on an enterprise-grade project. This is not padding — it reflects the genuine complexity of structuring an asset correctly as a security, selecting the right legal wrapper, and ensuring the compliance logic in the smart contract actually mirrors the legal obligations. On a real estate tokenization platform specifically, the admin panel architecture — controlling token valuation per property, managing rental income distribution, administering investor KYC and wallet controls — is meaningfully more complex than it appears in a requirements document.

For teams evaluating whether to build or adapt an existing solution, the white-label tokenization platform route compresses the initial timeline at the cost of customization flexibility. The right answer depends on asset class, jurisdiction, and whether the platform is the product itself or the infrastructure behind a financial product. Teams building the latter often find that a commercial real estate tokenization deep-dive provides more applicable reference points than generic blockchain platform guides.

Conclusion: What the Statistics Mean

The data assembled here converges on several durable conclusions.

On-chain TVL grew 266% in 2025 and added another 66% from the start of 2026. The holder base for tokenized US Treasuries grew from 13,000 to 55,000–60,000 during 2025; the total RWA owner base expanded from 90,000 to 500,000–600,000. Institutional validation is complete: BlackRock, Franklin Templeton, and JPMorgan are in production mode. Regulatory frameworks in the EU, Singapore, and UAE have moved from sandbox experiments to permanent regimes.

RWA is forming as the third pillar of digital assets — alongside stablecoins and "pure crypto" — and currently shows low correlation to the volatility of the latter. The central open question is not whether scaling will happen, but which infrastructure will become the standard: multichain architecture, ERC-3643, institutional custody, and compliant secondary markets.

Market participants converge on one reading of 2026: it is the year of proof, where products with reliable pricing, real liquidity, and clean operational rails survive.

FAQ

What is the current size of the RWA tokenization market?

The tokenized RWA market is approaching $30B on-chain per DeFiLlama data, with $2.47B of that constituting active DeFi TVL deployed in lending and collateral protocols. RWA.xyz's broader methodology, which includes permissioned registries, measured ~$27.5B TVL at end of Q1 2026. The market has grown 66% since the start of 2026, confirming the durability of institutional demand.

What will the RWA tokenization market be by 2030?

Forecasts range from $4–5T (Citi GPS, conservative) to $10T (BlackRock), $16T (BCG), and $30T (Standard Chartered). The spread reflects different definitions of "tokenizable assets" — narrow counts only regulated financial instruments; broad includes real estate, infrastructure, and commodities. All forecasts require regulatory clarity and infrastructure maturity as preconditions.

Which assets can be tokenized?

Practically any asset with measurable value and a legal basis. Funds, commodities, private credit, and tokenized equities account for over 95% of the RWA sector. The most mature classes are US Treasuries (~$16.6B on-chain) and private credit (~$9.5B). Real estate, art, and infrastructure are at earlier stages with higher regulatory complexity.

Which blockchain is best for RWA tokenization?

Ethereum dominates with 60–70% share by TVL. However, the market is moving toward multichain architecture: tokenized funds are deployed on Ethereum, Solana, Avalanche, and BNB Chain simultaneously, with Solana and Avalanche gaining institutional share fastest. Stellar remains the preferred network for MMF products. For new platforms, designing for multichain from the start is now a baseline expectation.

Is RWA tokenization legal?

In most key jurisdictions — yes, subject to applicable securities law. In the US: Regulation D/A+/S. In the EU: MiCA 2024 and DLT Pilot Regime. In Singapore: MAS licenses. Tokenization does not change the legal nature of the underlying asset — only its representation. Compliance obligations remain fully in force, and the legal wrapper (LLC, SPV, trust) determines what rights token holders actually have.

How much does it cost to build an RWA tokenization platform?

Based on 2026 market data: a compliant MVP costs $120K–$250K over 10–16 weeks; a mid-tier platform runs $250K–$500K; an enterprise-grade solution with full compliance stack starts at $500K and can exceed $1M. Legal structuring and regulatory filings add $200K–$800K on enterprise projects. Budget and architecture depend heavily on asset class, jurisdiction, and secondary market model.