- A white label centralized exchange (CEX) is a pre-built, production-tested trading platform you license, rebrand, and deploy — instead of building from scratch over 12–18 months.

- A production-ready white label CEX includes spot trading, margin, futures, an instant conversion module, admin panel, KYC/AML compliance, and liquidity integrations — not just a trading UI.

- The fastest documented deployment timeline from contract to live platform is under two weeks — achievable only when the base product is mature and the deployment process is documented.

- White label reuse reduces costs by 60–80% compared to custom development and eliminates core trading mechanics risk.

- The primary technical challenges — cold-start liquidity, infrastructure scaling, KYT compliance, and blockchain node sync timing — must be addressed at the architecture stage, not post-launch.

Most teams that set out to build a crypto exchange from scratch discover the same hard truth around month four: what looked like a trading platform is actually a distributed financial infrastructure project. The order book, matching engine, wallet accounting, liquidation mechanics, KYC/AML stack, admin panel, and liquidity layer are six separate engineering domains — each with its own failure modes. A white label centralized exchange solution doesn't eliminate this complexity. It shifts it from the "build" column to the "configure and extend" column, which is an entirely different risk profile.

This article covers what a production white label CEX actually contains, the architectural decisions that determine whether it will scale, the compliance integrations that regulators will check first, and the liquidity problem that kills more new exchanges than any other single factor. All observations are drawn from real deployments.

What "White Label CEX" Actually Means at the Engineering Level

The term is marketing shorthand for a specific technical arrangement: a codebase that has been built, tested, and deployed in production, then forked and reconfigured for a new operator. The trading logic, matching engine, and compliance flows are shared across deployments. The operator-specific layer — branding, payment gateway credentials, domain, fee structures, supported assets — sits on top.

A white label centralized exchange is not a template. It is a production system with an operator configuration layer. The distinction matters because "template" implies you're starting from mockups; "production system" means the order matching, wallet accounting, and liquidation logic have already been tested with real money on real networks.

In practice, the depth of what's included varies enormously between vendors. A superficial white label gives you a trading UI. A serious one gives you a platform architecture that has already answered questions like: how do you prevent double-spend on concurrent withdrawal requests? How does the liquidation engine behave when the price feed drops for 200 milliseconds? What happens to pending limit orders when a blockchain node falls behind by three blocks?

When evaluating any white label crypto exchange solution, the right questions aren't about UI features — they're about what production incidents the base platform has already encountered and resolved.

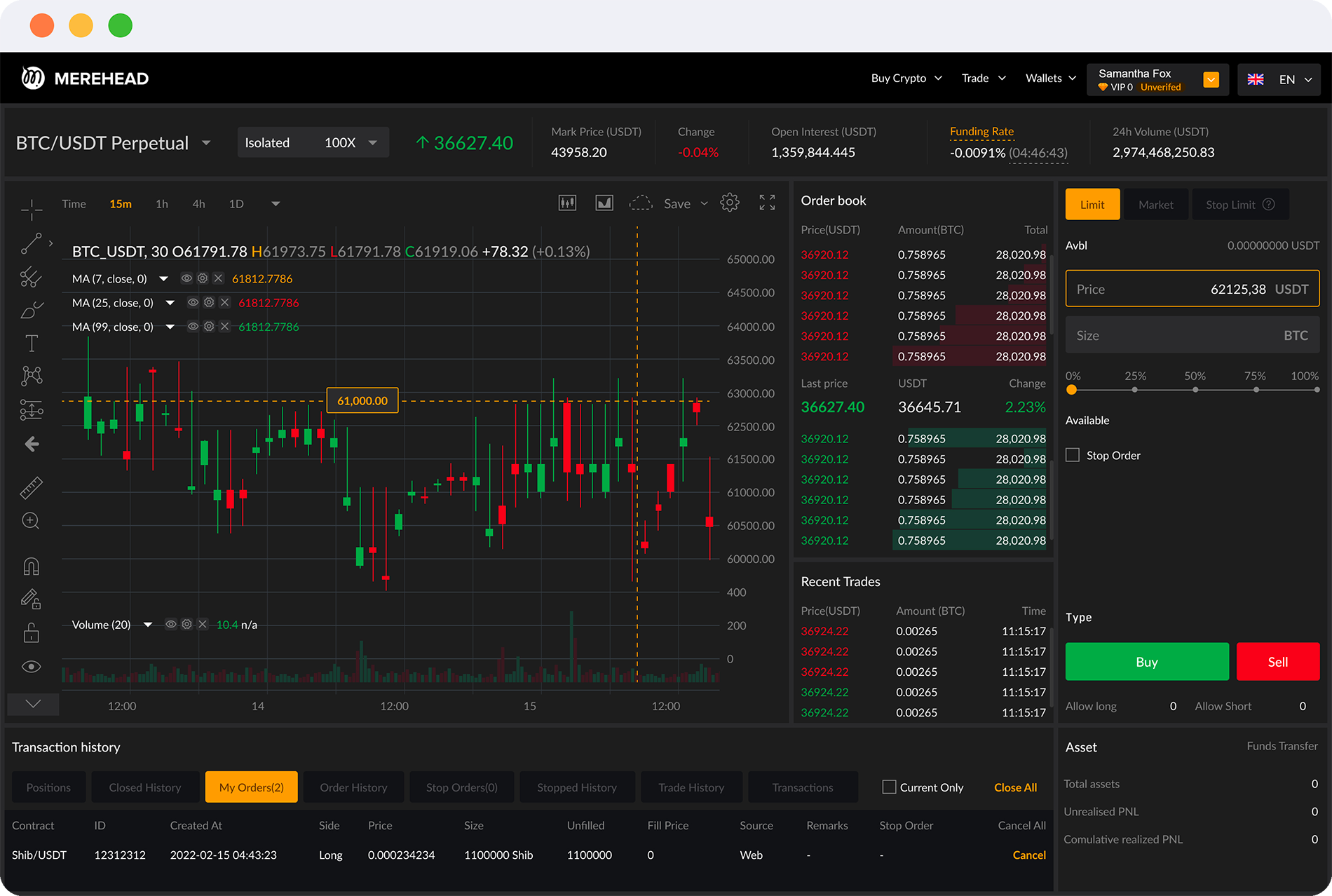

Module Architecture: What a Complete CEX Contains

In one of our large-scale exchange deployments, the final platform consisted of six distinct trading modules, each with separate order management logic, wallet accounting, and liquidation mechanics:

| Module |

Core Technical Function |

Key Complexity |

| Spot trading |

Limit/market order matching, order book management |

Matching engine throughput, order book depth display |

| Margin trading |

Leveraged positions with auto-liquidation |

Real-time margin ratio calculation, liquidation cascade prevention |

| Futures (B-book) |

Perpetual/fixed-term contracts, funding rate |

Internal counterparty risk management, funding rate settlement |

| Options |

Black-Scholes pricing, expiry settlement |

Greeks calculation engine, expiry batch settlement |

| Instant conversion |

Market-rate asset swap, no order book |

Rate locking, slippage control, external liquidity routing |

| Admin panel |

User management, fee configuration, compliance tools |

Granular role permissions, AML review queue, forced wallet ops |

The base platform without custom extensions takes 2–4 months to configure and deploy. Brand adaptation alone — applying colors, logo, and typography to the existing UI — takes 2–3 weeks. These timelines assume infrastructure is already provisioned. If it isn't, add more.

The critical architectural principle: plan for extensions from day one. One of our exchange clients added the following modules over 6–12 months post-launch that weren't in the original scope: multi-tier VIP account structures, AML-triggered forced wallet resets, per-user custom commission structures, OKX liquidity mirroring on the spot market, overdraft functionality, and fiat overnight staking with per-currency interest rates configurable by admin.

Adding fiat staking to an exchange that wasn't designed for fiat accounting is expensive. Adding it when the original microservices architecture anticipated it is a matter of weeks. The difference is entirely in the initial architecture decision — not in the feature itself.

The Infrastructure Layer: Kubernetes, Microservices, and Scaling Policy

A white label CEX is only as good as its infrastructure. In one of our production deployments, we migrated the platform from a monolithic virtual machine setup to full Kubernetes orchestration as part of the go-live preparation. The scope:

- 17 microservices rewritten as Docker containers

- Helm charts for declarative deployment

- HashiCorp Vault for secrets management, integrated with GitLab CI pipelines

- Horizontal Pod Autoscaler configured per service

- Redpanda (Kafka-compatible) message bus for inter-service communication

The part that consistently trips up teams new to exchange infrastructure: not all services should autoscale horizontally. Order book services and wallet services have state dependencies that make horizontal scaling non-trivial. Adding a second instance of a wallet manager without distributed locking creates a race condition on concurrent withdrawal requests. Adding a second matching engine instance without a shared state mechanism splits the order book.

Before writing a single Helm chart, define your scaling policy: which services are stateless (API gateway, notification service, rate feed aggregator) and which are stateful (wallet manager, matching engine, liquidation engine). That policy determines your entire infrastructure design.

Stateless services can scale horizontally under load without coordination overhead. Stateful services need a different approach: vertical scaling, leader election, or purpose-built distributed state management. Defining this before writing infrastructure code saves significant rework — and prevents the class of production incident where autoscaling creates more problems than the load spike it was responding to. For a technical deep-dive on how matching engines function at scale, the mechanics of matching engine architecture explained from Rust code to 1M+ TPS is directly relevant here.

Blockchain Node Integration: The Timeline Killer

Blockchain node integration is consistently one of the most underestimated items on a crypto exchange project plan. In our deployments, we work with Bitcoin, Ethereum, Litecoin, Tron, and BNB Smart Chain nodes. Synchronization times differ dramatically:

| Blockchain |

Full Node Sync Time |

Hardware Requirement |

| Bitcoin |

5–10 days |

Dedicated hardware required; shared infra adds time |

| Ethereum |

2–4 days |

High IOPS SSD required for state db |

| BNB Smart Chain |

1–3 days |

Snapshot sync available; reduces to hours |

| Tron |

1–3 days |

Standard dedicated server |

| Litecoin |

1–2 days |

Standard dedicated server |

This has a direct impact on project timelines. If node sync isn't started on day one of the project — in parallel with development, not sequentially after — you will reach the end of development and be waiting on Bitcoin. We've seen this delay production launches by a week or more. Our standard practice is to spin up nodes in the first week of any crypto project, regardless of whether integration work has started.

The Cold-Start Liquidity Problem

A new centralized exchange without liquidity is a dead product from day one. This is the single most common reason white label CEX deployments fail in the market within the first 90 days — not the technology, but the empty order books that drive away the first users who will never return.

The liquidity problem is architectural, not operational. You cannot solve it post-launch with a marketing budget. It must be addressed in the platform design before the first user registers. The two viable approaches are: connecting external liquidity providers via API, or implementing order book mirroring from a major exchange. Each has different tradeoffs on cost, complexity, and operational risk.

In one of our deployments, the client implemented a sophisticated OKX order book mirroring model for the spot market. The flow: when a user places a sell order, the system simultaneously borrows the equivalent amount on OKX (3x margin), executes the sell on OKX's market, credits the user's USDT balance, then settles the OKX borrow when funds are available. From the user's perspective, they see a live order book from day one — because it is backed by OKX's actual depth.

The operational requirements of this model are significant and non-negotiable:

- Real-time monitoring of OKX margin utilization (failure = user trades fail)

- Borrow limit tracking per asset (exceeding limits means orders can't be filled)

- USDT collateral position monitoring (under-collateralization triggers forced closure)

- Alerting on all critical thresholds via Telegram and Slack with automated escalation

The tradeoff is clear: you get populated order books on day one at the cost of operational complexity that requires dedicated monitoring infrastructure. For an independent assessment of the top providers worth integrating, the comparison of top crypto liquidity providers with pros and cons covers the major options and their technical integration requirements.

KYC/AML Integration: What Production Compliance Actually Looks Like

Most white label exchange descriptions list "KYC integration" as a feature bullet. What that phrase covers in practice ranges from a basic ID upload flow to a dual-path verification system with two separate state machines in the backend, each handling different webhook payloads and status transitions from different providers.

In our production deployments, we implement KYC through SumSub as the primary provider with dual-path architecture: mobile identity app verification for local users alongside standard document upload for international users. These are not two configurations of the same flow — they are two separate verification state machines in the backend, because each provider has different webhook payloads, different failure modes, and different status transitions.

KYT (Know Your Transaction) is the compliance layer that most exchanges add as an afterthought — and regulators check first. In production, KYT is wired to every inbound deposit without exception: each transaction receives an AML risk score before the balance is credited to the user's account. When a risk score exceeds the configured threshold, the system creates an admin review task and freezes the deposit.

The user does not see their balance update until a compliance officer explicitly clears the transaction. This is fundamentally different from checking KYC once at registration and trusting all subsequent deposits — which is the approach that generates regulatory sanctions.

A more sophisticated AML feature we've built for several clients is forced wallet regeneration triggered by a risk event. When a deposit address is flagged — by the AML scoring system or manually by a compliance officer — the system automatically generates new deposit addresses for that user across all supported networks and retires the flagged address. Any future deposits to the old address are quarantined. This breaks the association between the user's identity and a potentially compromised address without revealing the compliance trigger.

The compliance infrastructure also has a direct dependency on the blockchain integrations described above. KYT scoring on a Bitcoin deposit requires confirmed transaction data from the Bitcoin node — which means your KYT system is only as reliable as your node's sync status. Compliance and infrastructure are not separate engineering tracks on a crypto exchange; they share critical dependencies.

White Label Deployment: The Real Process and Timeline

The fastest deployment we've executed took under two weeks from contract signing to live platform. This is not a marketing claim — it's what becomes technically possible when the base product is mature, the deployment process is documented, and the client has no custom feature requirements beyond branding and payment gateway configuration.

The actual deployment sequence:

- Fork existing production codebase to client-dedicated repository

- Apply client's design tokens: colors, logo, typography across all UI components

- Replace API credentials for all third-party services (payment processor, SMS provider, email service, trading data feeds)

- Configure payment gateway keys and test deposit/withdrawal flows

- SSL configuration and domain binding

- Run smoke tests across all critical user flows: register → KYC → deposit → trade → withdraw

- Hand over admin credentials and operations documentation

The trading logic, affiliate system, admin panel, and compliance flows are identical across all deployments. The business case is straightforward: clients pay for configuration, customization, and the engineering work invested in the base over years of production operation. The white label reuse model cuts their cost by 60–80% compared to building from scratch and eliminates risk on core trading mechanics — which is where the most expensive bugs live.

Two weeks to live platform is only possible when the deployment process is documented to the point where it's repeatable. The moment a deployment requires ad-hoc decisions, the timeline doubles. Documentation is not an afterthought in white label operations — it's the product.

For a detailed cost breakdown of what goes into a white label deployment versus custom development, the complete white label crypto exchange cost pricing guide covers each component with current market rates.

The Three Technical Blockers That Delay Most Launches

Based on our delivery experience across multiple exchange projects, the blockers that push go-live dates are almost never code problems. They are infrastructure timing problems and client-side coordination failures.

1. Production access delays. Development can be complete and staging tests passing, but if the client's team hasn't provisioned production server credentials and infrastructure access, launch waits. We've seen this add two to three weeks to otherwise finished projects. The fix is contractual: infrastructure readiness milestones must be explicit client deliverables with dates, not assumptions.

2. Bitcoin node sync. Bitcoin full node synchronization takes 5–10 days on modern hardware. If it isn't started on project day one, it becomes the critical path item blocking go-live. Ethereum, Tron, and BNB Smart Chain sync in 1–3 days and are generally not the constraint. Bitcoin always is, unless you start it first.

3. Non-deterministic test failures in crypto environments. Crypto transactions depend on network state — fee levels, mempool congestion, confirmation counts. Test cases that pass in the morning fail in the afternoon because network conditions changed. This is not a bug in your test suite. It's the nature of decentralized networks. Test suites for exchange platforms must distinguish between infrastructure failures and application bugs — they require different remediation paths.

The fourth blocker that rarely appears on project plans but derails timelines just as effectively: fiat banking integration. SEPA instant vs SEPA standard settlement windows have different accounting implications. A deposit flow that treats "payment initiated" and "funds confirmed" as the same event will create reconciliation problems that are painful to fix after go-live.

If your exchange supports fiat on/off-ramp — and most white label deployments targeting US or EU users will — the fiat accounting model needs to be designed correctly from the start. Retroactively separating pending fiat deposits from confirmed crypto balances in a live production database is a complex migration under operational conditions.

Security Architecture: What White Label Inherits and What It Doesn't

A white label CEX inherits the security architecture of its base platform. This is a significant advantage if that architecture was designed correctly — and a significant liability if it wasn't. The areas where production exchanges most commonly experience security incidents fall into two categories: key management and withdrawal authorization.

Key management on a production exchange means hot wallet private keys never exist in plaintext on application servers. The standard architecture uses HSM (hardware security module) or a software equivalent like HashiCorp Vault with hardware-backed seal keys, with all signing operations happening inside the secure boundary. Application servers request signatures; they never hold keys. If a white label provider's architecture allows application servers to hold decrypted private keys in memory during normal operation, that is a fundamental design flaw — not a configuration choice.

Withdrawal authorization should enforce multi-step confirmation for amounts above configurable thresholds: user initiates, system validates against AML/KYT, second admin confirmation for large amounts, time-delay on first-time destination addresses. Each step is a separate database transaction with an audit log entry. Bypassing any step should require explicit override with logged justification. An exchange's withdrawal flow is the most attacked surface by both external actors and insider threats — the authorization model must be designed to withstand both threat vectors. The comprehensive treatment of crypto exchange security in 2026 covers the full threat model and mitigation architecture in detail.

Customization Roadmap: What Clients Actually Add Post-Launch

Based on our experience across multiple exchange deployments, the features that appear in post-launch roadmaps consistently fall into five categories. None of these should surprise an architect, but all of them should be anticipated in the initial system design:

| Feature Category |

Specific Examples from Deployments |

Architectural Dependency |

| Account tier system |

VIP tiers with reduced fees, higher withdrawal limits, dedicated support queue |

User model must support extensible tier attributes; fee engine must read tier context |

| Liquidity depth |

OKX/Binance mirroring, additional LP API connections, per-pair routing rules |

Liquidity abstraction layer must support multiple simultaneous providers with routing logic |

| Fiat functionality |

Overnight staking of fiat balances, per-currency interest rates, SEPA direct debit |

Accounting model must separate fiat and crypto balance types from day one |

| Compliance hardening |

Forced wallet regeneration on AML flag, transaction scoring thresholds per asset |

AML system must be event-driven with configurable action triggers, not batch-only |

| Commercial features |

Custom per-user commission structures, referral programs, API access for institutional clients |

Fee and commission model must be user-level configurable, not platform-level only |

The pattern is consistent: features that seem straightforward to add post-launch become expensive migrations when the initial architecture didn't anticipate them. An exchange that was designed assuming all users have the same fee structure will require a significant refactor to support per-user commissions. An exchange with a single balance type will require schema migration and accounting logic rewrites to support separate fiat and crypto balance treatment.

Comparing White Label CEX to the Alternatives

The decision to use a white label CEX solution typically comes down to a comparison against three alternatives: building from scratch, using open source exchange software, or launching a DEX instead of a CEX.

Build from scratch is the highest-cost, highest-risk option. Timeline: 12–18 months for a serious CEX with the modules described above. Cost: $500K–$1.5M+ depending on team location and scope. Risk: every component — matching engine, wallet system, KYC integration, liquidation engine — is being built for the first time, with no production history. The first production incidents will be novel, with no institutional knowledge of how to resolve them. For founding teams without deep exchange engineering experience in-house, this is rarely the rational choice.

Open source exchange software occupies a middle position. The codebase is available, but production support, security patches, and feature development are your responsibility. The hidden cost of open source in financial infrastructure is maintenance: you own every CVE, every upgrade, every incompatibility between dependencies. For teams with strong engineering capacity and a preference for full code ownership, it's viable. For teams optimizing for time to market, the operational overhead is underestimated.

Decentralized exchange (DEX) is architecturally different enough that the comparison requires clarification. A DEX eliminates the custodial risk of a CEX and removes the need for a KYC infrastructure stack — but it introduces smart contract risk, gas fee UX problems, and liquidity fragmentation across chains. For a business targeting institutional or regulated market users who need fiat on-ramps, a CEX is the correct architecture. For a DeFi-native audience, a DEX or hybrid model may be more appropriate. The architectural tradeoffs between building a centralized crypto exchange versus a DEX ultimately depend on your regulatory environment and target user profile.

Regulatory Considerations for White Label CEX Operators

A white label solution handles the technical compliance infrastructure — KYC flows, KYT scoring, AML action triggers, audit logs. It does not handle regulatory licensing, which is an entirely separate track and entirely the operator's responsibility.

In the US market, operating a centralized exchange that facilitates crypto-to-fiat transactions typically requires registration as a Money Services Business (MSB) with FinCEN, plus state-level Money Transmitter Licenses (MTL) in each state where you onboard users. The MTL licensing process in major states (New York, California, Texas) is measured in months to over a year. This licensing timeline must run in parallel with technical development — not after it.

The technical KYC infrastructure your white label provides — user identity verification, document storage, transaction monitoring — must be configured to meet the specific requirements of your licensing jurisdiction. A KYC configuration appropriate for an EU VASP may not satisfy New York's BitLicense requirements on customer due diligence depth. Review the technical KYC configuration with a crypto-specialized compliance attorney before onboarding users in any regulated jurisdiction.

Summary: What to Verify Before Signing a White Label Agreement

The white label CEX market has a wide quality spectrum. Before committing to any vendor, verify the following at the technical level — not the sales level:

- Production deployments: Ask for references from live exchanges running on their base platform, with verifiable transaction volume. A platform that has never been in production is not a white label — it's a prototype.

- Matching engine performance: Get specifics on throughput (orders per second), latency at P99, and the architecture of the matching engine (in-memory vs database-backed, language, concurrency model).

- Wallet security model: Confirm that private keys never exist in decrypted form on application servers. Ask specifically how the hot wallet signing infrastructure is designed.

- KYT integration: Verify that KYT scoring runs on inbound deposits before balance crediting — not as a batch job after the fact.

- Infrastructure ownership: Confirm whether you will run the platform on your own infrastructure or the vendor's. For a regulated operator, running on vendor infrastructure creates third-party risk that most regulators will ask about.

- Source code access: For any platform you intend to operate long-term, escrow access to source code is non-negotiable. A vendor relationship that ends should not mean your exchange goes dark.

A white label centralized exchange solution is a risk management decision as much as a cost decision. The 60–80% cost reduction is real. So is the risk reduction on core trading mechanics that have already been tested in production. The remaining risk — liquidity, compliance, infrastructure operations, and the extension roadmap — is yours to manage. Understanding that division of responsibility before signing is what separates a successful white label launch from an expensive lesson in misaligned expectations.

FAQ

How long does it actually take to launch a white label CEX?

The technical deployment, if you have no custom feature requirements, can be completed in under two weeks: forking the base codebase, applying branding, connecting payment gateway credentials, SSL/domain configuration, and smoke testing. In practice, most launches take 4–8 weeks because of client-side dependencies: provisioning production infrastructure, completing payment processor onboarding, and finalizing the regulatory/compliance configuration for the target market. The technical work is rarely the critical path.

What is included in "liquidity" for a white label exchange?

Liquidity configuration means connecting the exchange to one or more external liquidity providers via API, so that the order book shows live bids and offers from day one rather than being empty. The standard approach is connecting to two providers simultaneously (typically major exchanges with public APIs) and configuring routing rules per trading pair. More advanced setups implement order book mirroring with margin borrowing, which populates the order book with the depth of a major exchange. The configuration must include real-time monitoring of provider connectivity, rate feed health, and — if using the mirroring model — margin utilization and collateral positions.

Can a white label CEX handle margin trading and futures out of the box?

A production-grade white label CEX should include margin trading with configurable leverage, auto-liquidation mechanics, and either a perpetual or fixed-term futures module. However, confirm that these are genuinely functional modules with separate accounting and liquidation logic — not UI mockups over a basic spot engine. Ask the vendor specifically: how does the liquidation engine prevent cascades during rapid price moves? What is the B-book model for futures and how is internal counterparty risk managed? If those questions produce vague answers, the modules are not production-ready.

What's the difference between white label CEX and a Binance clone script?

A "clone script" is typically an unlicensed copy or reverse-engineered replica of an existing exchange's frontend, sometimes with basic backend functionality. It carries legal risk (IP infringement), lacks production history, and is rarely maintained beyond the initial sale. A legitimate white label CEX is a product built and maintained by a development company, deployed across multiple clients, with ongoing support, security updates, and documented deployment processes. The deployment speed may be similar; the risk profile and long-term operational quality are entirely different.

How much does a white label centralized exchange solution cost?

Pricing structures vary significantly: some vendors charge a one-time license fee ($30K–$150K+ depending on module scope), others charge a monthly SaaS fee ($3K–$15K/month), and some combine an upfront setup fee with revenue sharing. Custom features, additional trading modules, and compliance configurations are typically priced separately. The cost comparison that matters is not license fee vs license fee — it's total cost of ownership including ongoing infrastructure, maintenance, and feature development, compared against the 12–18 month build timeline and $500K–$1.5M cost of building from scratch.