Startups and businesses are increasingly moving away from traditional bank loans and choosing alternatives — peer-to-peer lending, equity crowdfunding, and real estate tokenization. The global P2P lending market was valued at approximately $139.8 billion in 2024 and is projected to reach $1.38 trillion by 2034, expanding at a CAGR of 25.73%. In the US specifically, the sector is forecast to grow from $8.33 billion in 2026 to $33.8 billion by 2034.

For entrepreneurs and fintech companies, this creates a real opportunity: launching your own P2P lending platform that brings investors and borrowers together. But "P2P lending platform software" covers a wide range of technical architectures and regulatory models — from simple consumer loan marketplaces to DeFi-native lending protocols. This guide covers what a production-ready system actually includes, which business model fits your goals, what US regulations apply, and what realistic development costs look like in 2026.

What Is P2P Lending Platform Software?

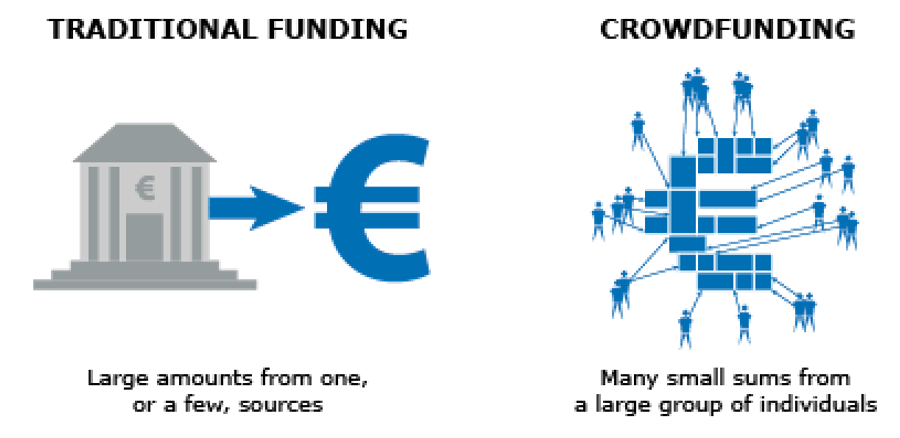

How lending platform software worksA P2P lending platform is a marketplace, not a banking app. Unlike a bank that holds deposits and issues loans from its own balance sheet, P2P lending software manages the rules, risk logic, compliance workflows, and transaction flows between two independent parties — borrowers and lenders. The platform never owns the capital; it facilitates its movement.

The general scheme: a borrower applies through the platform and provides identity and financial documentation → the platform scores their creditworthiness and publishes a loan offer → investors fund the loan in full or in fractional shares → the platform disburses funds to the borrower and manages repayment collection → principal and interest are distributed to lenders pro-rata.

Lending platform types

The models of such sites differ in purpose and monetization:

- Debt financing (P2P lending). Borrowers take loans directly from investors, bypassing bank intermediaries. Types of loans vary: personal, SME, real estate, student refinancing. The volume of this niche in the US was $8.33 billion in 2026, growing rapidly.

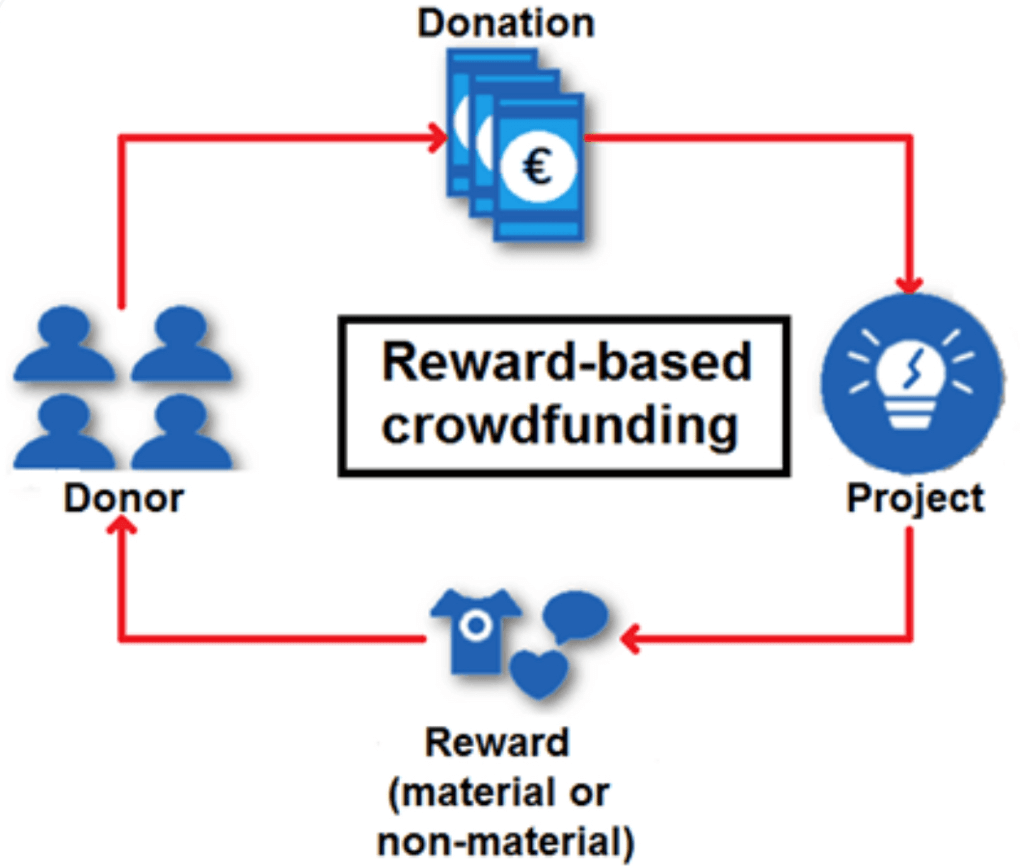

- Reward-based financing. Investors fund projects in exchange for a predetermined reward — a product, service, or acknowledgment — rather than financial returns. Volume was estimated at $1.42 billion in 2023. Primarily used for creative and educational projects.

- Investment financing / equity crowdfunding. Individuals or companies invest in exchange for equity shares or profit participation. Real estate tokenization marketplaces are one popular option. Volume was estimated at $13.34 billion in 2023.

What Are the Obligations of P2P Lending Platforms?

P2P lending platforms act as intermediaries and guarantors of transaction compliance. All platforms must operate within the laws of the jurisdictions where they provide services: in the US — the SEC, FTC, FINRA, and CFPB; in Germany — BaFin; in the UK — FCA; in Europe broadly — ECSPR regulations.Three Business Models for P2P Lending Platforms

Before writing a line of architecture, you need to decide which P2P lending model you're building — each one has different technology requirements, regulatory obligations, and operational complexity.| Centralized | Decentralized (DeFi) | Hybrid | |

|---|---|---|---|

| Intermediary | Platform | Smart contract | Both |

| Credit scoring | Platform-managed | Collateral-based | Platform-managed |

| Regulatory burden | High (SEC/FINRA/CFPB) | Evolving/uncertain | Medium |

| Operational cost | Higher | Lower | Medium |

| Fraud protection | Managed by platform | Smart contract logic | Managed + on-chain |

| Best for | US consumer / SME lending | Crypto-native, DeFi users | Balanced approach |

Centralized P2P Lending: the platform acts as intermediary — setting credit rules, managing borrower-lender matching, handling escrow, and running compliance workflows. LendingClub and Prosper operate this way. Full regulatory responsibility falls on the platform operator: SEC, FINRA, CFPB oversight depending on loan types. This is the practical starting point for most US fintech startups.

Decentralized P2P Lending (DeFi): loans execute via smart contracts on a blockchain. No central authority — borrowers and lenders interact directly through the protocol. Aave and Compound demonstrate this model. Smart contracts can automate origination, disbursement, and repayment collection, reducing operational costs significantly. The US regulatory status for DeFi lending is still evolving.

Hybrid Model: centralized compliance and customer support combined with blockchain-based transaction execution for transparency. This is increasingly the preferred architecture for platforms targeting both regulatory compliance and DeFi-native users.

Core Technical Modules of P2P Lending Software

A production-ready P2P lending platform consists of distinct functional modules. Here's what each does and why it matters:Borrower Portal: multi-step loan application flow, document upload, credit bureau integration (Experian, Equifax, TransUnion), income verification via bank data API (Plaid or Finicity), and real-time loan status tracking. The application UX directly determines completion rates — borrower drop-off during application is the single biggest conversion problem on P2P platforms. Every additional screen in the flow reduces completions; every piece of data automatically pulled from bank feeds reduces manual effort.

Lender Dashboard: portfolio view across active loans, expected returns, principal/interest breakdown, auto-invest settings with configurable allocation rules (minimum credit grade, maximum exposure per borrower, geographic filters), notification preferences, and automated tax document generation (Form 1099-INT for interest income).

Loan Origination Engine: rule-based approval workflow, credit scoring integration, interest rate calculation based on risk tier, loan product configuration (term ranges, amount min/max, rate floor/ceiling), and automated offer generation. This is the core logic that determines platform economics — pricing risk accurately is what keeps default rates manageable.

Credit Scoring Module: traditional credit score integration plus alternative credit data (ACD) for thin-filed borrowers. ACD via Plaid or Finicity analyzes a borrower's income patterns and spending behavior directly from bank account data. Platforms using ACD report approving 35% more creditworthy borrowers that traditional FICO models incorrectly reject, while simultaneously reducing defaults by up to 40%.

Escrow Management: lender funds are held in escrow until the loan reaches its funding threshold. On disbursement, funds transfer to the borrower's linked bank account. On repayment, principal and interest distribute pro-rata to each lender who funded the loan. The escrow logic must handle partial funding at deadline, loan cancellation, and partial repayment scenarios without manual intervention.

Secondary Market (Optional): lenders sell their loan notes before maturity, providing liquidity. This is a significant retention feature — lenders who can exit early commit more capital to longer-term loans.

Admin Panel: compliance dashboard, user verification queue, loan approval override controls, fee configuration, fraud monitoring alerts, and regulatory reporting exports.

Every one of these edge cases must be explicitly defined and tested before a single real dollar moves through the system. Platforms that treat failure states as "we'll handle it when it happens" discover them at the worst possible time — when a real user is trying to withdraw real money. We build state transition diagrams for every financial flow before development starts. This documentation also becomes the basis for regulatory audit responses when examiners ask "show us what happens to user funds when X occurs."

How P2P Lending Platform Owners Make Money

The main revenue source for P2P lending platforms is commissions. For P2P lending, platforms typically charge 0.5% to 5% of the loan amount to investors, and 1% to 6% to borrowers as origination fees. Equity-based platforms often retain 6–7% of funds raised and 5–7% of profits. When it comes to tokenizing real estate, management fees of 1–2% annually are standard. Payment processing fees add 2–5% per transaction.A paid subscription system can expand revenue: higher subscription tiers unlock premium analytics, faster application processing, and increased borrowing or investment limits. On Patreon, fees range from 5% to 12% of revenue depending on tier — a comparable tiered model works for both borrower and lender sides of a lending platform.

Separate fees for legal processing of contracts and compliance costs are increasingly common on regulated platforms, either as pass-through costs or as a platform revenue line.

Market Overview: Leading P2P Lending Platforms

By 2026, over 500 crowdfunding and lending platforms operate globally. The primary audience: people under 40 interested in alternative financing who understand modern technologies, plus institutional investors seeking yield in a compressed-rate environment. Market leaders by segment:

LendingClub

The market leader in US P2P lending. LendingClub connects borrowers and lenders with thorough pre-audit to minimize fraud risk. Supported loan types: personal, business, auto refinancing, patient solutions. Commissions: 1–6% to borrowers, 1% service fee on investor income.Investors are attracted to the investment platform because it enables diversified loan portfolios across risk tiers. Borrowers receive a credit rating and competitive interest rate based on solvency analysis. Automatic investment according to predetermined parameters is a standard lender feature.

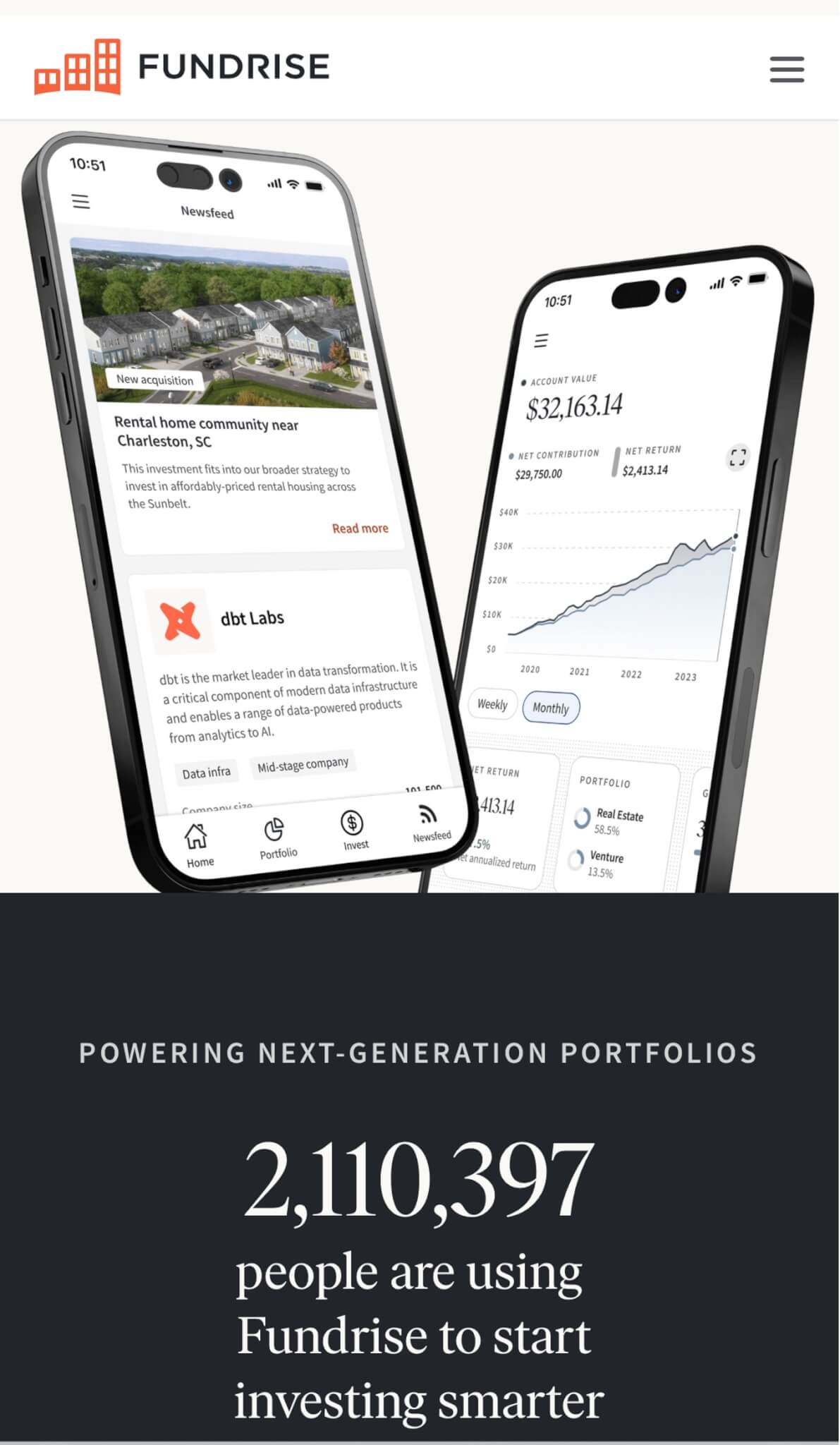

Fundrise

A unique real estate crowdfunding platform that allows US investors to purchase property shares via tokenization. The token approach provides greater transparency and sets a low entry threshold — from $500, since assets can be divided into smaller shares. Portfolio diversification and analytical tools are built in. Revenue model: 1% annual management fee plus asset acquisition fees.

CrowdStreet

A US-based investment crowdfunding platform specialized in commercial real estate for accredited investors — those with $200,000+ annual income or $1M+ in liquid assets. Minimum investment: $20,000. Investors get access to full project materials, risk reports, and financial models, plus direct communication with developers. Commission for developers: 1–3% of financed amount plus performance and service fees.

US Regulatory Framework for P2P Lending Platforms

P2P lending in the US operates under overlapping regulatory frameworks. The path you take determines your compliance architecture and your timeline to launch.SEC and securities registration: most P2P loan notes qualify as securities under SEC definitions. Your platform must either register loan notes as securities offerings or qualify for an exemption. Two primary exemptions:

- Regulation D: private placement to accredited investors only. No maximum raise amount but restricted marketing and investor qualification verification required.

- Regulation CF (Crowdfunding): raises up to $5M/year from non-accredited investors through a FINRA-registered funding portal. Lower capital limit but broader potential investor base.

FINRA registration: platforms operating as funding portals under Regulation CF must register with FINRA as a Funding Portal. Broker-dealer registration applies if you execute securities transactions or provide investment advice. The registration process takes 2–4 months.

CFPB (Consumer Financial Protection Bureau): consumer lending — personal loans, auto refinancing, student loan products — falls under CFPB oversight. Truth in Lending Act (TILA) disclosures: APR, total loan cost, repayment schedule must display at specific borrower journey touchpoints. Non-compliance here generates enforcement actions that are expensive and reputationally damaging.

State licensing: 49 US states require some form of consumer lending license for non-bank lenders. Operating without state licenses exposes you to enforcement. The practical approach: launch in states with lighter requirements first, obtain additional state licenses progressively as volume justifies the compliance investment.

AI Underwriting and Alternative Credit Data

Traditional credit scoring (FICO) excludes approximately 45 million "credit invisible" Americans who have limited credit history despite being financially responsible. For P2P lending platforms, this is both a compliance consideration and a market opportunity.Alternative Credit Data (ACD) addresses this by analyzing non-traditional signals through bank account APIs:

- Cash flow analysis — income patterns and spending behavior from 12 months of bank transaction data (Plaid or Finicity API)

- Income verification — actual payroll deposits rather than self-reported income

- Rent and utility payment history — positive payment signals that FICO ignores

- Employment stability — duration and consistency of income source

Platforms using ACD report approving 35% more creditworthy borrowers that traditional models incorrectly reject, while reducing defaults by up to 40%. Upstart, one of the leading AI-underwriting platforms, has reported 75% fewer defaults compared to traditional FICO scoring on comparable loan pools.

Every credit model must be documented and tested for fair lending compliance — CFPB requires you to be able to explain any adverse action decision in plain language to the applicant. Budget the AI underwriting module as a 3–4 month continuous effort, not a one-time integration. The ML governance requirements alone — model documentation, disparate impact testing, adverse action notice generation — add 3–5 weeks to the initial build.

Development Options: White Label vs Custom

Developing your own P2P lending platform software is a laborious process — providing all necessary functionality, securing payment transactions, and addressing legal requirements simultaneously. Two primary paths:Platform from scratch is the right choice when you have non-standard requirements: proprietary underwriting models, DeFi/blockchain integration, a unique borrower acquisition strategy, or specific regulatory configurations not available in standard templates. More time-consuming and financially intensive.

White Label solution uses a ready-made base that gets further developed: UI/UX design modified, specific functionality added, branding applied. Faster to market, lower initial cost, higher dependency on the vendor's existing architecture.

| Tier | Scope | Timeline | Cost |

|---|---|---|---|

| White Label | Branded platform, standard P2P lending flows, basic customization | 4–8 weeks | $20K–$50K setup + $2K–$8K/month |

| Custom Basic | Borrower portal, lender dashboard, loan origination, KYC/AML, admin panel, basic credit scoring | 10–16 weeks | $40,000–$80,000 |

| Custom Advanced | Basic + AI underwriting (Plaid), escrow automation, secondary market, TILA disclosures, SEC compliance layer | 16–24 weeks | $80,000–$180,000 |

| Custom Enterprise | Full stack: DeFi/blockchain, institutional lender portal, automated collections, CFPB tooling, multi-state licensing support | 5–9 months | $180,000–$400,000 |

Ongoing infrastructure: $2,000–$6,000/month. State lending licenses: $5,000–$30,000 per state in legal fees, separate from development.

Step-by-Step Launch Guide for P2P Lending Platforms

Step 1 — Define platform type and business model. P2P consumer loans, SME lending, real estate investment, or equity crowdfunding each have different regulatory paths and technical requirements. This choice determines your SEC exemption strategy, FINRA registration requirements, and development scope.Step 2 — Determine borrower and lender selection criteria. Reputation is central to crowdfunding and lending platforms. Create a detailed application questionnaire. Determine KYC tier requirements: basic email verification for browsing, ID + selfie for account opening, bank account verification for borrowing or investing above thresholds.

Step 3 — Design the interface with mobile-first in mind. The 2026 UX trend that has proven durable: simplicity and inclusivity. The interface should be intuitive for first-time users while providing depth for experienced investors. Registration, verification, and application flows must be clear at every step. Adaptive design for mobile is not optional — 70%+ of fintech interactions in 2026 happen on mobile.

Step 4 — Implement security infrastructure. For platforms handling financial transactions:

- SSL/TLS protocols for encryption in transit

- 2FA authentication (TOTP + SMS)

- Immutable transaction audit logs (retained per state requirements, typically 2–7 years)

- Rate limiting on all financial endpoints (not just login)

- AML program with SAR filing capability for transactions over $5,000

- System backups with tested recovery procedures

Step 5 — Integrate payment methods. The choice of available payment methods directly affects acquisition and retention. Integrate at minimum: ACH bank transfers (the US standard for lending disbursement and repayment), e-wallets, and optionally crypto wallets for DeFi-adjacent platforms. Top platforms support PayPal, Bank Transfers, ACH, and regional payment rails based on target geography.

Step 6 — Enable platform communication. Maintain technical support (live chat, help documentation, support ticket system) and direct communication channels between investors and project creators or borrowers. Communication quality is a significant trust signal that affects platform reputation.

Frequently Asked Questions

What is P2P lending platform software?

P2P lending platform software is the technology stack that powers a marketplace connecting borrowers directly with individual or institutional lenders — bypassing traditional bank intermediaries. The software manages loan origination, credit scoring, investor matching, escrow, repayment collection, and regulatory compliance. Unlike a banking app that holds deposits, a P2P lending platform is a marketplace where the software enforces the rules, risk logic, and transaction flows between two independent parties.

How much does it cost to build P2P lending platform software?

White label solution: $20,000–$50,000 setup plus $2,000–$8,000/month. Custom basic platform (borrower portal, lender dashboard, KYC, basic credit scoring): $40,000–$80,000, 10–16 weeks. Advanced platform with AI underwriting and SEC compliance layer: $80,000–$180,000. Enterprise with DeFi integration and full regulatory tooling: $180,000–$400,000. State lending licenses add $5,000–$30,000 per state separately.

What are the core modules of P2P lending software?

Production-ready P2P lending software includes: Borrower Portal (application flow, document upload, bank data integration via Plaid), Lender Dashboard (portfolio analytics, auto-invest settings, tax document generation), Loan Origination Engine (credit scoring integration, rate calculation, offer generation), Escrow Management (fund collection, pro-rata disbursement, repayment distribution), Admin Panel (compliance dashboard, verification queue, fraud monitoring), and optionally a Secondary Market module for note trading.

Do I need a license to operate a P2P lending platform in the US?

Yes. Most P2P loan notes qualify as securities under SEC definitions, requiring either broker-dealer registration or an exemption — Regulation D for accredited investors, Regulation CF for raises up to $5M/year from unaccredited investors through a FINRA-registered funding portal. Consumer lending additionally requires CFPB compliance and state money transmitter or lending licenses in most states. The regulatory path must be decided before development starts — it determines which compliance modules need to be built into the platform architecture.

What's the difference between centralized and decentralized P2P lending?

Centralized P2P (LendingClub model): the platform manages credit rules, matching, escrow, and compliance. Full regulatory responsibility, but full control over user experience. Decentralized P2P (DeFi model): loans execute via smart contracts — no central authority, collateral-based credit, lower operational cost, but evolving US regulatory status. Hybrid: centralized compliance with blockchain-based transaction transparency. Most US startups start with centralized given current regulatory clarity.

How does AI underwriting work in P2P lending software?

AI underwriting supplements traditional FICO scoring with alternative credit data: bank account cash flow analysis (via Plaid or Finicity API), rent and utility payment history, and employment stability signals. The ML model scores thin-filed borrowers who would be rejected by FICO-only models. The scoring model must be documented and tested for fair lending compliance. Building it correctly requires 3–4 months of continuous development — including ML governance, disparate impact testing, and adverse action notice generation — not a one-time API integration.

How long does it take to build a P2P lending platform?

Basic platform: 10–16 weeks of development. Advanced with AI underwriting and compliance layer: 16–24 weeks. Enterprise: 5–9 months. State lending license applications run in parallel and take 3–12 months depending on state. SEC Regulation CF funding portal registration with FINRA takes 2–4 months. The compliance timeline is often longer than the development timeline — start both processes on day one.

What security features does P2P lending software need?

Minimum: SSL/TLS encryption, 2FA (TOTP + SMS), PCI DSS compliance for payment data, rate limiting on all financial endpoints, immutable audit logs for all loan and payment events (retained 2–7 years per state requirements), and a documented AML program with SAR filing for suspicious transactions over $5,000. Advanced: AI-driven fraud detection for synthetic identity fraud, device fingerprinting, and bank account ownership verification to prevent fraudulent ACH pulls.