The answer most founders want: somewhere between $80,000 and $500,000, depending on your jurisdiction, platform choice, and execution model. The answer most founders get: more than that, because the numbers that show up in guides consistently leave out payment processor reserves, compliance infrastructure, and the real cost of getting from "platform is live" to "we have 200 active trading accounts".

This guide gives you the full breakdown — component by component, with realistic 2026 figures — and the parts that regularly surprise new brokers after contracts are signed.

Cost Summary: What to Expect at Each Budget Level

Before the full breakdown, a quick orientation. The three realistic tiers for launching a forex brokerage in 2026:| Micro Broker | Standard Broker | Premium Broker | |

| License | Offshore (Seychelles/Vanuatu): $5K–$20K | Tier-2 (Mauritius/LFSA): $25K–$50K | Tier-1 (CySEC/FCA): $30K–$80K |

| Platform | MT4/MT5 WL: $10K–$20K setup | MT4/MT5 WL: $10K–$20K setup | Custom: $80K–$300K |

| Regulatory capital | $50K minimum | $100K–$250K | $730K+ |

| Liquidity deposit | $50K | $100K–$150K | $200K+ |

| CRM | SaaS: $500–$2K/month | SaaS: $2K–$5K/month | Custom: $20K–$60K build |

| Payment setup | $3K–$10K | $5K–$15K | $10K–$30K |

| KYC/AML setup | $2K–$5K | $5K–$15K | $15K–$30K |

| Legal/incorporation | $3K–$8K | $5K–$15K | $10K–$30K |

| Total launch budget | $120K–$200K | $250K–$400K | $500K–$1M+ |

| Monthly ongoing | $15K–$25K | $25K–$45K | $50K–$100K+ |

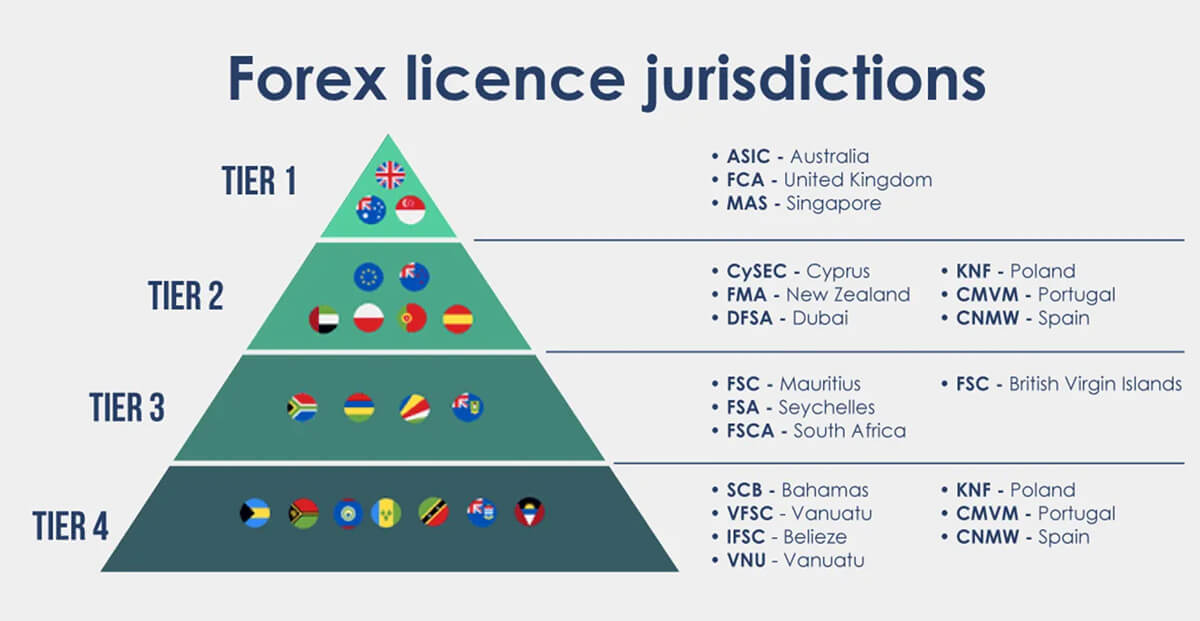

License Cost by Jurisdiction

The state or region jurisdiction determines the type of license without which a brokerage company cannot operate. Licensing is often treated as the biggest cost — but the regulatory capital requirement is almost always larger than the license fee itself.| Jurisdiction | Regulator | Min. Capital | License Fee | Timeline | Banking Access |

| Seychelles | FSA | $50K | $5K–$15K | 1–3 months | Limited |

| Vanuatu | VFSC | $50K | $3K–$10K | 1–2 months | Limited |

| Mauritius | FSC | $250K | $15K–$30K | 2–4 months | Moderate |

| Cyprus (CySEC) | CySEC | €125K–€730K | $25K–$60K | 3–6 months | Good (EU passporting) |

| Australia (ASIC) | ASIC | AUD $1M | $20K–$50K | 3–6 months | Excellent |

| UK (FCA) | FCA | £730K+ | $30K–$80K | 6–12 months | Excellent |

| USA (CFTC/NFA) | CFTC + NFA | $20M+ | $100K+ | 12–24 months | Full |

Banking institutions and payment aggregators prefer to work with licensed brokerage companies. A license obtained in a developed country simplifies opening a corporate bank account and works in other jurisdictions through mutual recognition agreements. Most brokers take a two-phase approach: launch with a Tier-2 or offshore license to validate the business, then upgrade to CySEC or FCA when volume justifies the additional capital requirement.

For the US market specifically: CFTC registration requires $20M+ in net capital, making it practically inaccessible for most startups. Most brokers targeting US-adjacent markets operate under offshore licenses with explicit US geographic exclusions and consult specialized legal counsel before accepting US clients.

Trading Platform Cost: MT4/MT5, cTrader, or Custom

The trading platform is the engine of your brokerage. The choice between white label and custom stock trading app development is the most consequential technology decision — and the one with the most misleading cost comparisons.| MT4/MT5 White Label | cTrader | Custom Platform | |

| Setup cost | $10K–$20K | $15K–$30K | $80K–$300K |

| Monthly fee | $4K–$8K/month | $2K–$5K/month | Infrastructure only |

| Bridge fees (separate) | $1K–$2.5K/month | Included | Custom |

| Trader familiarity | Very high | Medium-High | Low (new brand) |

| Customization | Limited | Medium | Unlimited |

| Hybrid routing | Basic admin panel only | Better API access | Full custom logic |

| Break-even vs WL | Baseline | Similar | ~18–24 months at moderate volume |

Among the proven platforms: MetaTrader 4 and 5 remain the industry standard for retail forex, Quadcode offers a modern SaaS alternative with diverse tools, and cTrader is preferred by algorithmic trader audiences who need professional FIX API access. How much it costs to open a brokerage company depends heavily on this platform selection and whether the monthly licensing fees or a one-time custom build better fits your growth trajectory.

Routing the same trader differently based on behavioral profile — the way a mature hybrid broker actually operates — requires a custom risk management overlay on top of the white-label platform. The practical path: launch on white label to validate the business model with real clients. Use 12–18 months of data to understand where the white-label ceiling limits profitability. Then invest in custom development for the specific components where flexibility is needed.

Liquidity Provider Cost

Liquidity providers supply the market prices and execution for your brokerage. Without reliable liquidity partners, traders experience slow execution, wide spreads, and re-quotes — the fastest path to account closure and negative reviews.Retail Liquidity Providers (accessible for new brokers): typically require a security deposit of $50,000–$100,000. Monthly fees are volume-based: $0.5–$1.5 per million USD traded, with a minimum monthly commitment of $500–$2,000. These providers offer accessible spreads and straightforward onboarding, though spread quality is weaker than institutional tiers.

Prime of Prime (Tier-2): require $100K–$500K security deposits and minimum monthly volumes. Offer better spreads and access to deeper institutional liquidity. The right tier for brokers targeting active traders who compare execution quality.

Direct Prime Broker (Tier-1): Goldman, Deutsche, UBS. Require $1B+ monthly volume — out of reach for startup brokers. Relevant for context when clients ask about your liquidity source; not a realistic option at launch.

Critical note on the deposit: the liquidity provider security deposit is not operational capital. It sits in the LP's account, funds your trading exposure, and is returned when the relationship ends. If your total capital is $150K and you place $80K with the LP, you have $70K for everything else — platform, compliance, staff, and marketing for 12+ months. Most founders discover this distinction too late.

CRM and Back-Office Cost

The platform's technological infrastructure includes a matching system with a transaction engine and liquidity providers accumulating funds in various currencies, CRM, and the trading platform itself. The CRM is the operational core — it handles KYC workflows, IB commission tracking, withdrawal approvals, and compliance reporting.

SaaS CRM options (B2Core, LXCRM, UpTrader): $500–$3,000/month depending on active accounts and feature tier. Integration with MT4/MT5 is native for most providers. The limitation: commission logic for complex IB structures and custom compliance reports often require workarounds or custom development on top.

Custom CRM development: $20,000–$60,000 one-time cost. Justified when your IB commission structure has more than three tiers, your compliance reporting requirements differ from standard templates, or you're scaling to multiple regions with different regulatory requirements.

After launching the platform to increase ARPU and LTV, provide brokers and traders: watch list (instruments), digital asset selector, accelerated trading protocol, hedging services, multi-monitor chart display, simplified access to shorts and longs, leverage explanation with optimal calculation per case, and protection against negative balance. Speed of payment solutions with revenue generation in dozens of ways brings together traders from multiple countries.

Payment Processing and Banking Cost

Reliable payment processing is essential for deposits and withdrawals. Multiple payment options — bank transfers, credit cards, crypto — make your brokerage more attractive, but each integration carries setup and ongoing costs.PSP setup costs: $3,000–$30,000 depending on the number of providers and regional payment methods. Standard integrations (bank wire, SEPA, card processing) are at the lower end; crypto wallet integration and local payment rails (mobile money, local bank networks) add cost.

Transaction fees: 0.5–2% of deposit/withdrawal volume for card processing; 0.1–0.5% for bank wire; 0.5–1.5% for crypto processors. Offering SEPA, SWIFT, or Faster Payments, stablecoins with USDT, and BTC/ETH/XRP for account currency exchange stimulates growth in volatility resilience.

Banking integration: standard corporate bank account for a Seychelles/Vanuatu broker costs $2,000–$10,000 to establish through a banking correspondent. Tier-1 licensed brokers access mainstream banking directly. Connect multi-currency accounts for portfolio diversification and to reduce currency conversion friction.

KYC/AML Compliance Cost

Compliance is not a feature you add at launch — it's infrastructure that shapes your architecture from the first sprint. KYC/AML requirements apply regardless of jurisdiction.KYC provider setup (SumSub, Jumio, Persona): $2,000–$10,000 initial integration. Per-verification costs: $0.50–$2.00 depending on verification tier (ID upload vs. video verification vs. database checks).

AML monitoring: $500–$2,000/month for transaction monitoring software. Includes sanctions screening, PEP (politically exposed persons) checking, and suspicious activity flagging.

Compliance officer: required by most regulators as a named individual. $60,000–$120,000/year salary depending on region. Cannot be outsourced for most Tier-1 and Tier-2 licenses.

Roadmap and Break-Even Point

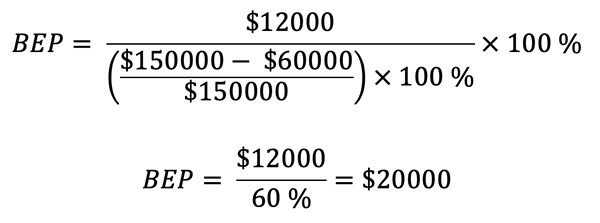

Roadmap and a business plan are two components of the project. The business plan is intended to attract investors and brokers, including volatility forecasts, license and labor costs, purchase or lease of servers and cloud solutions, spreads and commissions. Calculation of the break-even point (BEP):

Suppose 30,000 operations are performed per month, the cost of servicing each one is $2 on average ($60,000 current expenses), generating a profit of $5. Gross income is $150,000. $12,000 is spent on fixed costs (labor, platform, White Label, servers). Then:

Profit margin on marginal profit = (($5 — $2) / $5) × 100% = 60%

BEP (gross profit to break-even) = $12,000 / 60% × 100% = $20,000

BEP (number of services) = $60,000 / $5 = 12,000

To reach the break-even point of a Forex trading company, 12,000 operations must be carried out. Each subsequent one brings $3 direct profit. Profitability in this example is 52%:

This is the mathematics. Here's the operational reality:

IB networks take 3–6 months to produce steady referral flow. The brokerages that reach break-even fastest share one operational characteristic: they launch with two or three IBs already committed before the platform goes live — not after. Each committed IB represents predictable minimum volume. Building the platform with IB management tools, commission tracking, and partner dashboards as first-class features — not afterthoughts — is the technical decision that enables this strategy.

Partnerships and Revenue Diversification

Partnerships are a primary acquisition channel. Compensation models include referral fees, percentage of profit generation, and conversion-based commission — provided they keep brokers sustainable. Company visibility through contextual PPC advertising, SEO, mailings, influencer engagement, social media, and messaging apps like Telegram, LinkedIn, or Twitter builds the funnel.Forex brokers profit from commissions, swaps, and spreads as counterparties, and from VPS services. White Label solutions are 3–5x cheaper than native development, with launch times of 2–4 weeks and a debugged CRM included. Rent with a cost of $4,000–$8,000/month is significantly different from native development for $80,000–$300,000 with an additional CRM development cost of $20,000–$60,000.

Pay attention to affluent Muslim traders who require Shariah-compliant Islamic trading accounts — this segment represents significant AUM in Gulf markets and requires specific swap-free account configuration.

Hidden Costs Nobody Tells You About

The numbers above are the visible costs. The costs that consistently surprise new brokers arrive after contracts are signed and timelines are locked.Payment processor reserve requirements. When you onboard a PSP for deposits and withdrawals, they run their own compliance review and typically require a cash reserve — 5–15% of monthly processing volume held as a chargeback buffer. On a platform processing $500,000/month in deposits, that's $25,000–$75,000 tied up in an account that generates no yield. This is entirely separate from your regulatory capital requirement and rarely appears in brokerage cost guides.

Platform add-on fees that aren't in the headline price. MT4/MT5 monthly fees ($4,000–$8,000) typically exclude: bridge fees for liquidity routing ($1,000–$2,500/month), risk management plugin fees ($500–$1,500/month each), and server hosting infrastructure ($1,000–$5,000/month for colocation in financial data centers like Equinix LD4 or NY4). A platform quoted at "$5,000/month" can realistically cost $9,000–$12,000/month once these components are added.

Compliance retrofitting cost. Building KYC/AML correctly means tiered verification with automated risk scoring, AML monitoring on every transaction, and SAR filing capability — not a document upload form. When built in from the start, this adds 15–20% to platform scope. When retrofitted onto a live platform six months after launch, it costs 3–4x more and requires coordinating updates across live user accounts, active transactions, and production database schemas.

Regulators and banking partners increasingly require audit trails for every KYC decision, automated transaction monitoring with documented thresholds, and the ability to produce SAR-format reports on demand. Building this infrastructure correctly from sprint one is significantly cheaper than building it under pressure from a regulatory deadline.

Full Cost Comparison: White Label vs Custom Build

| Component | White Label Path | Custom Platform |

| Platform setup | $10K–$20K (MT4/MT5) | $80K–$300K |

| Platform monthly | $4K–$8K + $1K–$2.5K bridge | Infrastructure only ($2K–$8K) |

| CRM | $500–$3K/month SaaS | $20K–$60K custom build |

| License (offshore) | $5K–$20K | $5K–$20K |

| License (Tier-1) | $25K–$80K | $25K–$80K |

| Regulatory capital | $50K–$730K+ | $50K–$730K+ |

| Liquidity deposit | $50K–$200K | $50K–$200K |

| KYC/AML setup | $2K–$10K | $5K–$20K |

| PSP setup | $3K–$15K | $3K–$15K |

| PSP reserve | 5–15% monthly volume | 5–15% monthly volume |

| Legal/incorporation | $3K–$15K | $3K–$15K |

| Total launch (offshore) | $120K–$300K | $200K–$600K |

| Monthly ongoing | $15K–$35K | $10K–$25K (no platform fee) |

| Custom break-even vs WL | Baseline | ~18–24 months at moderate volume |

Understanding the concepts and techniques to build and launch a Forex broker website, planning a roadmap and a business plan with break-even points, and thoughtful licensing is the foundation for a successful brokerage. Smart platform selection, IB infrastructure, and compliance architecture built in from the start — not retrofitted — are what separate brokerages that reach profitability from those that run out of capital before they get there.

Frequently Asked Questions

How much does it cost to start a forex brokerage in 2026?

Total launch budget ranges from $120,000–$200,000 for a minimal offshore white-label brokerage to $500,000–$1M+ for a Tier-1 licensed custom platform. The most important nuance: regulatory capital ($50K–$730K+) and liquidity provider security deposit ($50K–$200K) represent 50–70% of total capital required — both are ring-fenced and can't fund operations. Budget for platform, compliance, staff, and 12 months of operations separately.

What's the cheapest way to start a forex brokerage?

Vanuatu or Seychelles license ($50K capital, $3K–$15K fee, 1–3 months) + MT4/MT5 white label ($10K–$20K setup, $4K–$8K/month) + basic SaaS CRM ($500–$1K/month) + retail LP ($50K deposit). Total: $120K–$150K. The tradeoff: limited banking access, restricted institutional LP relationships, and a jurisdictional credibility ceiling that caps your potential client base.

What are the ongoing monthly costs of a forex brokerage?

A mid-tier white-label brokerage spends $25,000–$45,000/month: platform and bridge fees ($5K–$10K), CRM and compliance tools ($2K–$5K), liquidity fees (volume-based), payment processing (0.5–2% of volume), KYC verifications ($0.50–$2 each), hosting ($1K–$5K), and staffing — compliance officer, risk manager, and customer support add $15K–$25K/month in salary costs.

Is MT4/MT5 white label cheaper than a custom platform?

At launch: significantly yes. MT4/MT5 setup costs $10,000–$20,000 vs $80,000–$300,000 for custom. The monthly comparison is less clear: white label costs $4,000–$8,000/month in platform fees (plus $1,000–$2,500 bridge fees) while a custom platform costs infrastructure only. A custom platform becomes financially competitive at roughly 18–24 months of moderate volume. The more important consideration: white label caps your hybrid execution routing flexibility, which limits profit optimization at scale.

What is the forex broker license cost by country?

License fee ranges: Vanuatu VFSC $3K–$10K, Seychelles FSA $5K–$15K, Mauritius FSC $15K–$30K, CySEC $25K–$60K, ASIC $20K–$50K, FCA $30K–$80K, US CFTC $100K+. But the license fee is rarely the biggest cost — regulatory capital is. Seychelles requires $50K paid-up capital; CySEC requires €125K–€730K; FCA requires £730K+. US CFTC requires $20M+ net capital, making US retail forex brokerage impractical for most startups.

What hidden costs do new forex brokers miss?

Three consistently: (1) PSP reserves — payment processors hold 5–15% of monthly processing volume as chargeback buffer, tying up $25K–$75K at $500K/month volume. (2) Platform add-on fees — MT4/MT5 quotes exclude bridge fees ($1K–$2.5K/month), risk management plugins ($500–$1.5K/month each), and hosting. (3) Compliance retrofitting — building KYC/AML post-launch onto a live platform costs 3–4x what building it correctly from the start would have cost.

How long does it take to break even as a new forex broker?

Realistically 8–18 months, not 3–6 months as business plans typically project. Key variables: trader acquisition speed (Google/Meta have country-specific forex CFD ad restrictions), IB network development (takes 3–6 months to produce steady referral flow), and monthly trading volume per active account. Brokers that reach break-even fastest launch with 2–3 IBs already committed before going live — not after.

What's the difference between liquidity deposit and regulatory capital?

Both are required, both are large, and neither funds operations. Regulatory capital ($50K–$730K+) sits in a segregated account required by your license regulator — it proves financial substance and cannot be used for day-to-day expenses. Liquidity provider deposit ($50K–$200K) sits with your LP as a security margin for trading exposure — it's returned when the relationship ends. Together they can represent 70%+ of total capital raised. Founders who don't model these separately from operational capital often discover the distinction in month two when the operating account runs dry.