Starting a forex brokerage is one of the more complex financial businesses to launch — not because the market is inaccessible, but because the decisions compound quickly. Your business model determines your technology stack. Your jurisdiction determines your minimum capital. Your platform choice determines your customization ceiling two years from now. Getting these three decisions right in the right order is what separates brokerages that reach profitability from those that run out of capital before they get there.

The foreign exchange market processes over $7.5 trillion in daily volume. Retail participation is growing across Southeast Asia, Latin America, and Africa — markets where local banks offer minimal investment options and forex access fills a real gap. Whether you aim to start a forex trading company from scratch or launch on a white-label platform, this step-by-step guide covers what actually matters.

Step 1 — Choose Your Business Model: A-Book, B-Book, or Hybrid

The single most consequential decision in launching a forex brokerage isn't technology or jurisdiction — it's your execution model. This determines your revenue source, risk profile, regulatory exposure, and relationship with traders.A-Book (NDD — No Dealing Desk)

Your platform routes all client orders directly to external liquidity providers. You earn from the spread markup or commission on each trade — regardless of whether the trader wins or loses. This model is conflict-free, more straightforward to regulate, and scales better long-term. The constraint: margin per trade is lower and you depend on trading volume.B-Book (DD — Dealing Desk)

Client orders are filled internally — your platform acts as the counterparty. When a client loses, the brokerage profits. This generates higher margins per trade and requires less external liquidity infrastructure. The risks: regulatory scrutiny (B-book brokers are frequently investigated for order manipulation), reputational exposure, and concentration risk if a sophisticated client wins consistently.Hybrid — The Practical Default

Most serious brokerages operate hybrid models: routing large or sophisticated traders A-book while maintaining a B-book for smaller accounts that statistically generate losses. This balances risk exposure with profitability.| A-Book (NDD) | B-Book (DD) | Hybrid | |

|---|---|---|---|

| Revenue source | Spread + commission | Client losses | Both, segmented by trader |

| Conflict of interest | None | High | Managed |

| Regulatory risk | Low | Higher scrutiny | Medium |

| Liquidity required | External LP mandatory | Internal only | Both |

| Technology complexity | Medium | Low | High |

| Best for | Regulated markets, institutional | Small retail, fast launch | Scalable retail brokerage |

Brokers who start with a white-label solution often discover this limitation when they try to implement hybrid routing and find the white-label doesn't support the configuration granularity they need. This is the decision that should be made before selecting a platform, not after.

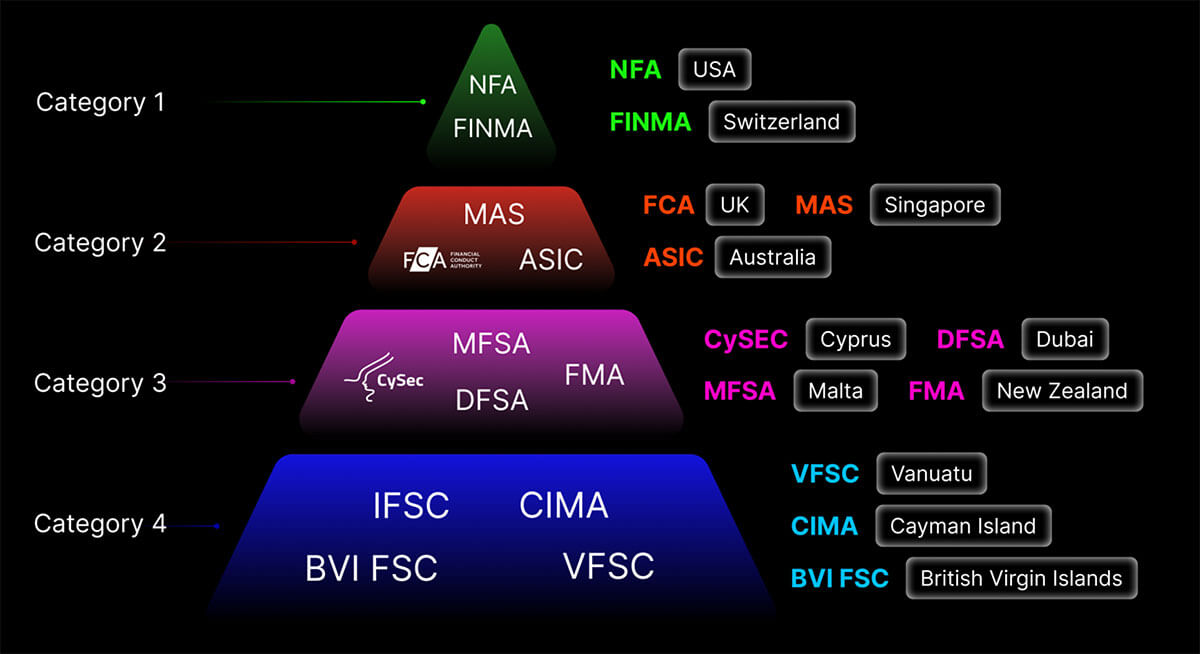

Step 2 — Choose Your Jurisdiction and Get Licensed

Jurisdiction selection determines regulatory obligations, minimum capital, client trust levels, and ongoing compliance costs. There is no universally "best" jurisdiction — only the right one for your specific market, capitalization, and growth strategy.| Jurisdiction | Regulator | Min. Capital | License Cost | Timeline | Trust Level |

|---|---|---|---|---|---|

| Cyprus (CySEC) | CySEC | €125K–€730K | $25K–$60K | 3–6 months | High (EU passporting) |

| UK (FCA) | FCA | £730K+ | $30K–$80K | 6–12 months | Very High |

| Australia (ASIC) | ASIC | AUD 1M | $20K–$50K | 3–6 months | High |

| Seychelles (FSA) | FSA | $50K | $5K–$15K | 1–3 months | Medium |

| Vanuatu (VFSC) | VFSC | $50K | $3K–$10K | 1–2 months | Low–Medium |

| Mauritius (FSC) | FSC | $250K | $15K–$30K | 2–4 months | Medium |

| Dubai (DFSA/ADGM) | DFSA | $500K+ | $30K–$70K | 3–6 months | High |

| USA (CFTC/NFA) | CFTC + NFA | $20M+ | $100K+ | 12–24 months | Very High |

In the USA, retail forex dealers are licensed and controlled by the CFTC and NFA. The $20M+ net capital requirement makes full CFTC registration effectively inaccessible for startups. Most brokers targeting US retail traders use offshore licenses combined with US exclusion policies, or pursue NFA registration only as an introducing broker.

Step 3 — Write a Business Plan for Your Forex Company

A business plan for a forex brokerage is not a generic startup document — it needs to address the financial services-specific variables that determine viability.The core calculation: if you attract 1,000 traders with average deposits of $1,000, your gross platform exposure is $1M. At a 7–20% income from attracted capital and a 30–40% share of trader profits, the math looks like this:

| Metric | Conservative | Optimistic |

|---|---|---|

| Traders | 1,000 | 1,000 |

| Average deposit | $1,000 | $1,000 |

| Platform income from capital (7%) | $70,000 | — |

| Platform income from capital (20%) | — | $200,000 |

| Share of trader profits (30–40%) | $60,000 | $280,000 |

| Gross revenue estimate | $130,000 | $480,000 |

| Operating costs (~25–45%) | $32,500 | $216,000 |

| Net profit estimate | ~$97,500 | ~$264,000 |

Key plan sections to develop: starting capital for launch, initial support infrastructure for traders, anticipated costs (technology, staff, compliance, marketing) and revenues, jurisdiction-specific regulatory costs, and competitive analysis of brokers operating in your target market.

Step 4 — Choose Your Platform: White Label, SaaS, or Custom

Technology is where the broker's product lives. The platform choice determines what features you can offer, how fast you can launch, and what you can build later.| MT4/MT5 White Label | SaaS Forex Solution | Custom Platform | |

|---|---|---|---|

| Time to launch | 4–8 weeks | 1–3 weeks | 4–8 months |

| Setup cost | $10K–$30K + $3K–$5K/month | $2K–$10K/month | $80K–$300K |

| Customization | Limited — MetaQuotes controls roadmap | Limited to provider's features | Unlimited |

| Trader familiarity | Very high — industry standard | Variable | Depends on UX investment |

| Ownership | Rented license | Rented | Full |

| Best for | Fast launch, established retail audience | MVP testing | Unique product, long-term independence |

MT4/MT5 White Label remains the default for over 80% of new brokers. MetaTrader's installed base is enormous — many traders won't use an unfamiliar platform. For a new broker without an established brand, launching on MT4/MT5 means inheriting institutional trust from the platform name.

You can also connect a stock trading app development company and develop your project from scratch. This takes 4–6 months and a budget of $80,000–$300,000 depending on scope.

Step 5 — Set Up Liquidity

Liquidity is what makes your brokerage functional. Without proper liquidity connections, traders can't execute at competitive prices and your A-book model can't operate.Tier-1 Prime Brokers (Goldman, Deutsche, UBS): direct access, tightest spreads, minimum volume requirements of $1B+ monthly. Not accessible for startups.

Tier-2 Prime of Prime (IS Prime, Advanced Markets, Sucden): aggregated Tier-1 liquidity through an intermediary. Typical minimums: $100K–$500K monthly volume, $50K–$100K security deposit. The realistic entry point for growth-stage brokers.

Retail Liquidity Providers (FXCM Pro, Finalto, Amana): accessible for startup brokers. Higher spreads than Tier-1/2, but lower minimums and simpler integration via standard MT4/MT5 bridges.

Forex liquidity integration has the same challenge: if an LP connection drops during order routing, the broker's platform must resolve the order state before confirming the trade to the user. This "order state recovery" logic is where many custom-built forex platforms have production bugs that only surface under real trading conditions. Standard MT4/MT5 bridges handle this for you; custom platforms must implement it explicitly.

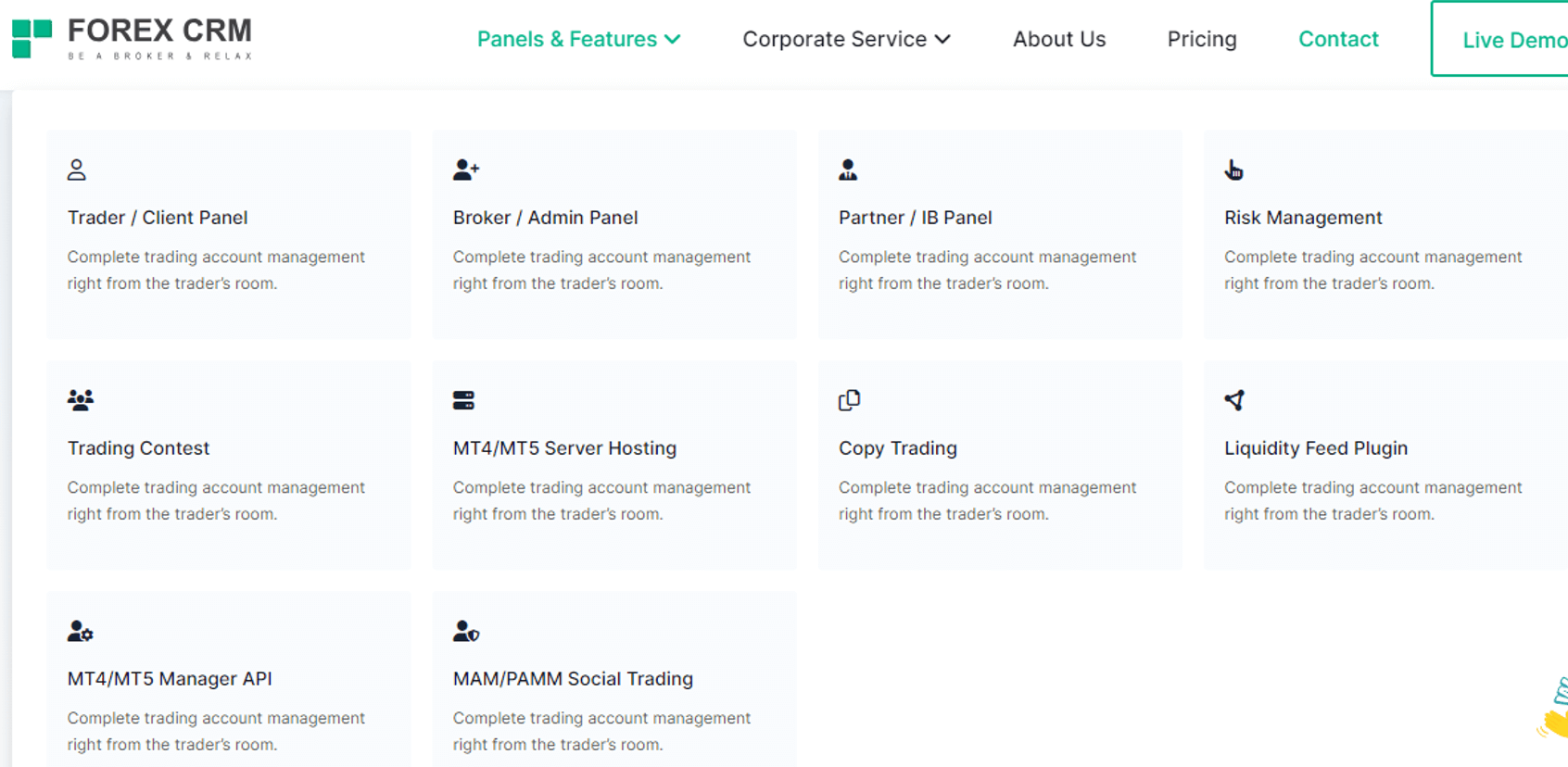

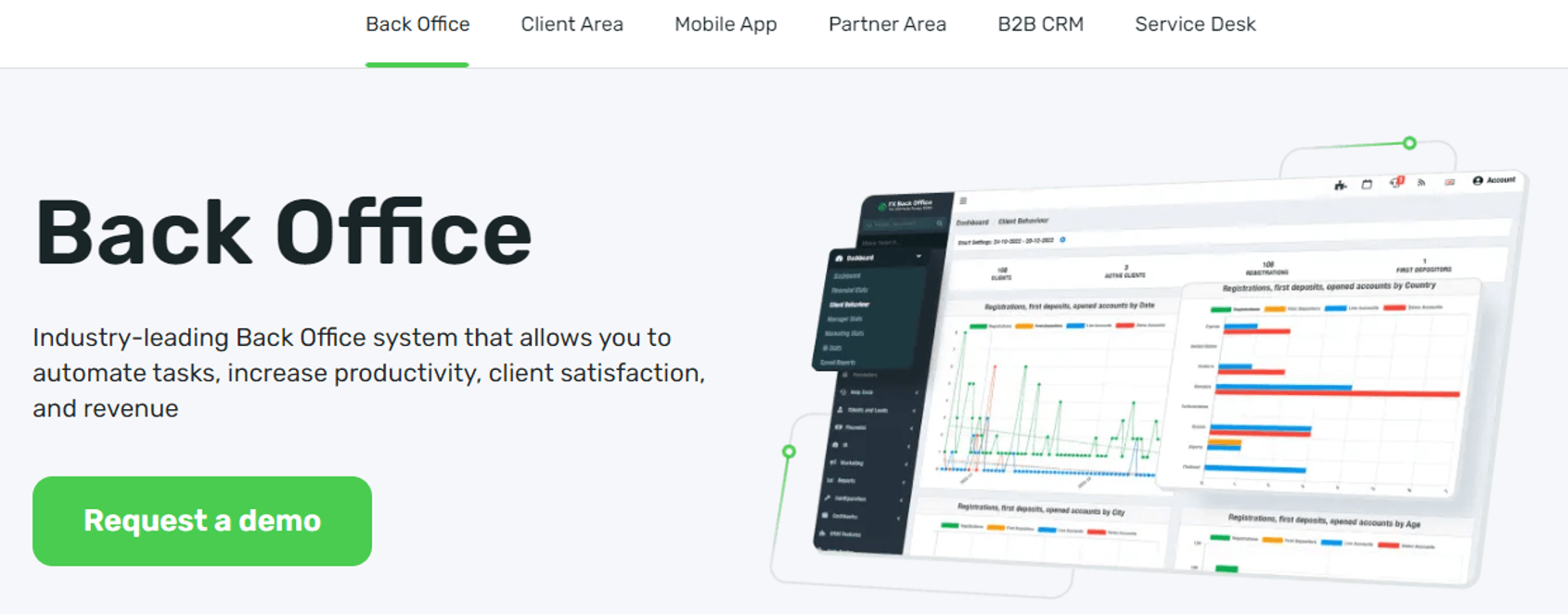

Step 6 — Build Your CRM and Back Office

A CRM system for a forex brokerage isn't a generic sales tool — it's the operational core. Back office and trader room modules handle reconciliation and protection of client accounts, deposit and withdrawal processing, compliance workflows, and communication infrastructure.

What a forex-specific CRM must handle:

- KYC verification workflow — document upload, identity check, risk categorization, approval/rejection with audit trail

- Trader account management — balance, trading history, KYC status, login activity, one-click controls

- Deposit and withdrawal processing — multi-PSP integration, conversion rates, payment status tracking, export in web/Excel/CSV

- IB (Introducing Broker) tracking — multi-tier commission calculation, referral attribution, partner dashboard

- Compliance reporting — SAR preparation tools, regulatory report generation, AML monitoring

- PAMM account management — fund manager allocation, investor tracking, performance fee calculation

Leading platforms in 2026: B2Core (supports crypto and fiat, strong compliance module), LXCRM (serves 350+ brokerages, $200B monthly transactions), UpTrader (strong IB management, MT4/MT5 native integration). Custom CRM development makes sense for brokers with unique IB tier structures or compliance requirements not covered by off-the-shelf options — typically $20,000–$60,000 for a purpose-built solution.

Thoughtful UI/UX in cross-platform format — with both light and dark themes — simplifies operations for both brokers and traders. Fast updates, multi-level information display, and multi-currency support are standard requirements. The forex trading website and CRM must function as a unified system, not separate tools.

Step 7 — Launch Operations: Payments, KYC, and Compliance

Deposit infrastructure is the heartbeat of a forex brokerage. A trader's sensitivity to payment processing directly affects retention — slow confirmations, failed withdrawals, or unclear transaction status are the top reasons traders abandon platforms.Key operational requirements:

- Multi-PSP integration — minimum two payment service providers for redundancy; EMI and PSP licenses increase payment option breadth

- KYC tiers — Level 1 (email only, limited deposits), Level 2 (ID + selfie, standard limits), Level 3 (proof of address, high-value accounts)

- AML monitoring — transaction screening against sanctions lists, automated SAR flagging for suspicious patterns

- Security infrastructure — 2FA (Google Authenticator + SMS), IP whitelisting, country restrictions, SSL/SMTP verification, ELK stack for log monitoring and anomaly detection

- Bulk operations capability — admin tools for mass actions: deposit crediting, class changes, account status updates — essential for operational efficiency at scale

Export of full transaction history in web, Excel, and CSV formats — with high-accuracy exchange rates and prioritized conversion calculations — builds the transparency that serious traders require. REST API integration with external platforms, customizable registration flows, and IB ranking lists with demographic analytics complete the operational layer.

Step 8 — Attract and Retain Traders

Building a forex brokerage firm is the first step; growing the trader base is the ongoing work. Two initial "anchors" that attract traders in any market condition: fast order execution and low commissions. These create the minimum viable reason to choose your platform over an established competitor.Beyond the basics, retention tactics that work at the brokerage level:

Mentoring and education. A broker that teaches traders how to work with commodities, ETFs, futures, and CFD contracts builds long-term loyalty — educated traders trade more and lose less catastrophically, which stabilizes your volume base.

PAMM accounts. Proxy trading via managed PAMM accounts captures traders who want market exposure without active trading. The broker earns from the fund manager's trading activity; the investor earns from the fund manager's performance.

Competitive spreads and transparency. Keeping spreads current with market conditions and clearly communicating the commission structure reduces the friction of "is this broker cheating me?" — a concern that drives churn on retail platforms.

IB program. Introducing brokers who bring clients in exchange for revenue share are the primary acquisition channel for most retail forex businesses. A quality IB dashboard with FTD tracking, CTR analytics, and real-time commission reporting attracts professional affiliates over competitors with basic referral links.

How Much Does It Cost to Start a Forex Trading Company?

| Component | White Label Path | Custom Platform Path |

|---|---|---|

| License (offshore: Seychelles/Vanuatu) | $5K–$20K | $5K–$20K |

| License (CySEC/ASIC) | $25K–$60K | $25K–$60K |

| Legal and company setup | $5K–$15K | $5K–$15K |

| MT4/MT5 white label setup | $10K–$30K | — |

| Custom platform development | — | $80K–$300K |

| CRM and back office | $5K–$20K | $20K–$60K |

| Liquidity deposit (LP security) | $50K–$200K | $50K–$200K |

| Payment gateway setup | $3K–$10K | $3K–$10K |

| KYC/AML integration | $2K–$5K | $2K–$5K |

| Regulatory minimum capital | $50K–$730K | $50K–$730K |

| Total launch budget (offshore WL) | $130K–$300K | $210K–$600K |

| Monthly ongoing costs | $10K–$30K | $15K–$50K |

Brokers who launch with less than $130,000 total — platform, license, liquidity deposit, and six months of operating expenses — typically exhaust capital before reaching break-even trading volume. The regulatory minimum capital is separate from operational capital: it sits in a segregated account and cannot be used for day-to-day expenses.

Frequently Asked Questions

How much does it cost to start a forex trading company?

A realistic minimum for an offshore-licensed forex brokerage (Seychelles or Vanuatu) with MT4/MT5 white label and a basic CRM: $130,000–$200,000 including liquidity deposit and 6 months operating reserve. A CySEC or FCA-licensed broker with custom platform development: $500,000–$1,500,000. The most common failure point is undercapitalization — brokers who launch with "just enough" to get the license rarely survive to profitability.

What is the difference between A-book and B-book forex brokers?

A-book brokers route all client orders to external liquidity providers — they earn from spread or commission regardless of trade outcome. B-book brokers fill orders internally, acting as the counterparty — they profit when clients lose. Most modern brokerages use a hybrid model: routing large or sophisticated traders A-book while maintaining B-book for smaller accounts. Hybrid requires more sophisticated order routing infrastructure but optimizes both risk management and profitability.

What license do I need to start a forex trading company?

It depends on your target market and budget. For rapid, low-cost entry: Seychelles FSA or Vanuatu VFSC ($50K minimum capital, $5K–$20K license cost, 1–3 months). For EU market access: CySEC (€125,000+ capital, 3–6 months). For UK institutional clients: FCA (£730,000+ capital, 6–12 months). For the US retail market: CFTC registration requires $20M+ net capital — effectively inaccessible for startups.

Can I start a forex brokerage with MT4/MT5 white label?

Yes, and it's how the majority of new brokers launch. An MT4/MT5 white label costs $10,000–$30,000 setup plus $3,000–$5,000/month. Traders recognize the platform, which reduces onboarding friction. The limitation: MetaQuotes controls the roadmap, customization is constrained, and you depend on their infrastructure. If you plan to differentiate on platform features or need hybrid order routing, budget for custom development from the start rather than migrating mid-operation.

How long does it take to launch a forex brokerage?

Offshore license (Seychelles/Vanuatu): 1–3 months. CySEC: 3–6 months. FCA: 6–12 months. MT4/MT5 setup: 4–8 weeks from license approval. CRM configuration: 2–4 weeks. Liquidity provider onboarding: 2–6 weeks (LP runs their own compliance review). Realistic total from decision to first client: 3–6 months for an offshore-licensed white-label brokerage.

What CRM does a forex brokerage need?

A forex-specific CRM handles: KYC verification workflow, trader account management, deposit/withdrawal processing, IB tracking and commission calculation, compliance reporting, and marketing automation. Leading options include B2Core, LXCRM, and UpTrader. Custom CRM development ($20,000–$60,000) makes sense for brokers with unique IB tier structures or compliance requirements not covered by off-the-shelf solutions.

What's the best jurisdiction to start a forex company in 2026?

For most new brokers: start with Seychelles FSA or Vanuatu VFSC for speed and low cost, then add CySEC within 12–24 months as volume justifies the capital requirement. Seychelles gives a credible regulated license at $50K minimum capital; CySEC gives EU passporting and institutional counterparty relationships. If your target market is Europe from day one and you have the capital, start with CySEC and avoid the intermediate step.

Do I need a PAMM account feature for my brokerage?

Not mandatory at launch, but it opens a meaningful market segment: traders who want forex market exposure without active trading. PAMM accounts let fund managers trade on behalf of investors, with performance fees split configurable in the CRM. For brokers targeting retail clients in markets where self-trading is intimidating (common in emerging markets), PAMM access increases depositing rates among less experienced users significantly.