Paxful Clone Script: P2P Exchange with Escrow (2026)

Build a P2P Crypto Exchange Fast

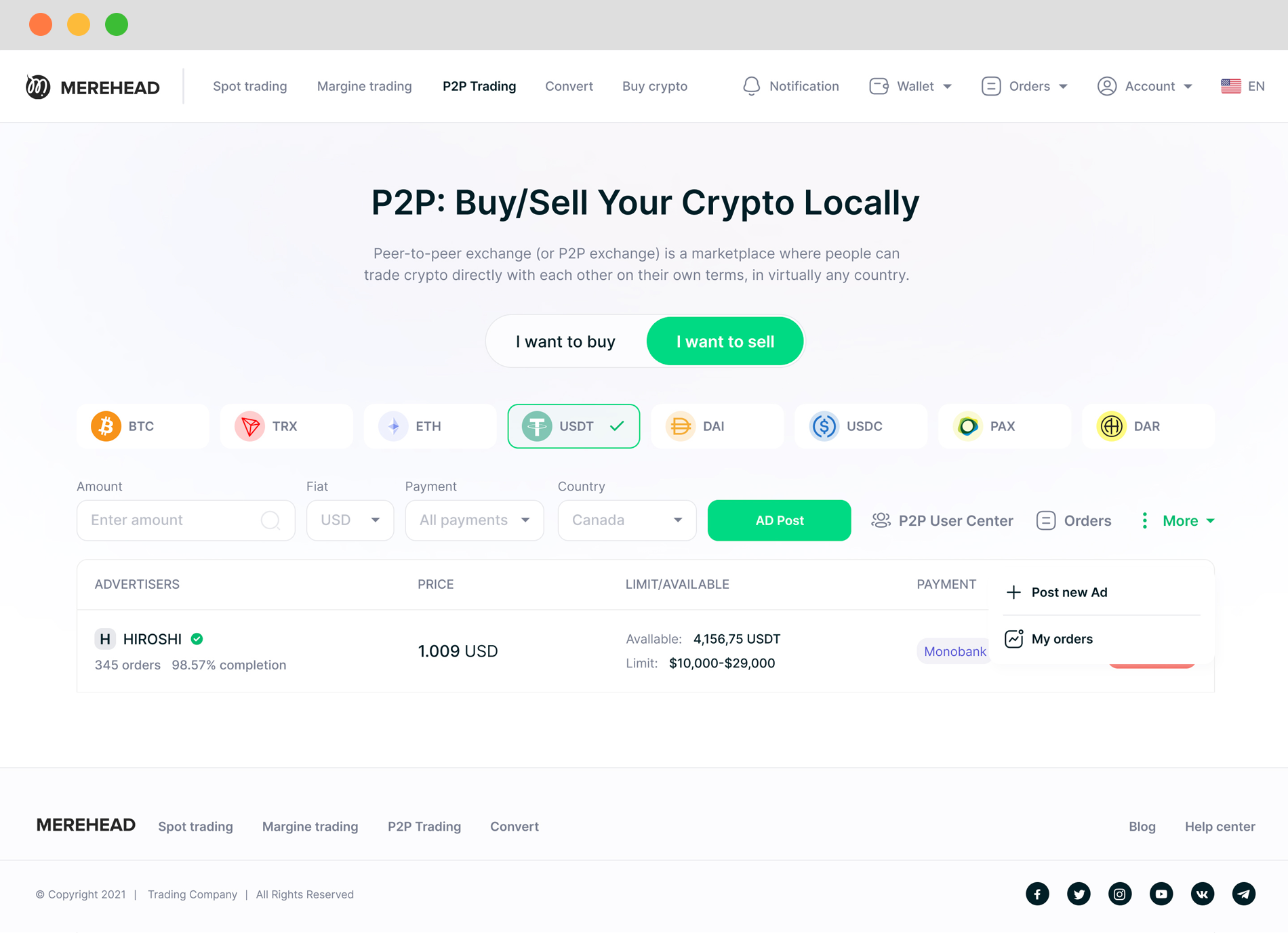

Launch a P2P crypto exchange like Paxful: escrow engine, 300+ payment methods, KYC/AML, dispute resolution, reputation system.

Access to Demo

Paxful was one of the most recognized peer-to-peer (P2P) cryptocurrency exchanges in the world — connecting buyers and sellers directly, offering more than 300 payment methods, with every transaction protected by escrow. Then in April 2023, Paxful suspended operations. LocalBitcoins closed the same year. Two dominant P2P platforms gone within months.

For anyone building a P2P exchange, this matters more than it might seem. The P2P trading model didn't die with Paxful. The users did. Millions of traders in sub-Saharan Africa, Southeast Asia, and Latin America who relied on these platforms to access crypto with local payment methods suddenly had no reliable alternative. Regional P2P platforms that launched in 2023–2024 to fill this gap saw immediate user acquisition with minimal marketing — the demand was already there.

If you're planning to build a P2P crypto exchange like Paxful, this guide walks you through the full process — platform logic, escrow architecture, fraud prevention, monetization, compliance, and development paths.

Here's the full trade flow:

This system supports more than just Bitcoin or Ethereum. With the right configuration, you can enable swaps across any tokens, fiat currencies, and even gift cards. Some P2P exchange scripts also support atomic swaps for crypto-to-crypto exchanges without custodial middlemen.

| P2P Exchange (Paxful model) | Centralized Exchange (Binance model) | |

|---|---|---|

| Liquidity | User-generated — no cold start problem | Requires market makers from day one |

| Payment methods | 300+ (gift cards, mobile money, bank transfer) | Primarily crypto + select fiat on-ramps |

| Best markets | Developing economies, unbanked users, fiat access | Global, professional and volume traders |

| Revenue model | Escrow fees + listing fees + affiliates | Trading fees + spread + margin |

| Development cost | $25K–$80K | $40K–$200K |

| Time to launch | 6–10 weeks | 8–14 weeks |

| Fraud risk | Higher (gift cards, chargebacks) | Lower (crypto-only flows) |

| Competitive moat | Network effect of user reputation scores | Liquidity depth and trading pairs |

| Module | What's Included | Priority |

|---|---|---|

| P2P Trade Engine | Offer posting (buy/sell ads); automatic matching; trade initiation flow; status tracking per trade | Core |

| Escrow System | 5-state trade machine (Initiated → Paid → Confirmed → Released / Disputed); timelock auto-dispute; audit trail | Core |

| Payment Methods | Bank transfer, mobile money, PayPal, gift cards, cash, e-wallets — 50–300+ configurable per region | Core |

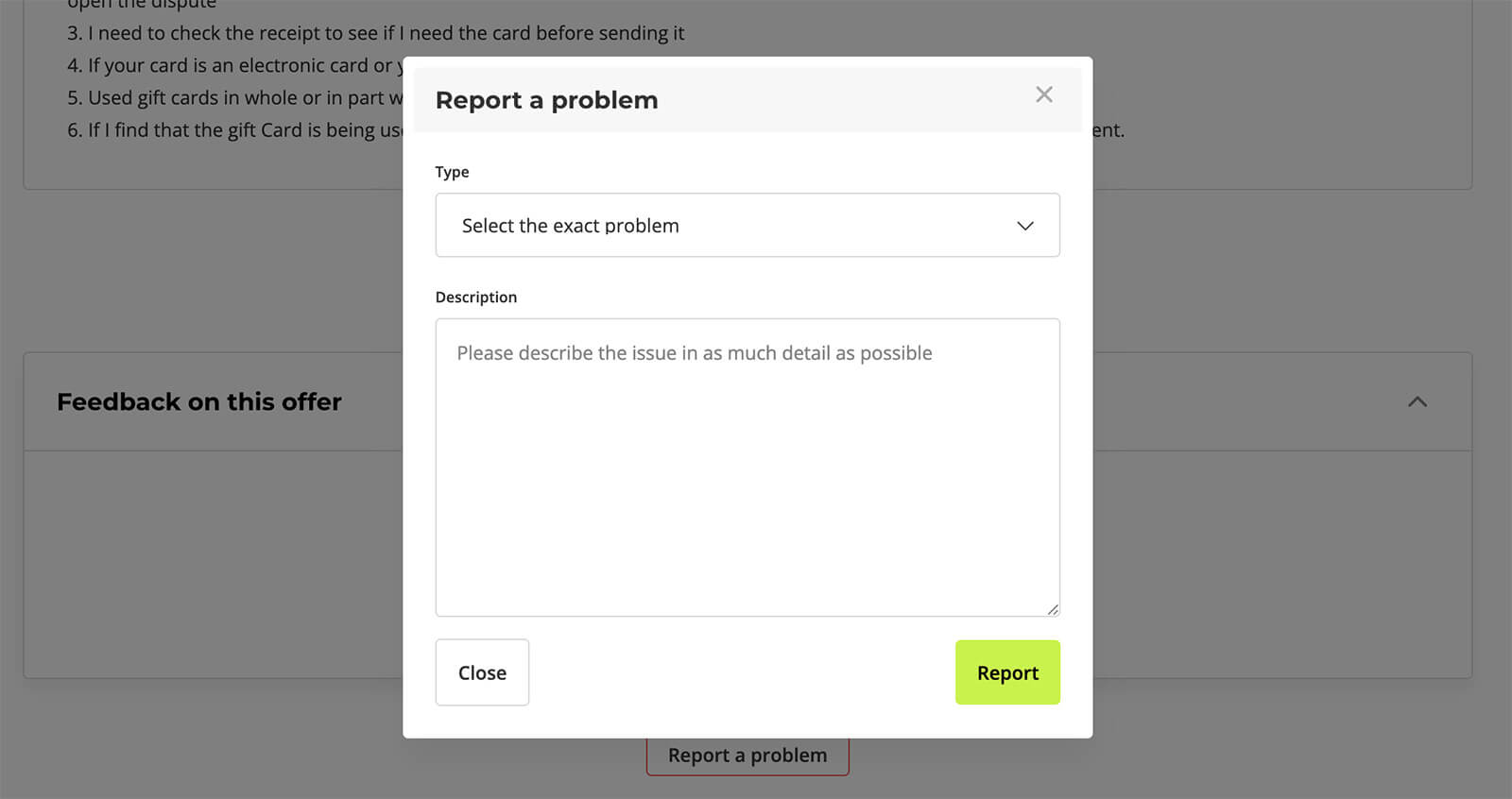

| Dispute Resolution | Admin access to trade chat; payment proof review; fund release controls; appeal mechanism; case history log | Core |

| User Wallets | Built-in hot wallets; BTC, ETH, USDT (ERC20/TRC20/BEP20); multi-sig cold storage for platform reserves | Core |

| KYC / AML | 3-tier KYC (email → ID + selfie → proof of address); SumSub/Jumio integration; AML transaction monitoring | Core |

| Reputation System | Trade rating (positive/neutral/negative); feedback with comment; trust score display; badge tiers for top traders | Core |

| Live Trade Chat | In-trade secure messaging; file upload for payment proof; admin monitoring; dispute trigger button | Core |

| Admin Panel | User management; KYC approval queue; dispute queue; fee configuration; fraud monitoring dashboard | Core |

| Anti-Fraud | Gift card verification API; velocity limits for new accounts; delayed release rules; chargeback monitoring | Security |

| Affiliate Program | Referral link generation; commission tracking; multi-tier levels; payout management | Optional |

| Notifications | Email + SMS + push for trade events; admin alerts for disputes and suspicious activity | Core |

| Mobile Apps | Native iOS + Android; biometric login; push notifications; full trade/wallet/chat functionality | Core |

| Multi-language | UI localization; RTL language support (Arabic, Persian); regional currency display | Optional |

A production escrow system is a 5-state trade machine:

Initiated → buyer and seller agree on terms, seller's crypto is locked in escrow

Paid → buyer marks payment as sent (with proof uploaded to chat)

Confirmed → seller confirms receipt of payment

Released → escrowed crypto transfers to buyer's wallet

Disputed → either party triggers admin intervention

Each state transition has a configurable time constraint. If the seller doesn't confirm within a set window (typically 30–60 minutes for bank transfers, 15 minutes for instant payments), the trade enters automatic dispute mode. This prevents sellers from holding crypto indefinitely after payment is confirmed.

The basic attack: a fraudster pays for crypto with an Amazon or Google Play card. The seller releases the crypto. The fraudster reports the card as stolen. The card is invalidated. The seller has received nothing; the crypto is gone.

Technical mitigations to build in from day one:

Balance verification API. Before escrow release on any gift card trade, integrate with a gift card verification service (CardCash, GiftCards.com, or direct retailer APIs) to confirm the card has the claimed balance and hasn't already been redeemed.

Trade velocity limits. Cap how many gift card trades a single account can complete per day and per week until they establish a verified reputation score. New accounts with zero reputation should not access high-value gift card trades.

Delayed release for new accounts. For accounts under 30 days old or fewer than 10 completed trades, add a mandatory 15–30 minute hold after "payment confirmed" before automatic release — enough time to catch early fraud signals.

PayPal chargeback protection. PayPal buyers can file chargebacks up to 180 days post-transaction. Never allow PayPal for crypto P2P trades without explicit chargeback-risk acknowledgment, account age restrictions, and — for higher values — requiring the buyer to have a verified identity tier.

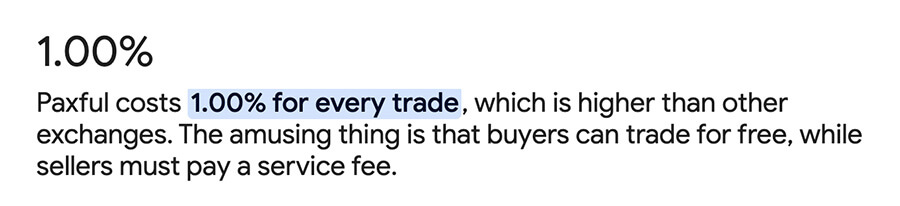

Revenue example: 1,000 daily trades at an average transaction size of $100 with a 1% fee = $1,000/day in platform revenue. Add listing fees, withdrawal charges, and affiliate revenue — and you have a business that scales with user growth, not with your own capital deployment.

Realistic 2026 costs: $25,000–$50,000 for a production-ready white-label deployment with regional payment integration and basic mobile apps. Scripts priced at $1,000–$5,000 are typically unaudited codebases that require significant additional development before they handle real user funds reliably.

Best for: Founders who want to validate a regional market before committing to full custom development. Launch fast, prove the business, then invest in custom features.

Costs: $50,000–$120,000 for a full custom P2P platform with advanced anti-fraud, native mobile apps, and regional payment integrations. Enterprise-grade platforms with institutional compliance run $120,000+.

Best for: Funded startups targeting regulated markets (US, EU, UK), platforms planning multi-region deployment, or teams building a long-term P2P business rather than an MVP.

FinCEN MSB (US): Any platform facilitating crypto-to-fiat P2P trades must register as a Money Services Business with FinCEN — regardless of where fiat payment flows. Paxful's $3.4M fine in 2023 established this clearly. Registration takes up to 180 days and requires a documented BSA/AML program and designated compliance officer. Start on day one of your project.

State MTLs: Beyond federal MSB registration, most US states require a Money Transmitter License. New York's BitLicense is the most demanding. Practical approach: launch in states with lighter requirements first, expand as licenses are obtained.

Gift card payment classification: Accepting gift cards for crypto in several US states may qualify as money transmission requiring a state MTL even when the platform holds no fiat. Verify your specific payment method mix with a crypto-specialized attorney before US launch.

FATF Travel Rule: For transactions above $1,000 (lower in some jurisdictions), VASPs must share originator and beneficiary information. P2P exchanges must determine whether the Travel Rule applies to their escrow model — it typically applies to the crypto leg of the transaction.

Non-custodial P2P: If your platform uses on-chain atomic swaps with no custodial escrow, the regulatory profile changes significantly. You're closer to a DEX than a traditional P2P exchange, which reduces money transmission exposure. Worth considering if your target market has high regulatory sensitivity.

A Paxful clone script is a pre-built P2P crypto exchange platform replicating the core mechanics of Paxful: escrow-protected trading, offer matching, multi-payment support, reputation system, and dispute resolution. You get a production-ready codebase to launch your own branded P2P exchange without building from scratch. Unlike Paxful (which suspended operations in 2023), you control your platform, your market focus, and your compliance setup.

Realistic 2026 costs: white-label P2P script with core features and regional customization — $25,000–$50,000. Custom development with advanced fraud prevention, full mobile apps, and compliance tooling — $50,000–$120,000. Enterprise-grade platform with institutional compliance and multi-region deployment — $120,000+. Scripts priced at $1,000–$5,000 are typically unvetted codebases that require significant additional development before they safely handle real user funds.

Yes, but gift cards require specific fraud mitigations: balance verification API before escrow release, trade velocity limits for new accounts, and delayed release rules. Gift card fraud is the highest-volume attack vector on P2P platforms — it was a primary factor in FinCEN's $3.4M enforcement action against Paxful in 2023. Also verify your jurisdiction: accepting gift cards for crypto may require a Money Transmitter License in several US states.

Yes. FinCEN's 2023 enforcement action against Paxful confirmed that escrow-based P2P platforms are classified as Money Services Businesses requiring federal MSB registration regardless of where fiat payments flow. Most US states additionally require Money Transmitter Licenses. Plan for federal MSB registration (up to 180-day processing) and state-level licensing from day one of the project — not post-launch.

In custodial escrow (Paxful model), your platform's backend holds the crypto during the trade — you control the keys. In non-custodial escrow (atomic swap model), a smart contract holds the crypto and releases it based on cryptographic conditions without any party controlling the keys. Custodial is simpler to implement and easier to dispute-resolve; non-custodial reduces your regulatory exposure as a money transmitter. Most production P2P exchanges use custodial escrow with transparent audit trails.

White-label with standard features and regional payment integration: 6–10 weeks. Custom development with advanced fraud prevention, gift card verification APIs, and native mobile apps: 12–18 weeks. FinCEN MSB registration runs in parallel and takes up to 180 days — start it on day one of the project, not after launch. State MTL applications should also start early as processing times vary widely by state.

Any method where a seller and buyer can agree on terms — the P2P model is payment-agnostic by design. Standard implementations include bank transfers (ACH, SEPA, SWIFT), mobile money (M-Pesa, MTN, Airtel Money), PayPal and Venmo, gift cards (Amazon, Google Play, Steam), and cash for in-person trades with location matching. Fraud risk and compliance requirements differ significantly by payment type — gift cards and PayPal require the most operational attention and the strictest velocity controls.

On a P2P exchange, users trade directly with each other through an escrow-mediated marketplace — fiat payment happens outside the platform. On a DEX, users swap tokens on-chain through a smart contract AMM or order book with no fiat involved. P2P covers the fiat-to-crypto use case that DEXes can't — local bank transfers, mobile money, and 300+ payment methods. The competitive advantage of P2P is access: it lets users in developing markets buy crypto with whatever payment method they already use, not with crypto they don't yet have.