Introduction: Why NFT Real Estate Marketplace Development Is Booming

NFT real estate is no longer a niche experiment — it's a working infrastructure being adopted by US-based startups, investment funds, and property developers right now. The core idea is straightforward: tokenize the ownership rights of a physical property on a blockchain, issue tradable digital assets (NFTs or security tokens), and let investors participate from anywhere in the world with as little as $100.Traditional real estate transactions carry structural inefficiencies that have remained unchanged for decades. Purchasing a property in the US typically requires a six-figure down payment, months of due diligence, a stack of legal agreements, and a web of intermediaries — brokers, escrow agents, title companies — each taking a fee. For fractional investors or international buyers, the barriers are even higher.

NFT-based tokenization removes several of these layers. The same apartment building that once required $500,000 to enter can be split into 10,000 tokens at $50 each, with ownership, dividend rights, and transfer logic enforced automatically by a smart contract. No broker required to process the resale. No title company needed to record the transfer.

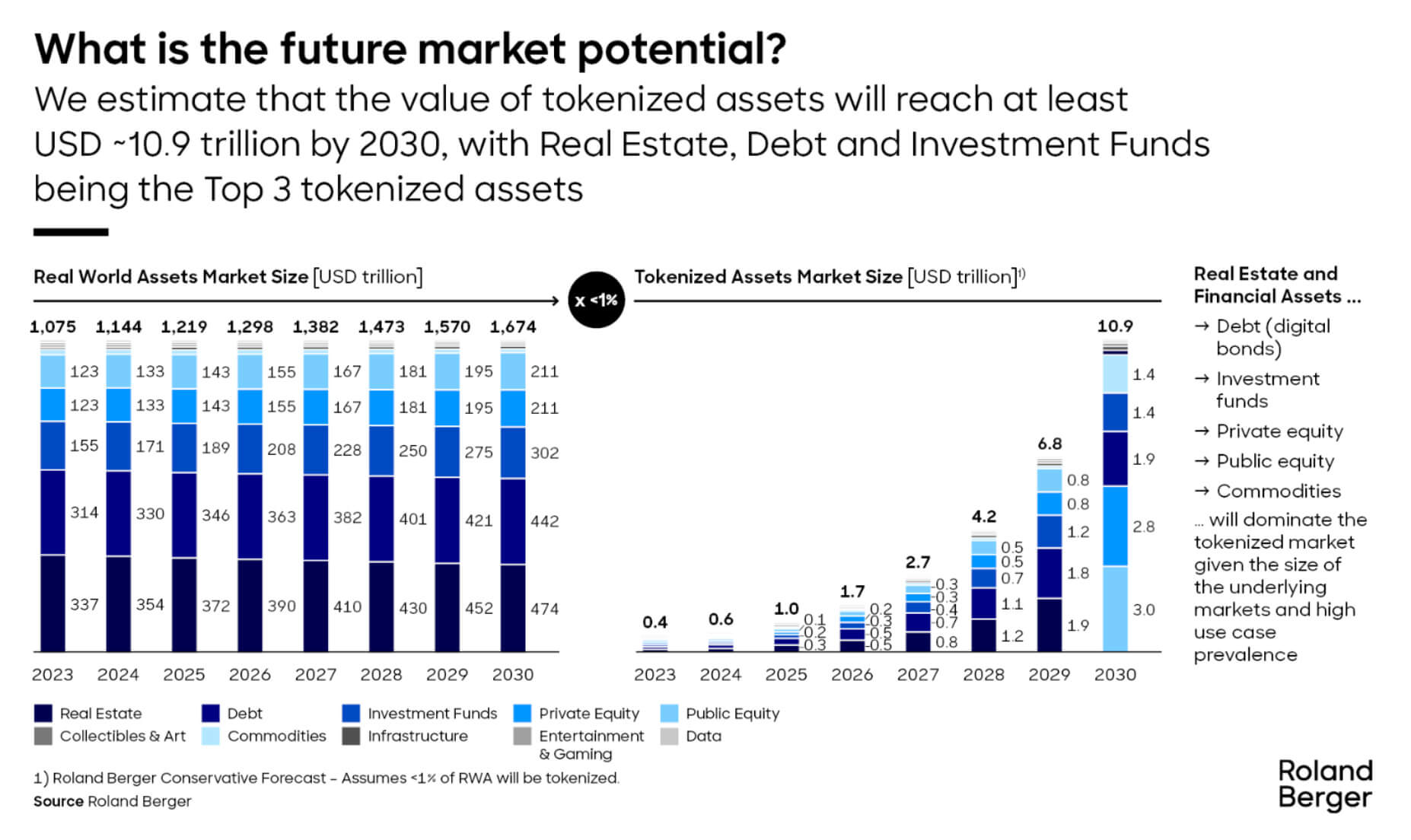

Today, tokenized real estate accounts for roughly 0.2% of the global real estate market. The US, Switzerland, Singapore, and the UK lead adoption, with dozens of specialized platforms already operational. The window for first-mover advantage is open, but it's narrowing — particularly in the US, where SEC regulatory clarity is accelerating institutional interest.

This guide covers what you actually need to build a production-ready NFT real estate marketplace: the token standard decisions, smart contract architecture, legal compliance structure for the US market, full platform feature scope, and the investment mechanics that drive user adoption. If you're a founder, developer, or product team evaluating this space, this is the technical and strategic roadmap you need.

How NFT Real Estate Tokenization Works

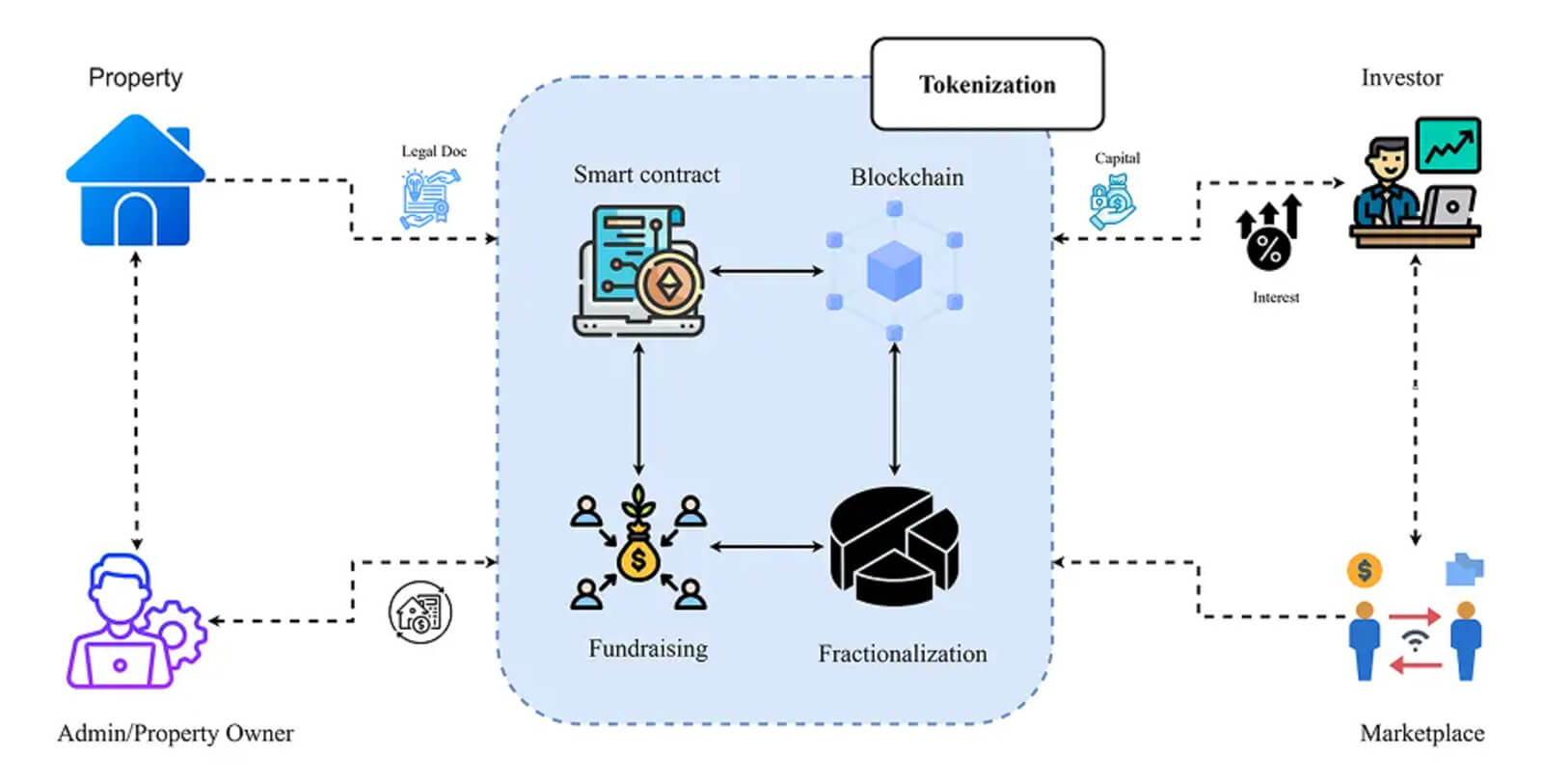

At its core, real estate tokenization converts a property's ownership rights into blockchain-based digital assets. Each token represents a fractional interest — either direct equity in the property or membership interest in a legal entity that owns it. The token is enforced by a smart contract, which automates transfers, dividend distribution, and compliance checks without manual intervention.

Step 1: Legal Structuring — The Foundation Everything Else Rests On

A common misconception: you can tokenize a property by simply minting an NFT with its address in the metadata. You cannot. Without a legal wrapper, the NFT is just a JPEG with a property photo — it carries no enforceable ownership rights and will not survive regulatory scrutiny in the US.The most legally defensible structure currently used in US-based platforms is the Serial LLC model (Delaware jurisdiction). Here's how it works in practice:

Each Series LLC is legally isolated from all others: if one asset encounters legal or financial trouble, it cannot affect other properties on the platform. This structure is fully compliant with SEC security token offering requirements and is the architecture used by established US platforms including those registered with the SEC as Reg D or Reg A+ offerings.

This legal isolation is not a bureaucratic detail — it is the product. Without it, investors have no enforceable claim. Platforms that skip this step typically issue tokens that are legally unenforceable and expose both themselves and their users to significant regulatory risk.

Step 2: Choosing the Token Standard — ERC-721 vs ERC-1155 vs Custom

The choice of token standard directly affects gas costs, marketplace compatibility, fractional logic, and secondary market mechanics. This is a technical decision that has significant product consequences.| Standard | Best For | Fractional Support | Gas Efficiency | Marketplace Support |

| ERC-721 | Whole property NFTs, unique assets | Requires external fractionalizer (e.g., Fractional.art) | Low (one tx per token) | OpenSea, Rarible, LooksRare |

| ERC-1155 | Fractional models, batch minting | Native semi-fungibility | High (batch operations) | OpenSea, Rarible (partial) |

| ERC-20 | Fungible property shares (like stock) | Full fungibility | High | DEX-compatible, not NFT marketplaces |

| Custom (BSC/Polygon) | Low gas environments, retail investors | Configurable | Very high (10–50x cheaper than ETH mainnet) | Platform-native only |

On Ethereum mainnet, a single minting transaction at the time cost $15–40 in gas — destroying the economics of small fractional purchases. BSC reduced that to under $0.50. We implemented a "1 token = 1 sq.m". model: a 120 sq.m. apartment generates exactly 120 tokens, each carrying proportional dividend rights encoded directly in the smart contract. The contract was deployed via Hardhat, verified on BscScan, and integrated with the platform's backend via Web3.js event listeners.

Step 3: Smart Contract Architecture

The smart contract is not a simple token wrapper — it's the operational logic of the entire platform. A production-ready real estate NFT contract needs to handle the following:- Minting with property metadata: Each token batch is linked to a specific property via IPFS-hosted JSON metadata (address, sq.m., legal entity reference, property photos, expected yield).

- Ownership transfer logic: ERC-1155 safeTransferFrom with KYC gate — transfers only execute if both sender and receiver have passed identity verification.

- Dividend distribution: Admin triggers a distribution function that calculates each holder's proportional share based on current token balance and sends stablecoin (USDC/USDT) accordingly. Gas optimization is critical here — looping over thousands of holders on-chain is prohibitively expensive; off-chain calculation with on-chain settlement is the standard approach.

- Secondary market controls: Transfer restrictions can be enabled/disabled at the contract level — essential for platforms awaiting regulatory clearance on secondary trading.

- Token status management: Coming Soon → Live → Sold Out state transitions, with automatic lock on new purchases when supply is exhausted.

Development stack: Solidity (contract logic), Hardhat (local testing + deployment), OpenZeppelin (audited base contracts for ERC-1155, AccessControl, Pausable), IPFS / Pinata (metadata storage), Etherscan / BscScan (contract verification).

Before mainnet deployment, the contract must be audited by a third-party security firm. Unaudited contracts in a financial application are not acceptable — not for investors, not for regulators, and not for any reputable marketplace that might list your tokens.

Step 4: Minting and Metadata

Metadata is the on-chain identity of each property token. It must be stored on decentralized infrastructure (IPFS, Arweave) — not on your own server. If your server goes down, all metadata disappears and the tokens lose their reference data.A production metadata JSON for a real estate NFT looks like this:

{

"name": "Downtown Apartment — Token #47 of 120",

"description": "Fractional ownership token representing 1 sq.m. of a 120 sq.m. residential apartment. Holder receives proportional monthly rental income".,

"image": "ipfs://QmXyZ.../apartment_main.jpg",

"external_url": "https://platform.com/properties/downtown-apt-001",

"attributes": [

{"trait_type": "Property Type", "value": "Residential"},

{"trait_type": "Location", "value": "Austin, TX"},

{"trait_type": "Total Tokens", "value": "120"},

{"trait_type": "Token Represents", "value": "1 sq.m".},

{"trait_type": "Legal Entity", "value": "Platform Holding Series LLC — Series #14"},

{"trait_type": "Expected Annual Yield", "value": "8-12%"},

{"trait_type": "Year Built", "value": "2019"}

]

}

Once metadata is pinned to IPFS and the contract is deployed, minting is triggered through the admin panel — the platform operator initiates a batch mint that creates all tokens for a given property in a single transaction (gas-efficient with ERC-1155). Each minted token becomes immediately visible on blockchain explorers and in the platform's marketplace.

How to Build an NFT Real Estate Marketplace: Technical Architecture

Building a tokenization platform is a different challenge from building a general-purpose NFT marketplace. The feature scope is broader, the compliance requirements are stricter, and the UX must serve retail investors who have zero crypto experience — not DeFi power users. Based on our development practice, here is the full technical architecture of a production-ready platform.Core Platform Modules

| Module | Key Features | Technical Notes |

| Property Marketplace | Listing cards, search & filter by country/type/status, sell-out progress bar, property detail page with photos/financials/map | Real-time sold% via WebSocket; statuses: Coming Soon / Live / Sold Out driven by token supply; sortable by first publication date |

| Smart Contract Layer | Token minting, ownership transfer, dividend distribution, secondary market on/off toggle | ERC-1155 or custom standard; Hardhat deploy; OpenZeppelin base; off-chain dividend calc + on-chain settlement |

| Wallet & Payments | Fiat deposit (bank wire, credit card), crypto deposit (BTC, ETH), fiat↔crypto swap, withdrawal requests | Payment gateway API (Stripe / Coinbase Commerce); masternode integration; instant exchange via third-party liquidity provider |

| KYC / AML / Compliance | Government ID upload, accredited investor questionnaire (US), Customer Agreement e-sign, 2FA, anti-phishing | Third-party KYC provider (Jumio / Sumsub); dynamic PDF generation; SEC-compliant accreditation gate for US users |

| Admin Panel | Property CRUD, token price control, manual balance adjustment, dividend distribution trigger, KYC review, user management, withdrawal approval | Role-based access control; drag-and-drop photo ordering; forced status overrides; waitlist management dashboard |

| Secondary Market | Peer-to-peer token resale, order book or fixed-price listings | Disabled by default pending regulatory clearance; unlocked via admin toggle; users notified via email on activation |

| Notification System | Email verification, KYC status updates, dividend payments, secondary market activation, waitlist confirmations | 24h expiry on email confirmation links; Zendesk ticketing integration for support |

| Mobile Apps | iOS + Android native with full feature parity to web | Responsive registration flows; adaptive KYC document capture; mobile-optimized marketplace cards |

US Regulatory Compliance: The Accredited Investor Flow

For any platform operating in the US, SEC compliance is non-negotiable. Real estate tokens that carry profit rights (rental income, appreciation) are almost certainly classified as securities under the Howey Test. This means the platform must operate under an exemption — typically Regulation D (506b/506c) for accredited investors only, or Regulation A+ for wider public participation.

The accredited investor verification flow must be built directly into the registration process and cannot be an afterthought. Here is the compliant multi-step flow from our production implementation:

If the user selects "None of the above", access is blocked with a clear explanation and an estimated date when the platform plans to open to non-accredited investors under Reg A+. The accreditation declaration is stored with a legally binding acknowledgment: the user confirms they may be permanently banned for providing false information. This declaration feeds directly into the platform's compliance records for SEC audit purposes. After accreditation, the user proceeds to KYC document upload and Customer Agreement e-signature.

The Customer Agreement is generated dynamically as a PDF with the user's name, date, and accreditation status pre-filled. Upon e-signature, it is stored in the user's profile under "My Documents" and in the admin panel's compliance archive. This document chain — accreditation declaration + KYC + signed agreement — is what allows the platform to demonstrate regulatory compliance during an SEC review.

The Waitlist Mechanic: Capturing Demand Before Launch

A production marketplace needs to handle the period before a property goes live — and the moment it sells out. Simply showing a disabled "Invest" button is a missed opportunity. The correct pattern is a waitlist system.The waitlist email confirmation uses a 24-hour expiry link to prevent fake sign-ups from inflating demand metrics. For registered users, the waitlist entry is linked to their account, which simplifies the conversion to actual investment once the offering opens.

Where to Buy and Trade NFT Properties: Platform Overview

There are two distinct categories of platforms currently operating in the NFT real estate space, and they serve different user profiles and use cases.General-Purpose NFT Marketplaces

OpenSea

OpenSea is the largest NFT marketplace by volume and supports tokenized real estate assets alongside art, gaming, and collectibles.

OpenSea operates primarily on Ethereum and Polygon. Listing a property NFT requires connecting a wallet (MetaMask, Coinbase Wallet), uploading property media, defining metadata, setting royalties, and signing the listing transaction. OpenSea does not perform KYC or legal compliance checks — it is infrastructure, not a regulated platform. For fractional property tokens that qualify as securities, listing on OpenSea without SEC registration creates significant legal exposure.

Rarible

Rarible supports minting on Ethereum, Tezos, Polygon, and Flow. It offers more granular smart contract control than OpenSea, including custom royalty logic and flexible metadata schemas — useful for property tokens that require non-standard attribute structures. Like OpenSea, it provides no compliance layer.

Specialized Real Estate Tokenization Platforms

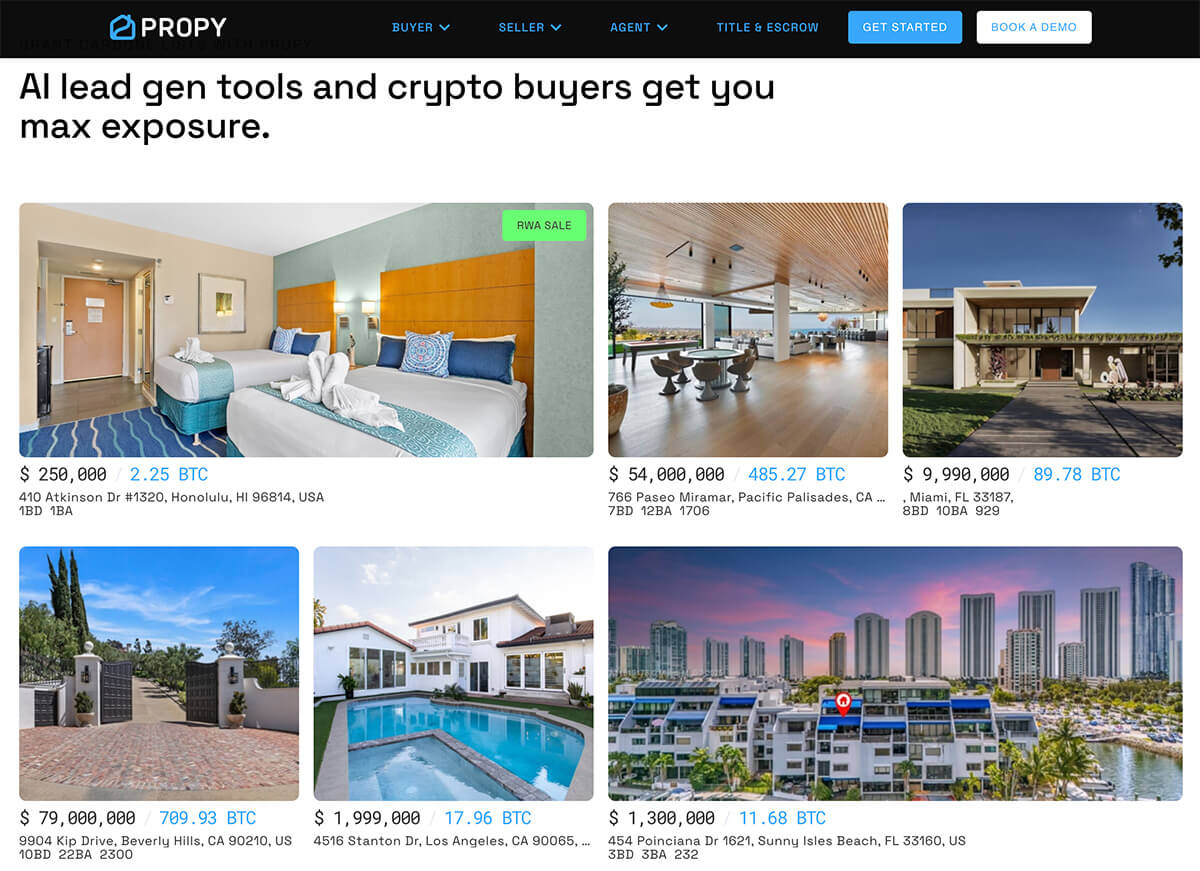

Propy

Propy is built exclusively for real estate and integrates the NFT transfer with the legal title transfer process. In 2022, Propy facilitated the first US real estate sale via NFT — a private property in Florida for over $653,000 in cryptocurrency. It handles KYC, escrow, and deed transfer in a single workflow, making it one of the few platforms where NFT ownership maps directly to legally recorded title.

Metropoly

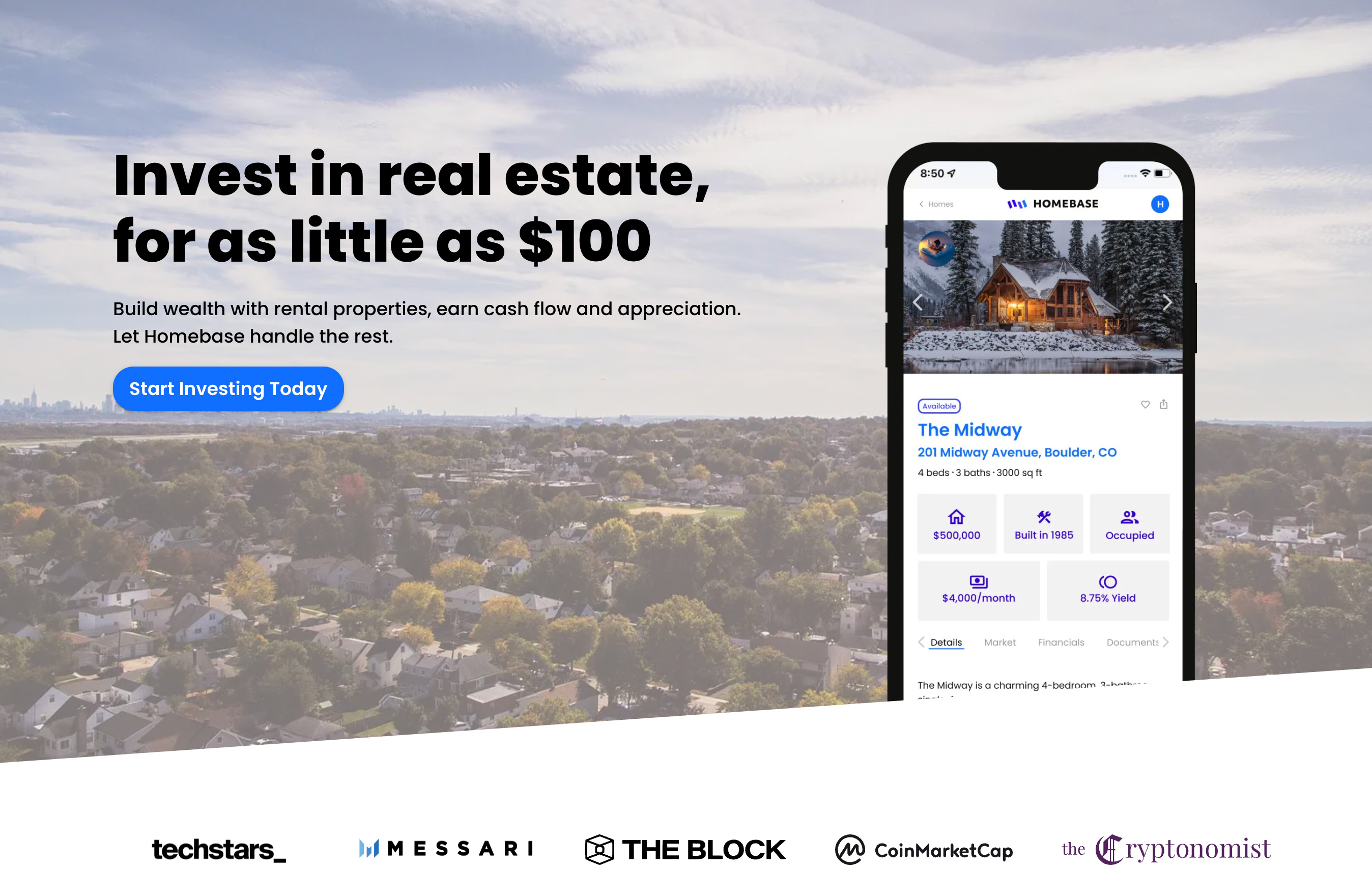

Metropoly enables fractional ownership with minimum investments starting from $100. Properties are divided into micro-shares representing as little as 0.01% of the asset. A real-time dashboard tracks rental income and price appreciation per token, making the investment mechanics transparent to retail users.Homebase

Homebase is focused on US rental properties with fractional NFTs. Dividends are distributed monthly in USDC stablecoins, eliminating the volatility risk of receiving rental income in native cryptocurrency. Full KYC is required; the platform currently accepts US investors only.

RedSwan

RedSwan targets commercial real estate — offices, hotels, large residential complexes — and restricts participation to accredited investors. Returns are tied to leasing income and asset appreciation. It represents the institutional end of the fractional NFT market.Decentraland

Decentraland operates in the virtual land segment — parcels in a metaverse environment rather than physical properties. While conceptually different from physical real estate tokenization, it demonstrates that digital land with no physical backing can carry real economic value through scarcity, utility, and speculative demand.Platform Selection Guide

| Use Case | Recommended Platform | Key Consideration |

| Prototype / experiment with minting | OpenSea, Rarible | No compliance layer — not suitable for securities |

| Legally compliant US property sale | Propy, RedSwan | Full KYC + title transfer integration |

| Retail fractional investment ($100+) | Metropoly, Homebase | Low minimums; USDC dividends; dashboard UX |

| Commercial / accredited investor only | RedSwan | High-value assets; SEC-registered offerings |

| Virtual land / metaverse | Decentraland, The Sandbox | No physical asset backing; speculative |

| Building your own platform | Custom development | Full control over compliance, UX, token economics |

Step-by-Step: How to Create and Mint an NFT Real Estate Asset

Minting a real estate NFT is not a one-click process. It requires legal preparation, smart contract development, metadata engineering, and compliance integration before a single token reaches a buyer. Here is the complete production workflow.Step 1: Legal Entity and Property Documentation

- Register a Series LLC (Delaware) as the legal owner of the property being tokenized.

- Obtain and verify all property title documents, ownership history, and existing liens.

- Draft the token purchase agreement defining what each token represents (equity, income rights, voting rights).

- Confirm SEC exemption pathway (Reg D 506b/506c or Reg A+) with legal counsel before proceeding.

Step 2: Blockchain and Token Standard Selection

- Ethereum mainnet + ERC-1155: Best for high-value properties where gas costs are insignificant relative to token price.

- Polygon + ERC-1155: Strong choice for retail-focused platforms — gas fees under $0.01, OpenSea compatible.

- BSC: Viable for budget retail platforms; lower ecosystem trust than Ethereum/Polygon.

- Tezos / Flow: Lower energy consumption; smaller developer ecosystem.

Selection criteria: transaction cost per mint, cost of dividend distribution at scale, marketplace compatibility, and your legal jurisdiction's accepted blockchain infrastructure.

Step 3: Metadata Creation and IPFS Storage

Create the property metadata JSON (see schema above). Upload property photos and documents to IPFS via Pinata or NFT.Storage. Store the IPFS CID in the metadata JSON as the image and document references. Pin the metadata file itself to IPFS and record the final CID — this becomes the tokenURI for the contract.Step 4: Smart Contract Development and Audit

- Write the contract in Solidity using OpenZeppelin's ERC-1155 base with AccessControl and Pausable extensions.

- Implement KYC-gated transfers:

require(kycRegistry[to] == true, "Recipient not KYC verified") - Implement dividend distribution with off-chain snapshot + on-chain payment pattern to avoid gas limits.

- Add secondary market toggle function (admin-only, initially locked).

- Deploy to testnet (Goerli / BSC Testnet) and run full test suite with Hardhat.

- Submit to third-party audit before mainnet deployment.

Step 5: Minting

- Deploy audited contract to mainnet and verify source code on block explorer.

- Execute batch mint via admin panel — all tokens for the property created in a single transaction.

- Confirm all token IDs are visible on-chain and metadata resolves correctly via tokenURI.

Step 6: Platform Listing and Compliance Verification

- Create the property listing in the admin panel: photos, financials, legal entity reference, expected yield, dividend schedule.

- Set initial status to "Coming Soon" with waitlist enabled.

- Verify KYC gate is active — no token purchase should execute without verified identity.

- Test full purchase flow on staging environment: wallet connect → KYC check → payment → token delivery → balance update.

- Set "Launch Date" in admin panel to activate the "Live" status and open purchases.

Step 7: Distribution and Secondary Market

- Implement a manual dividend trigger in the admin panel: admin inputs the rental income amount for a property → system calculates each holder's share → distributes USDC proportionally.

- Secondary market remains disabled until SEC/regulatory clearance is obtained; notify waitlisted users via email when activated.

A hard block on missing optional fields creates operational bottlenecks and forces admins to enter placeholder data, which creates legal liability. The correct pattern: SAVE allows incomplete data; PUBLISH enforces all required fields. Optional fields (launch date, dividend date, lot size for condos) should degrade gracefully to TBA or an em dash rather than blocking the action.

NFT Real Estate Marketplace: Must-Have Features Checklist

Below is the complete feature scope for a production-ready NFT real estate marketplace, based on real platform development. This is the baseline — not the minimum viable product.| Feature Area | User-Facing Features | Admin Features |

| Authentication | Registration, login, 2FA, password recovery, anti-phishing, email verification (24h link expiry) | User management, role assignment, account suspension |

| Onboarding / Compliance | KYC document upload (Passport / Driver License / National ID), accredited investor questionnaire (US), Customer Agreement e-sign, certificate in "My Documents" | KYC review and approval queue, accreditation status override, compliance record export |

| Marketplace | Property listings with status badges (Soon / Live / Sold Out), sell-out progress bar, search, filter by country/type/yield, property detail page with photos/map/financials | Property CRUD, photo ordering (drag-and-drop), status management (forced override), unpublish/republish, launch date scheduling |

| Investment Flow | Token purchase (quantity selector, order summary, buying power display), order history, portfolio dashboard with P&L and dividend tracking | Token price control, total investor count display, offering detail fields (Purchase Price, Closing Costs, Platform Fee, Improvements Reserve) |

| Waitlist | "Join Waitlist" modal on Coming Soon / Sold Out listings, desired investment size input, confirmation email | Waitlist dashboard per property, export for investor relations |

| Wallet & Payments | USD deposit (bank wire), crypto deposit (BTC/ETH), fiat↔crypto swap, withdrawal request (bank account details), transaction history | Manual balance adjustment, withdrawal approval/rejection workflow, exchange rate management |

| Dividends | Monthly rental income distribution to token holders (USDC), dividend history, estimated first dividend date display | Dividend distribution trigger per property, amount input, confirmation log |

| Secondary Market | Token resale listings, buyer/seller matching (inactive until SEC clearance) | Secondary market enable/disable toggle per property, user notification on activation |

| Support | Ticket submission (Zendesk integration), FAQ page, Cookie Policy modal (non-navigating) | Zendesk dashboard, ticket routing by category |

Blockchain Infrastructure Comparison for Real Estate Platforms

Choosing the right blockchain for your NFT real estate marketplace affects gas costs, scalability, ecosystem trust, and long-term regulatory positioning. Here is a practical comparison based on production deployment experience.| Blockchain | Token Standards | Avg. Gas per Mint | TPS | Marketplace Ecosystem | Best For |

| Ethereum | ERC-721, ERC-1155, ERC-20 | $5–40 (variable) | ~15 | OpenSea, Rarible, LooksRare | High-value assets, institutional credibility |

| Polygon | ERC-721, ERC-1155 | <$0.01 | ~65 | OpenSea (Polygon), QuickSwap | Retail fractional platforms, low ticket sizes |

| BSC | BEP-721, BEP-1155 | <$0.50 | ~100 | PancakeSwap, platform-native | Cost-sensitive retail platforms |

| Tezos | FA2 | <$0.01 | ~52 | Objkt.com, Rarible (Tezos) | Eco-focused platforms, lower developer resources |

| Cardano | Native tokens (via NMKR) | ~$0.10–$0.50 | ~250 | NMKR, JPG.Store | Long-term infra bets; smaller current ecosystem |

Advantages and Risks of NFT Real Estate Investment

NFT real estate offers a structurally different value proposition compared to traditional property investment. Understanding both sides is essential before committing capital — or building a platform around this model.

Advantages

Accessibility at scale. Fractional ownership drops the minimum investment from six figures to $50–$500. A $2M commercial property can be split into 20,000 tokens at $100 each, opening participation to investors who would never qualify for a traditional commercial real estate syndication.Programmable dividends. Rental income distribution that traditionally required a property manager, accountant, and wire transfer to each investor is reduced to a single admin action that triggers a smart contract function. Distribution happens in minutes, not weeks. Stablecoin payouts (USDC) eliminate the currency conversion problem for international investors.

Transparent ownership chain. Every token transfer, every dividend payment, every change in property status is recorded on a public blockchain. Unlike opaque real estate syndication structures where investors rely entirely on the operator's reporting, blockchain-based ownership is independently auditable by anyone.

Liquidity potential. Traditional real estate is one of the most illiquid asset classes — exiting a fractional syndication position can take months or years. NFT tokens can theoretically be resold on a secondary market in minutes. In practice, liquidity depends on market depth, but the infrastructure for rapid exit exists.

Risks

Regulatory classification risk. In the US, tokens carrying profit rights from a common enterprise almost certainly qualify as securities under the Howey Test. Platforms that ignore this and list unregistered securities face SEC enforcement, potential criminal liability, and mandatory investor remediation. This risk is not theoretical — the SEC has already pursued enforcement actions against multiple crypto platforms.Platform dependency. Token holders are exposed to operational risk of the issuing platform. If the platform shuts down, the admin panel that controls dividend distribution disappears. Smart contract dividend functions can be designed to operate autonomously, but most production implementations still require admin triggers — meaning centralized operational risk persists.

Liquidity is not guaranteed. Secondary market depth on specialized platforms is thin. A token priced at $100 is worth $100 only if a buyer appears. In a market downturn or following negative news about a specific property, tokens can become effectively illiquid for extended periods.

Smart contract risk. Unaudited contracts are a fundamental security risk. A vulnerability in dividend distribution logic or ownership transfer can result in fund loss with no recourse. The immutable nature of blockchain means bugs cannot be patched after deployment without a complete migration.

Legal enforceability. An NFT is a blockchain record. Whether it constitutes legally enforceable property ownership depends entirely on the legal wrapper (LLC structure, signed agreements, jurisdiction). Platforms that issue tokens without proper legal structures leave investors with no enforceable claim against the underlying asset.

Investment Potential and Strategies

For investors evaluating NFT real estate as an asset class, the financial mechanics work as follows. Each token generates two potential return streams: rental yield (periodic cash flow) and capital appreciation (token price increase as property value rises or secondary market demand grows).Yield Expectations

Rental yield on NFT real estate platforms currently ranges from 6% to 22% annually, depending on property type, location, and platform fee structure. Commercial properties in high-occupancy markets tend to cluster in the 8–14% range after platform fees. Residential properties in emerging markets can offer higher headline yields with higher vacancy risk.| Monthly Investment | Annual Yield | 10-Year Cumulative Gain |

| $250 | 8% | ~$13,200 |

| $250 | 12% | ~$21,500 |

| $250 | 22% | ~$36,000+ |

These figures do not account for token price appreciation — only the cash flow component. They also assume consistent reinvestment and do not factor platform fees or tax treatment.

Investment Strategies

Dollar-cost averaging is the most defensible approach in a volatile, early-stage market. Allocating a fixed monthly amount ($100–$500) across multiple properties smooths entry price volatility and builds position gradually.Diversification by property type and geography reduces concentration risk. Splitting exposure between US residential, international commercial, and emerging market properties creates a natural hedge against any single market downturn.

Yield focus vs. appreciation focus reflects different risk profiles. Stabilized assets in mature markets offer predictable rental yield with modest appreciation. Emerging market properties or pre-construction tokenizations offer higher appreciation potential with higher vacancy and execution risk.

Secondary market flipping requires deep market knowledge and is higher risk. Purchasing underpriced tokens on secondary markets and reselling after property news (renovations, occupancy improvements, market appreciation) can generate outsized short-term returns but requires active monitoring.

NFT Real Estate Marketplace Development: Cost and Timeline

For founders and product teams evaluating build vs. buy, here is a realistic scope and cost breakdown for a full-featured NFT real estate marketplace based on production development experience.| Development Component | Scope | Estimated Timeline |

| Technical documentation + UI/UX design | Architecture spec, wireframes, design system, component library | 3–4 weeks |

| Smart contract development + audit | ERC-1155 contract, KYC gate, dividend logic, secondary market toggle, testnet + mainnet deploy | 4–6 weeks |

| Web platform (frontend + backend) | Marketplace, investment flow, wallet/payments, KYC integration, notifications | 8–10 weeks |

| Admin panel | Property management, user/KYC management, dividend distribution, financial dashboard | 4–5 weeks |

| Mobile apps (iOS + Android) | Native apps with full feature parity | 6–8 weeks |

| Third-party integrations | KYC provider, payment gateway, Zendesk, blockchain node | 2–3 weeks (parallel) |

| Total (web + admin + contracts) | ~3 months | |

| Total (web + admin + contracts + mobile) | ~4–5 months |

Legal entity registration (Series LLC setup in Delaware) runs in parallel with development and typically takes 2–4 weeks with a US attorney. The two tracks — legal and technical — must converge before any token is sold to a real investor. Attempting to launch without both tracks complete is the most common cause of regulatory exposure in this space.

Conclusion: Building for the Infrastructure Gap

The NFT real estate market is not waiting for the technology to catch up — the technology is ready. What the market lacks is well-engineered, legally compliant platforms that retail and institutional investors can actually trust. Most existing platforms either sacrifice compliance for speed to market or sacrifice UX for compliance complexity. The opportunity is in building both correctly.The technical stack for a production platform is well-defined: ERC-1155 smart contracts on Polygon or Ethereum, Serial LLC legal structure per property, KYC-gated token transfers, off-chain dividend calculation with on-chain settlement, and a UX built for investors who have never touched a crypto wallet. The compliance requirements — accredited investor verification, SEC exemption structuring, customer agreement chain — are non-negotiable for the US market and are the primary differentiator between platforms that scale and those that get shut down.

If you're evaluating NFT real estate marketplace development for your project — whether as a property owner looking to tokenize assets, an investment platform expanding into blockchain, or a startup building fractional ownership infrastructure — the decision framework is the same: start with the legal architecture, define the token economics, then build the platform around those constraints.

Frequently Asked Questions

What is NFT real estate marketplace development?

It is the process of building a platform that tokenizes physical real estate properties into blockchain-based NFTs or security tokens, allowing investors to purchase fractional ownership, receive rental income, and trade their tokens. Development encompasses smart contract engineering, legal entity structuring, KYC/AML compliance integration, marketplace UI, and payment infrastructure.

Which token standard should I use — ERC-721 or ERC-1155?

For fractional real estate (multiple investors per property), ERC-1155 is the practical choice. It supports batch minting of multiple fungible token copies in a single transaction, which is gas-efficient and maps naturally to the "N tokens per property" model. ERC-721 is best for whole-property NFTs where each token represents the entire asset.

Are real estate NFTs considered securities in the US?

In most cases, yes. Tokens that carry profit rights derived from a third party's management of the underlying property satisfy the Howey Test criteria for investment contracts. This means they require SEC registration or an applicable exemption (Reg D 506b/506c for accredited investors, Reg A+ for public offerings). Operating without compliance exposes the platform to enforcement action.

What is the Serial LLC structure used for real estate tokenization?

A Serial LLC (Delaware) is a master legal entity under which separate child LLCs are created for each property. Each child LLC owns one property, and the tokens issued for that property represent legal membership interests in that LLC. This gives token holders legally enforceable ownership rights and isolates each property's legal exposure from others on the platform.

How long does it take to build an NFT real estate marketplace?

A full-featured platform covering web, admin panel, and smart contracts takes approximately 3 months with a dedicated team. Adding native iOS and Android apps extends this to 4–5 months. The smart contract audit and legal entity registration are the critical-path items — both run on fixed timelines that cannot be significantly compressed.

Which blockchain is best for a real estate tokenization platform?

For retail-focused platforms with small ticket sizes ($100–$500), Polygon (ERC-1155) is currently the strongest choice: sub-cent gas fees, OpenSea compatibility, and full Ethereum toolchain support. Ethereum mainnet is preferable for institutional or high-value assets where gas costs are insignificant relative to token price. BSC is viable for cost-sensitive markets outside the US.

How does dividend distribution work in NFT real estate?

Most production platforms use a hybrid model: rental income is calculated off-chain (admin inputs the total rental proceeds for a property), and the smart contract distributes stablecoin (USDC/USDT) to token holders proportionally in a single on-chain transaction. Pure on-chain loops over thousands of holders are gas-prohibitive. The off-chain calculation + on-chain settlement pattern is the industry standard.

What is the minimum investment on NFT real estate platforms?

It varies by platform. Metropoly allows entry from $100; Homebase operates in a similar range. Platforms built on the "1 token = 1 sq.m". model price tokens based on property value divided by square footage — a $250,000 apartment of 100 sq.m. would price tokens at $2,500 each, which is less accessible. Token denomination strategy is a product decision with significant impact on investor acquisition.