In this guide, we review the best crypto friendly banks in the US, UK, Europe, Australia, Canada, and UAE — with a focus on what actually matters for businesses: AML policy, exchange integrations, API availability, and account access for non-residents.

The banks on this list were selected based on their ability to support crypto business operations end-to-end: from receiving payments on-chain to executing SEPA/SWIFT settlements and passing AML checks without account freezes.

What Makes a Bank Truly Crypto Friendly?

The term "crypto friendly" is widely misused. A bank that doesn't block your Coinbase transfer is not the same as a bank that can serve as operational infrastructure for a crypto startup.

When evaluating banks for crypto businesses, there are four hard criteria that separate genuine partners from merely tolerant ones:

| Criteria | What it means in practice | Why it matters |

|---|---|---|

| Exchange compatibility | No blocks on transfers to/from Binance, Kraken, Coinbase, Huobi | Operational liquidity for daily business |

| API access | Documented REST API for automated reconciliation and transaction tracking | Critical for crypto processing systems and off-ramp automation |

| AML transparency | Documented procedure for handling flagged transactions without immediate freeze | Prevents loss of operations when your own AML system returns a transaction |

| Non-resident access | Ability to open an account without being a local entity | Essential for international Web3 startups |

In Europe, the MiCA regulation (Markets in Crypto-Assets) sets binding standards for crypto-asset service providers: licensing, capital adequacy, AML compliance, and custody rules. Banks embracing MiCA aren't just "friendly" — they operate within a defined legal framework that protects your business. In Switzerland, Argentina, Brazil, and the US, cryptocurrency is already accepted for tax payments and salary settlements.

Crypto Friendly Banks for Business: Our Technical Experience

We've built crypto payment infrastructure for clients across Europe and the US. This section reflects what we learned about banking integrations — anonymized, but technically specific.

Case 1: Crypto Processing Platform — Choosing a Banking Partner

The processing architecture had five interaction layers with the financial system: wallet balance tracking (BTC, ETH, USDT TRC20/ERC20, Solana, BNB, USDC, Doge), payment provider orchestration with operation initiation and finalization, automated financial reconciliation, liquidity pool management, and a real-time AML check on all incoming transactions.

The AML module was built to return high-risk transactions before finalization — meaning the bank needed to handle returned transactions without triggering an account review. Most banks that market themselves as "crypto-friendly" in the EU have no documented procedure for this scenario. In practice, traditional banks, even in green-zone jurisdictions, either lack the API documentation needed for automated reconciliation, or their compliance teams interpret any returned transaction as suspicious activity. Both outcomes are fatal for operations at scale.

The microservices architecture required: daily backups of all instances, geo-redundant server infrastructure with automatic failover routing, independent key management for signing operations, and configurable webhook callbacks for each partner project. Banking API limitations were the single most common reason for re-evaluating partners mid-project.

Case 2: Non-Custodial Wallet with DEX Integration — Off-Ramp Problem

During development of a perpetual futures (Perp DEX) module for an existing non-custodial wallet built on TrustWalletCore (iOS + Android), we encountered the off-ramp problem that most Web3 startups face: no classic "crypto-friendly" bank could provide adequate infrastructure for withdrawing funds from L2 networks to a fiat account.

The trading module integrated HyperLiquid as the liquidity source for perpetual contracts, with a full OrderBook supporting Limit, Market, and Stop-Limit orders, isolated and cross-margin modes, and a configurable leverage system. At the deposit/withdrawal layer, the startup needed a bank account capable of processing transactions from DEX addresses without delays or manual review queues.

Parallel development required a fork/PR workflow: client developers maintained their own feature branch while our team developed the futures module independently, with regular pull requests reviewed by the client's tech lead. Banking delays at the off-ramp layer blocked the final testing phase — not because of regulatory issues, but because the bank had no documented SLA for processing transactions originating from smart contract addresses.

Practical conclusion: for projects with a non-custodial wallet and DEX trading, selecting a bank with open API and documented transaction SLAs is more important than the bank's general attitude toward cryptocurrency. "Crypto-friendly" without an API is a marketing claim, not an operational reality.

Best Crypto Friendly Banks in the USA

For US-based crypto startups and Web3 businesses, the choice of bank directly impacts your ability to operate. Below are the banks with the strongest track records for crypto business accounts.

| Bank | Location | Crypto Friendly | Digital Bank | Crypto Wallets |

|---|---|---|---|---|

| Mercury | United States | Yes | Yes | No |

| Juno | United States | Yes | Yes | Yes |

| Capital One Bank | United States | Partially | No | No |

| Anchorage Digital Bank | United States | Yes | Yes | Yes |

Mercury

Mercury is the go-to banking option for US crypto startups, particularly those building in the Web3 and DAO space. Founded in 2017 in San Francisco, it does not support on-account crypto storage but has an explicitly positive policy toward Web3 entities — including allowing frictionless transfers to major exchanges.

Key operational features for crypto businesses:

- Non-resident account opening (fully remote, no US entity required at launch)

- No minimum balance, no monthly fees

- Zero-commission overdraft facility — relevant for businesses with variable crypto revenue cycles

- Clean transfer policy to Binance, Coinbase, Kraken without blocking

- Treasury tools for managing idle fiat between on-chain deployments

Mercury is best suited for early-stage Web3 startups that need a clean USD account with exchange access but don't yet require on-account custody.

Anchorage Digital Bank

Anchorage Digital is the only federally chartered digital asset bank in the US — it received an OCC national banking charter in January 2021. This makes it structurally different from every other bank on this list: it was built for crypto institutions, not adapted for them.

Anchorage serves institutional clients — hedge funds, asset managers, corporations — not retail. Its feature set reflects that:

- Institutional-grade digital asset custody with insurance coverage

- Trading and brokerage execution for large-volume crypto transactions

- Staking and on-chain governance participation on behalf of clients

- Advanced fraud prevention and risk management under federal banking oversight

- Compliance frameworks aligned with OCC, FinCEN, and OFAC requirements

If you're running a hedge fund, crypto asset manager, or corporate treasury with significant digital asset exposure, Anchorage is the only US option with a full federal banking charter behind it.

Juno

Juno is a crypto-native banking platform that bridges fiat and digital assets within a single account. It supports direct purchase, sale, and custody of cryptocurrency alongside a high-yield checking account — and offers a debit card with crypto cashback at select merchants.

Juno is best positioned for individual crypto professionals and small teams who need a unified account rather than separate exchange + bank infrastructure.

Capital One Bank

Capital One is a traditional US bank with a partially crypto-compatible stance. It does not block crypto exchange transfers outright, but it does not offer any built-in crypto services. For crypto businesses that need a large, well-known US bank on their cap table for investor optics, Capital One is worth considering — but it will not satisfy technical integration requirements.

Best Crypto Friendly Banks in the UK

| Bank | Location | Crypto Friendly | Digital Bank | Crypto Wallets |

|---|---|---|---|---|

| Revolut | United Kingdom | Yes | Yes | Yes |

| Monzo | United Kingdom | Yes | Yes | No |

Revolut

Revolut is one of the most technically complete crypto-compatible neobanks available globally. Founded in the UK in 2015, it now holds banking licenses in multiple European jurisdictions and supports 30+ cryptocurrencies with in-app trading.

Revolut features relevant to crypto businesses:

- Multi-currency accounts (USD, EUR, GBP + crypto) within a single interface

- In-app crypto trading with competitive exchange rates across 30+ assets

- International transfers at 0.15% commission for USD payments — significantly below SWIFT standard fees

- Physical and virtual Visa cards with spending controls

- Deposit protection under EU banking regulation (where applicable)

Revolut is best for businesses that need a single platform for multi-currency treasury management combined with direct crypto exposure — without managing a separate exchange account.

Monzo

Monzo is a UK neobank with a crypto-tolerant rather than crypto-native stance. It does not support direct cryptocurrency purchases or on-account wallets, but it processes transfers to major exchanges (Binance, Kraken, Coinbase, Bitstamp) without restrictions — subject to standard AML/KYC checks.

Monzo's competitive advantage is its GBP business account: transparent fee structure, intuitive account management, and reliable operations for UK-based companies. It is the right choice for businesses that process primarily GBP and need a fiat account that won't block exchange transfers — not for teams requiring integrated crypto functionality.

Best Crypto Friendly Banks in Australia

| Bank | Location | Crypto Friendly | Digital Bank | Crypto Wallets |

|---|---|---|---|---|

| Commonwealth Bank of Australia | Australia | Yes | No | Yes |

| Westpac | Australia | Limited | No | No |

Commonwealth Bank of Australia

Commonwealth Bank of Australia (CBA) is the country's largest bank and the most progressive among the traditional Australian Big Four when it comes to digital assets. CBA launched a pilot crypto trading feature directly within its CommBank app — making it one of the few traditional retail banks globally to integrate on-app crypto functionality.

For crypto businesses operating in Australia, CBA provides domestic credibility combined with an explicit digital asset strategy — which reduces the risk of account issues compared to banks with no stated crypto policy.

Westpac

Westpac — one of Australia's original "Big Four" banks (founded 1817) — takes a limited and cautious approach to cryptocurrency. It does not block all crypto-related transfers, but it has historically applied higher scrutiny to transactions involving digital asset exchanges. Suitable as a secondary operational account for Australian entities, not as a primary banking partner for crypto businesses.

Best Crypto Friendly Banks in Canada

| Bank | Location | Crypto Friendly | Digital Bank | Crypto Wallets |

|---|---|---|---|---|

| TD Canada Trust | Canada | Partially | No | No |

| CIBC (Imperial Bank of Commerce) | Canada | Yes | No | No |

TD Canada Trust

TD Canada Trust, a division of TD Bank (one of Canada's Big Five), provides partial crypto compatibility: it accepts transactions involving Bitcoin and other major cryptocurrencies but does not offer integrated crypto services. TD has strong cross-border capabilities between Canada and the US — useful for businesses with North American operations.

CIBC

CIBC (Canadian Imperial Bank of Commerce), formed from the 1961 merger of Imperial Bank of Commerce and Commerce Bank of Canada, is one of Canada's Big Five and the more crypto-progressive of the two options listed here. CIBC explicitly allows cryptocurrency deposit transactions and has a documented stance on digital asset transfers that is more permissive than TD.

Best Crypto Friendly Banks in the UAE

The UAE — particularly Dubai and Abu Dhabi — has emerged as one of the most crypto-progressive jurisdictions globally. VARA (Virtual Assets Regulatory Authority) provides a clear licensing framework for crypto businesses, and local banks have adapted accordingly.

| Bank | Location | Crypto Friendly | Digital Bank | Crypto Wallets |

|---|---|---|---|---|

| Emirates NBD | UAE | Yes | No | No |

| RAKBANK | UAE | Yes | No | No |

| Mashreq Bank | UAE | Yes | No | No |

Emirates NBD

Emirates NBD is the UAE's leading banking group and one of the largest financial institutions in the Middle East. It has adopted a progressive stance on digital assets, supporting crypto business accounts for entities licensed under VARA. For companies establishing a presence in the Dubai crypto ecosystem, Emirates NBD provides the institutional credibility and international correspondent banking network required for serious operations.

RAKBANK

RAKBANK (Ras Al Khaimah National Bank), established in 1976, offers broad retail and corporate banking services and accepts crypto-related business accounts. It is particularly relevant for smaller crypto entities and fintech startups entering the UAE market that need an accessible, customer-centric banking partner without the formality of a tier-1 institution.

Mashreq Bank

Mashreq Bank, established in 1967, is one of the UAE's oldest financial institutions and has become a leader in digital banking innovation across the region. With operations in the Middle East, North Africa, and international markets, Mashreq provides crypto businesses with the geographic reach needed for cross-border digital asset operations in the MENA corridor.

Best Crypto Friendly Banks in Europe

Europe's regulatory landscape post-MiCA (2024) has clarified which banks can and cannot serve crypto businesses. The options below operate within defined licensing frameworks — a critical distinction when your company's AML reporting depends on a compliant banking partner.

| Bank | Location | Crypto Friendly | Digital Bank | Crypto Wallets |

|---|---|---|---|---|

| Wirex | Italy / Europe | Yes | Yes | Yes |

| Bank Frick | Liechtenstein | Yes | No | Yes |

| Bankera | Lithuania | Yes | Yes | No |

| AMINA Bank | Switzerland | Yes | No | Yes |

| Solarisbank | Germany | Yes | Yes | Yes |

| Bank Syz | Switzerland | Yes | No | Yes |

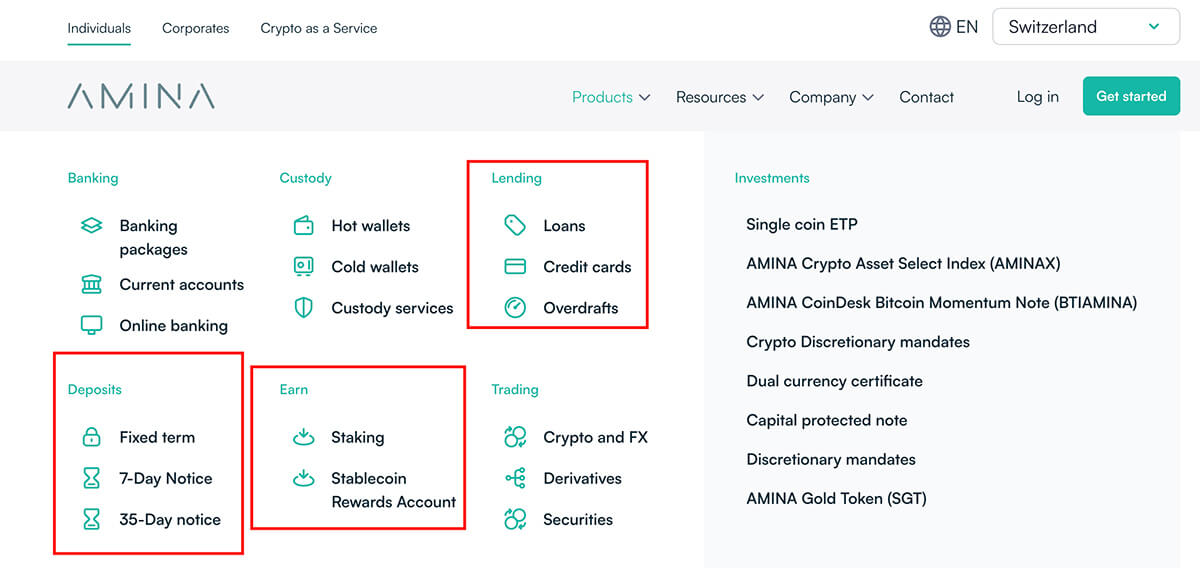

AMINA Bank (Switzerland)

AMINA Bank holds a full Swiss banking license from FINMA and is one of the most technically complete crypto banks in Europe. It offers institutional-grade services that span the full stack: deposits, staking, trading, lending, and overdraft — all within a regulated Swiss banking framework.

AMINA bridges traditional private banking and digital asset management for institutional and high-net-worth clients. For crypto businesses requiring Swiss regulatory standing and a full spectrum of financial services from a single institution, AMINA is the benchmark European option.

Wirex

Wirex is a fintech platform licensed in Europe and the UK, specifically designed for businesses operating at the intersection of fiat and digital assets. It provides multi-currency accounts (USD, EUR, GBP) alongside wallets for BTC, ETH, USDT, LTC, XRP, ADA, and others — eliminating the need for separate exchange and bank accounts.

Wirex's practical advantages for crypto businesses:

- SWIFT and SEPA support on classic accounts — direct fiat settlement for EU clients

- Currency exchange, transfers, and crypto buy/sell within a single platform

- Up to 2% cashback in cryptocurrency on Wirex card transactions

- Exploration of tokenized real-world asset (RWA) integrations for expanded investment access

Bankera (Lithuania)

Bankera operates under a license from the Central Bank of Lithuania and is one of Europe's most explicitly crypto-business-oriented banks. Importantly, Bankera itself does not hold cryptocurrency — it partners with SpectroCoin for on-ramp/off-ramp operations, where corporate account balances can be transferred and converted to BTC, ETH, or other assets.

This architecture — fiat banking + licensed crypto partner — is well-suited for EU businesses that need a compliant, auditable structure separating fiat treasury from crypto holdings.

Bank Frick (Liechtenstein)

Bank Frick is a private bank with a specific focus on digital asset institutional services. It provides secure custody for digital assets, with access for both individual and institutional clients — operating under Liechtenstein's Blockchain Act, one of the most comprehensive crypto regulatory frameworks in Europe.

Bank Frick is the right choice for investment funds and asset managers that need compliant digital asset custody with private banking capabilities.

Solarisbank (Germany)

Solarisbank operates as a Banking-as-a-Service (BaaS) provider — it does not serve retail clients directly, but enables fintech companies and crypto exchanges to embed banking products into their own platforms without requiring a banking license of their own.

For crypto exchanges, payment processors, and fintech products targeting the European market, Solarisbank provides a fully licensed, API-driven banking infrastructure layer. This is a builder-tier option, not an end-user bank.

Bank Syz (Switzerland)

Bank Syz is a Swiss private bank founded in 1996, serving high-net-worth individuals, families, and institutions with wealth management and private banking services. Its crypto exposure is primarily through digital asset custody and investment products — relevant for wealth preservation clients, not for operational crypto business accounts.

How to Choose a Crypto Friendly Bank: 6 Technical Criteria

Choosing a banking partner for a crypto business is an architectural decision. Here are the criteria that matter most, based on our integration experience.

1. Banking Services Scope

Evaluate what the bank can actually offer your business operationally:

- Which currencies can you hold and settle in?

- Does the bank provide overdraft facilities — and what are the terms?

- Can you open multi-currency accounts for segregating client funds from operational reserves?

AMINA Bank, for example, provides deposit, staking, trading, lending, and overdraft from a single Swiss-licensed account — a rare combination for institutional clients.

2. Fee Structure

Fee costs compound quickly at transaction volume. Key questions:

- Domestic transfer fees — flat or percentage?

- International transfer fee — SWIFT vs SEPA rate?

- Is there a hidden spread on currency conversion built into the "no fee" claim?

As a benchmark: Revolut's international USD transfer commission is 0.15% — well below traditional SWIFT rates of 0.5–1%.

3. Overdraft Policy

For businesses with volatile crypto revenue cycles, overdraft capability prevents operational gaps:

- Does the bank offer overdraft at all?

- What is the commission or interest rate?

Mercury Bank offers a zero-commission overdraft option — particularly valuable for early-stage startups managing bridge periods between fundraising rounds.

4. API and Integration Capability

This is the most frequently overlooked criterion. A bank without a documented API cannot serve as the settlement layer for a crypto payment processor, exchange, or non-custodial wallet. Verify:

- Is there a public REST API for transaction data retrieval?

- Does the API support webhook callbacks for real-time settlement notifications?

- What is the rate limit and SLA for API availability?

In our crypto processing builds, banking API limitations were the single most common reason for mid-project partner replacement.

5. AML/KYC Policy Transparency

The critical question most founders forget to ask: what happens when your own AML system flags and returns a transaction? Does the bank treat that as a suspicious activity report, or as normal compliance behavior?

6. Physical Branch and Reputation

For businesses managing significant capital volumes, physical branch access remains relevant — particularly for resolving account freezes quickly. Before choosing any bank, review its Trustpilot profile and Google Business reviews. Prioritize feedback from other crypto businesses specifically, not general retail customers.

Crypto Friendly Banks vs Crypto Exchanges: The Integration Layer

One of the most misunderstood aspects of crypto banking is the relationship between banks and exchanges. A crypto-friendly bank is not a crypto exchange — and the quality of the integration between the two determines your operational capability.

When a payment is initiated through a crypto processing system, the bank handles fiat settlement while the exchange executes the on-chain transaction. The synchronization between these two layers — including real-time status updates, reconciliation, and failure handling — is where most operational problems occur in production.

The AML check ran before funds touched either layer: high-risk transactions were returned at the blockchain monitoring stage, before they entered the processing queue. This architecture required the bank to have zero involvement in crypto-specific logic — but it also required the bank to have no policies that would flag high-volume crypto-adjacent fiat flows as suspicious. Finding a bank that met this requirement took longer than any technical integration.

Pros and Cons of Crypto Friendly Banks

Advantages

- Operational bridge between fiat and crypto: eliminating the friction of moving between multiple platforms for settlement, conversion, and custody.

- Regulatory cover: licensed crypto-friendly banks provide the compliance framework (AML, KYC, tax reporting) that standalone exchanges cannot offer as a primary banking partner.

- Business scalability: banks like AMINA, Solarisbank, and Anchorage offer institutional-grade services that scale with transaction volume and regulatory complexity.

- 24/7 crypto market access via mobile: neobanks like Revolut and Juno provide mobile-first platforms that match crypto's round-the-clock operating schedule.

Disadvantages

- Higher service fees: the compliance overhead of crypto banking is priced into fees — typically higher than a standard business account at a traditional bank.

- Regulatory exposure: if new legislation restricts or bans specific crypto activities in your jurisdiction, even a crypto-friendly bank will comply — which can mean account restrictions with limited notice.

- Limited DeFi compatibility: no regulated bank currently offers native DeFi protocol integrations — the off-ramp from decentralized finance to regulated banking remains a manual or semi-automated step.

Frequently Asked Questions

Which bank is best for a crypto startup in the US?

Mercury is the most common choice for early-stage US crypto startups due to its permissive policy toward Web3 entities, no minimum balance, and clean exchange transfer policy. Anchorage Digital is the option for institutional-scale operations requiring a federally chartered bank.

Can a non-resident open a crypto-friendly bank account in the US?

Yes — Mercury explicitly supports non-resident account opening and is one of the few US banks that do not require a US entity at the time of application. Most other US banks require either a Social Security Number or an EIN linked to a registered US entity.

What is the difference between a crypto-friendly bank and a crypto exchange?

A bank handles fiat settlement, regulatory compliance, SEPA/SWIFT transfers, and account infrastructure. An exchange handles on-chain transaction execution and crypto custody. In a production crypto processing system, both operate as separate layers. A "crypto-friendly bank" does not replace an exchange — it ensures the fiat layer does not block exchange integrations.

Do crypto-friendly banks require KYC?

Yes, without exception. All licensed banks — regardless of their crypto stance — operate under AML and KYC obligations. The difference between a crypto-friendly and a standard bank is not whether they perform KYC, but how they treat the output: a crypto-friendly bank does not automatically treat crypto-adjacent transactions as suspicious activity requiring manual review.

Which European bank is best for a crypto business under MiCA?

AMINA Bank (Switzerland, FINMA-licensed) and Bankera (Lithuania, Central Bank of Lithuania-licensed) are the strongest options under the post-MiCA European regulatory framework. AMINA is better for institutional clients; Bankera is more accessible for small and medium businesses needing a compliant EU fiat account with a crypto on/off-ramp partner.

What should I verify before opening a business crypto bank account?

Before signing: confirm the bank's written policy on exchange transfers (Binance, Kraken, Coinbase), request documentation on AML-returned transaction handling, verify whether the bank has a REST API for automated reconciliation, and check whether they require a local entity or accept non-residents. Failure to verify any of these in advance is the most common cause of mid-project banking partner replacement in crypto infrastructure projects.

Is Monzo crypto friendly?

Yes, with limitations. Monzo does not support buying, selling, or holding cryptocurrency directly on the platform. However, it allows transfers to licensed crypto exchanges (Binance, Coinbase, Kraken, Bitstamp) and does not block crypto-related fiat activity subject to standard AML/KYC checks. It is best used as a GBP operational account, not as a primary crypto banking solution.

What banks support crypto businesses in the UAE?

Emirates NBD, RAKBANK, and Mashreq Bank all support crypto-related business accounts in the UAE. For companies holding a VARA (Virtual Assets Regulatory Authority) license, Emirates NBD provides the strongest institutional infrastructure. RAKBANK is a more accessible entry point for smaller crypto entities entering the market.