Reducing the AI industry to a single figure is a failed undertaking from the start. Gartner has its own methodology, McKinsey has its own, Statista has a third, and sometimes the difference in estimates for the same market can reach threefold. This isn't because someone is wrong, but because the subject of research changes faster than definitions can be established. But amidst this chaos, it's still possible to identify a consistent core of figures—from Gartner, McKinsey, Stanford HAI, the WEF, and a dozen industry agencies—that doesn't depend on who issued the most sensational press release this week.

Key indicators for 2026:

- Total global spending on AI—infrastructure, enterprise software, and services—is approaching $2.5 trillion in 2026 (Gartner's revised May estimate).

- The AI software and services market itself, without the broad "everything in sight", is estimated at a much more modest $312 billion to $900 billion, depending on how you count it.

- The base market CAGR is 19–31% over the horizon up to 2033–2035, depending on the methodology.

- Generative AI is growing significantly faster than the mainstream market— 29–43% per year, according to MarketsandMarkets and related firms.

- 88% of companies worldwide use AI in at least one function: a year ago it was 78%, two years ago it was 55% (McKinsey).

- only 7% of companies have fully scaled AI across their entire organization . The rest are somewhere between pilot and partial implementation.

- 39% report a measurable effect on EBIT, while only 6% of companies actually earn more than 5% of EBIT from AI.

- 62% of organizations are experimenting with agent AI, but only 23% have scaled such systems.

- Investment in generative AI has grown nearly eightfold since ChatGPT's launch.

- The WEF predicts that by 2030, AI and related technologies will create 170 million jobs and destroy 92 million – a net gain of 78 million.

- 39% of key skills in the labor market will become obsolete or transformed by 2030.

- AI infrastructure is the fastest-growing segment of the market, with spending on it jumping nearly 49% year-over-year.

- North America holds 31–41% of the global market, depending on the calculation, with the Asia-Pacific region experiencing the fastest growth in adoption.

It's worth keeping these numbers in mind as a frame of reference—we'll explore where they come from and what's behind each one later.

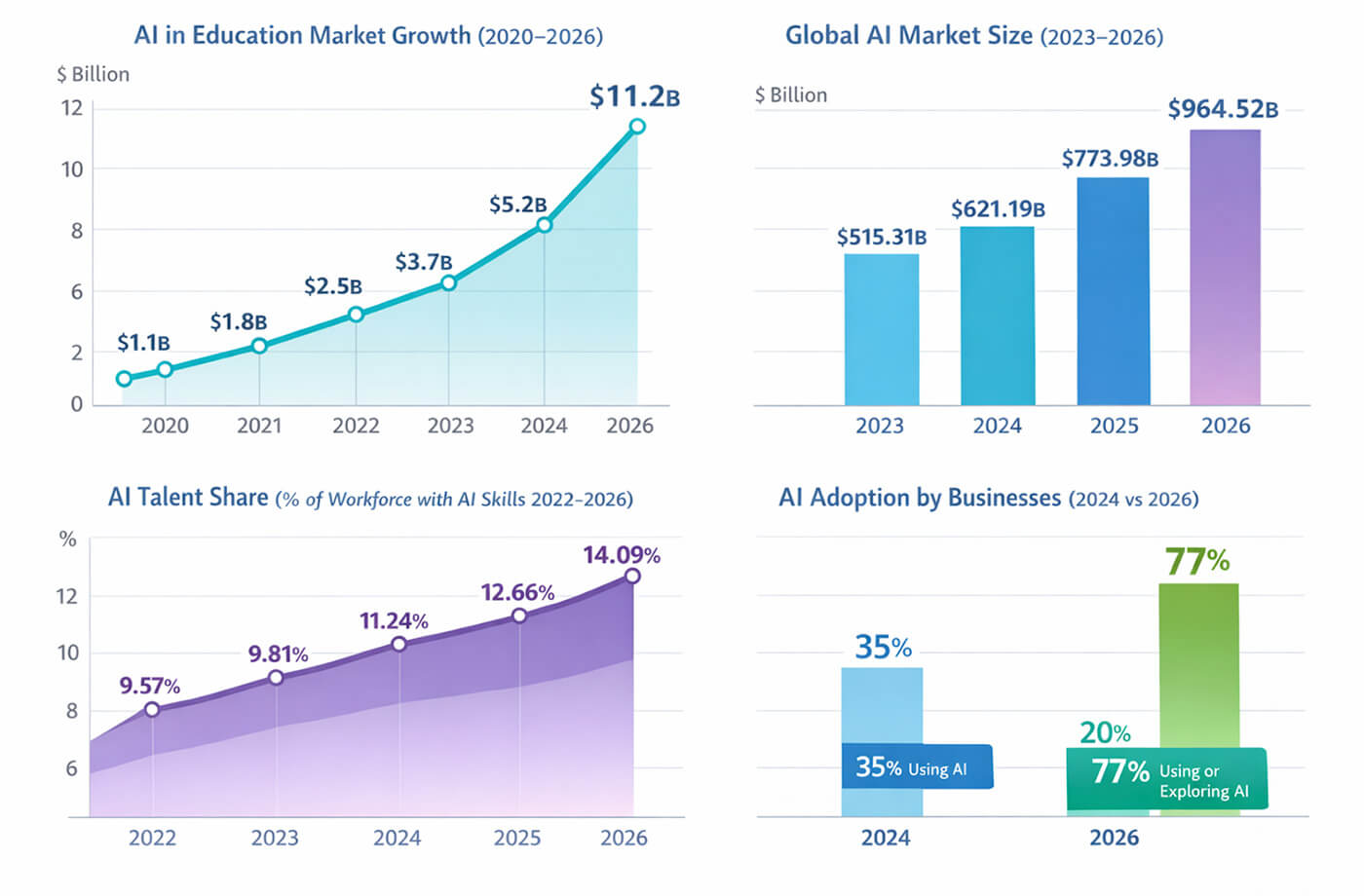

Market size and forecasts

The range of estimates for the global AI market size is not a sign of unreliable data, but a consequence of fundamentally different measurement boundaries.

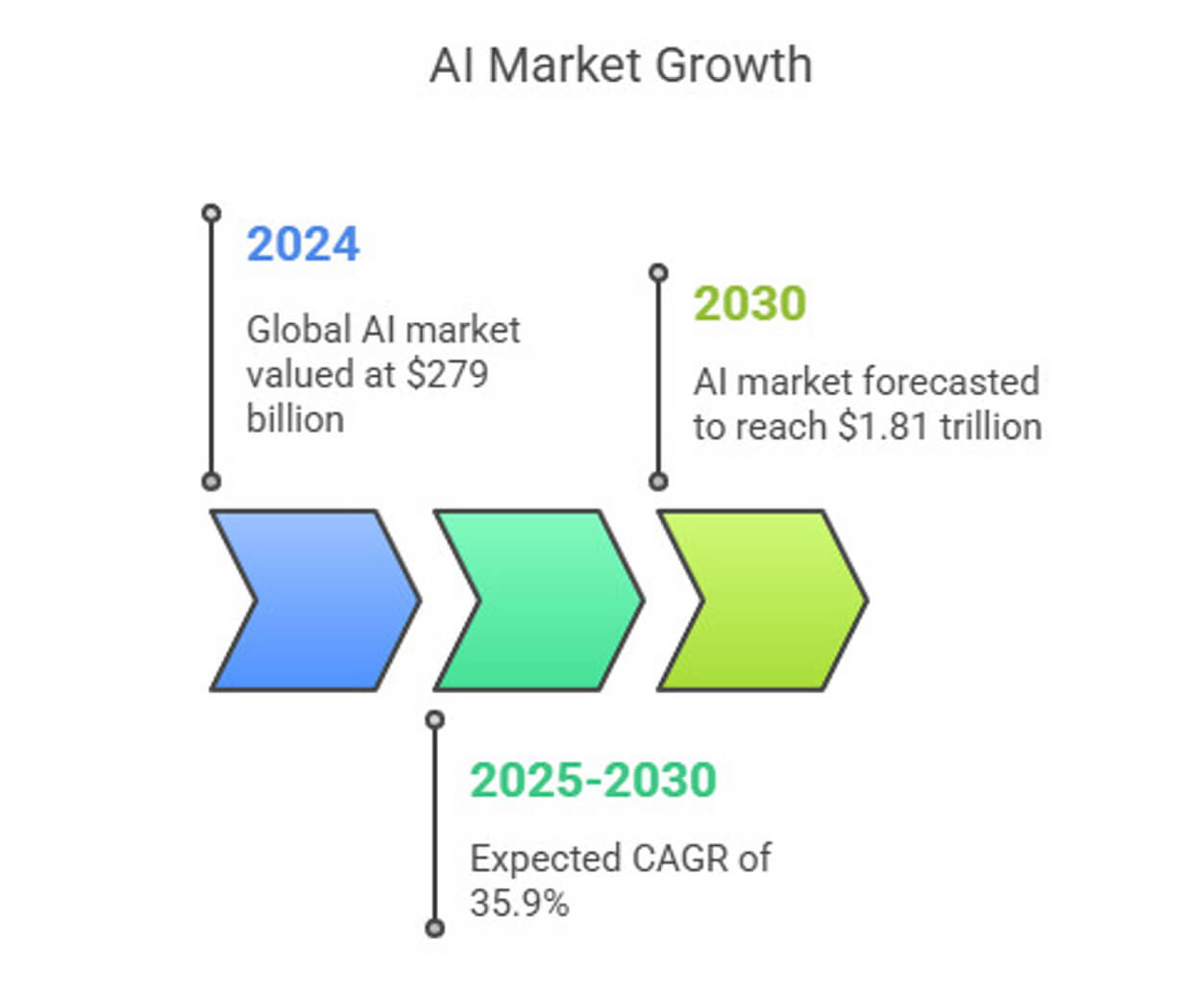

Take three reports in a row and you'll see three different worlds. Fortune Business Insights's scope includes software, services, and some hardware, totaling around $376 billion in 2026, expected to grow to $2.48 trillion by 2034 at a CAGR of 26.6%. MarketsandMarkets takes a broader view: they also include and develop server-side AI infrastructure, and the base almost doubles — $602 billion this year, and $3.64 trillion by 2033 at a CAGR of 29.3%.

Precedence Research's market definition is completely different from the previous two—broad, industry-specific, with no clear boundaries between "software" and "infrastructure"—and the resulting figure is $900 billion already, with a target of $4.2 trillion by 2035.

Statista is traditionally more conservative: around $312 billion in 2026, growing to $827 billion by 2030 at a CAGR of 27.7%. Meanwhile, total global IT spending on AI—a Gartner category that includes everything from data centers to corporate licensing—already exceeds $2.5 trillion, with no sign of slowing down.

Within this picture, generative AI is growing faster than all other fields—29–43% annually, compared to much more modest rates for machine learning, computer vision, and classical NLP. According to MarketsandMarkets, operational processes and logistics will become the largest functional application of AI in business by 2026.

Precedence Research is largely uncontroversial, but places another leader alongside it—the BFSI sector, banking, and finance, which, according to their calculations, accounts for an equally significant share of demand.

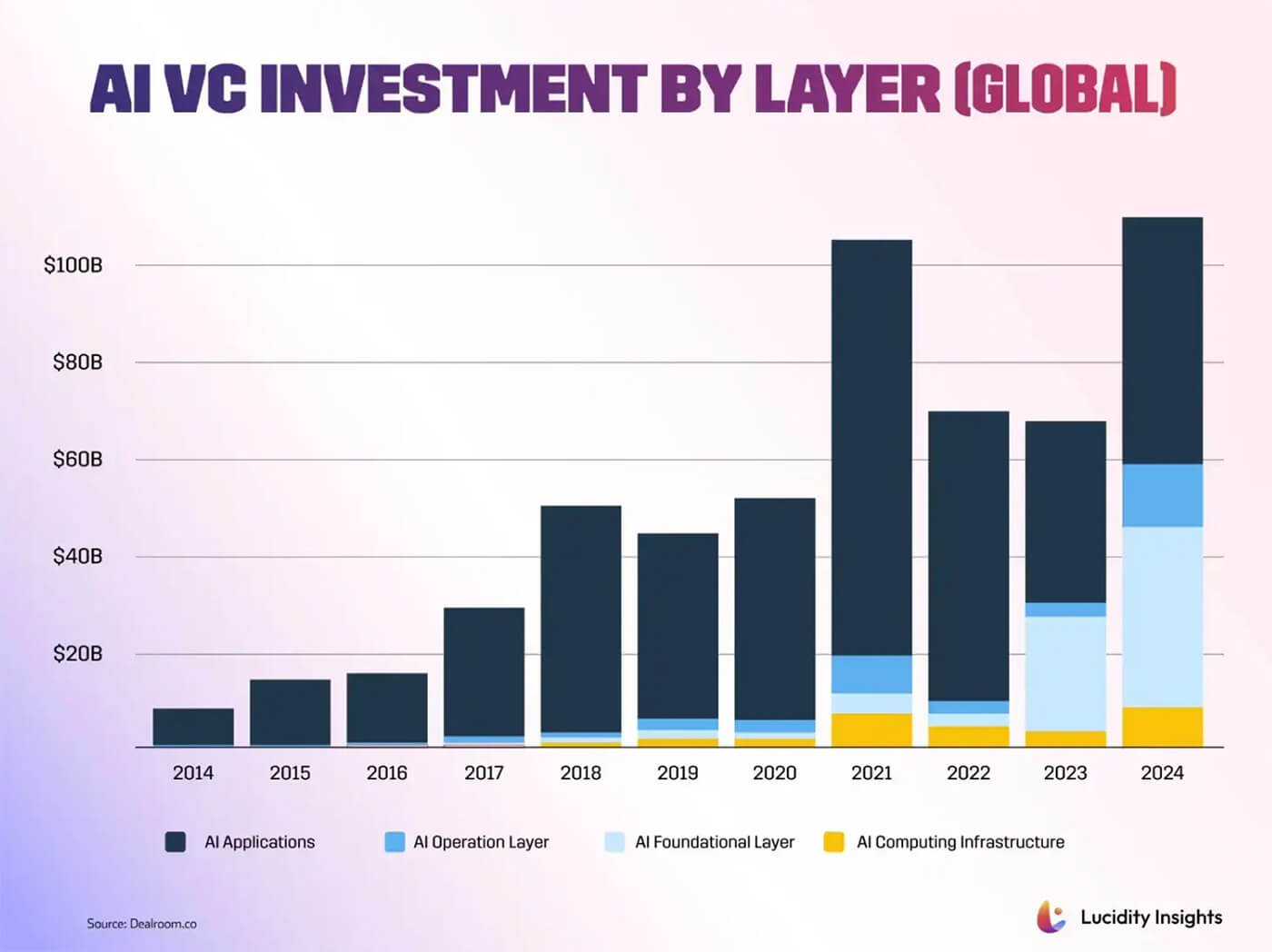

Investments and venture financing

Venture capital has long since ceased to regard AI as just another field — it has become almost synonymous with technology ventures as such.The share of mega-rounds (deals over $100 million) going to companies declaring AI as their core product continues to grow year over year, while the concentration of capital in the hands of a small group of leaders—laboratories like OpenAI, Anthropic, xAI, and a few infrastructure players—is increasing, leaving ever-decreasing space for mid-tier startups.

A curious development in 2026 is the formation of consortiums around open frontier models: NVIDIA, for example, announced an alliance with Mistral AI, Black Forest Labs, and Perplexity to jointly develop models on DGX Cloud infrastructure, reflecting a shift in the competitive logic—from isolated races to coalitions around a shared computing base. Such alliances are changing the structure of investment flows: capital is concentrated not only in the models themselves but also in the underlying infrastructure—chips, cloud platforms, and agent orchestration tools.

To be honest, most of the money the press calls "AI investments" actually ends up not in products or models, but in capital expenditures on computing power: GPU clusters, data centers, and IaaS for training and inference. This segment has grown by almost 49% year-over-year—faster than any other market segment. Understanding this nuance is important for anyone trying to assess where money is really flowing in the industry, rather than simply reading headlines about the latest mega-round.

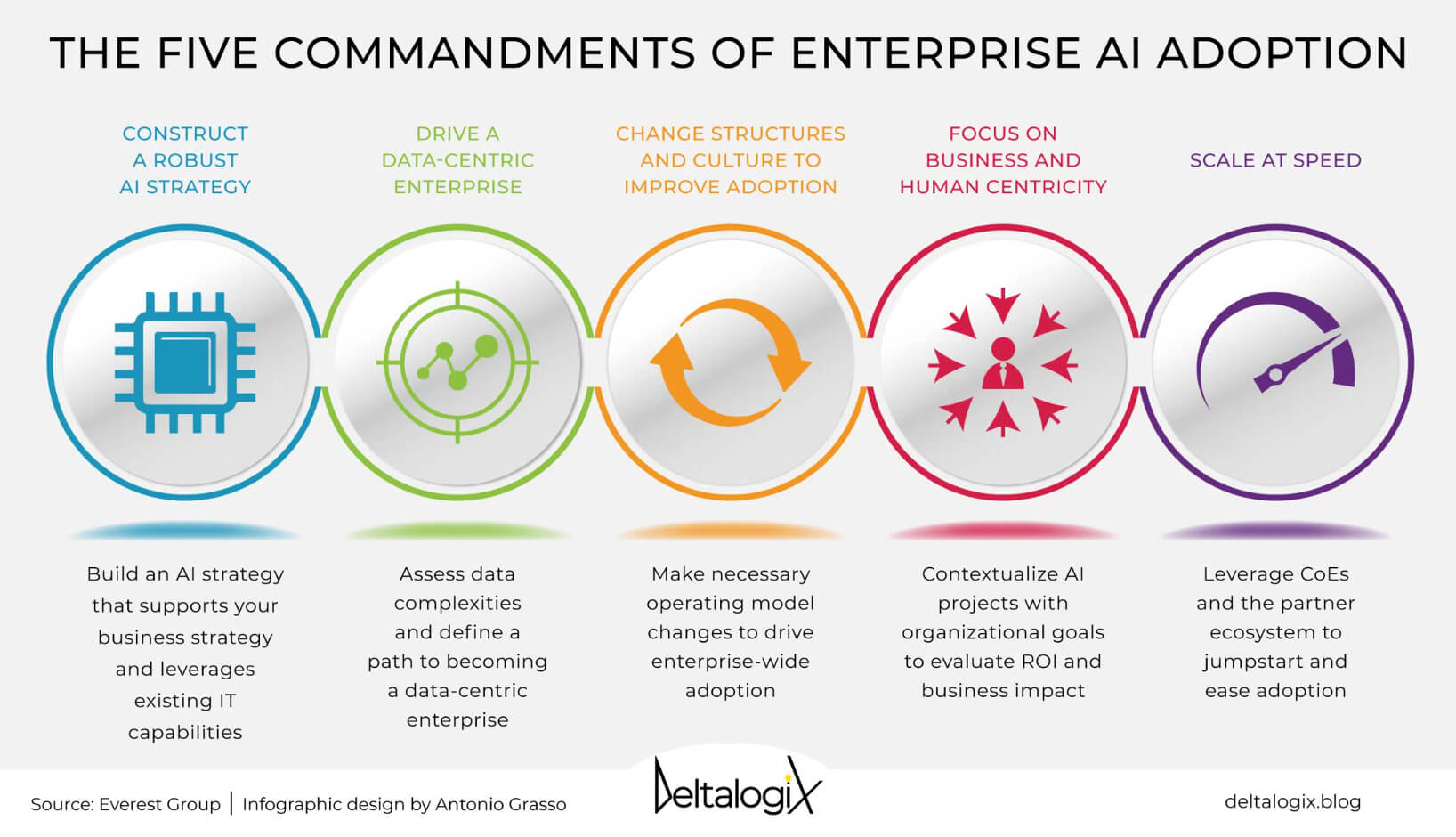

Implementing AI at the enterprise level

The main methodological benchmark here is McKinsey's annual survey, which covers nearly 2,000 respondents in 105 countries. Its latest wave recorded an increase in the share of companies using AI in at least one function to 88%—up from 78% the year before and 55% two years earlier. This figure is often cited as proof of "AI's victory", but a closer reading of the same report paints a less clear picture.

Two-thirds of organizations have yet to scale AI beyond pilots. About a third have fully deployed it enterprise-wide, but strictly speaking, without any elaboration on the definitions, only 7% have. The difference between large and small players is also striking: almost half of companies with revenues over $5 billion have reached the scaling stage, compared to only 29% of companies with revenues under $100 million.

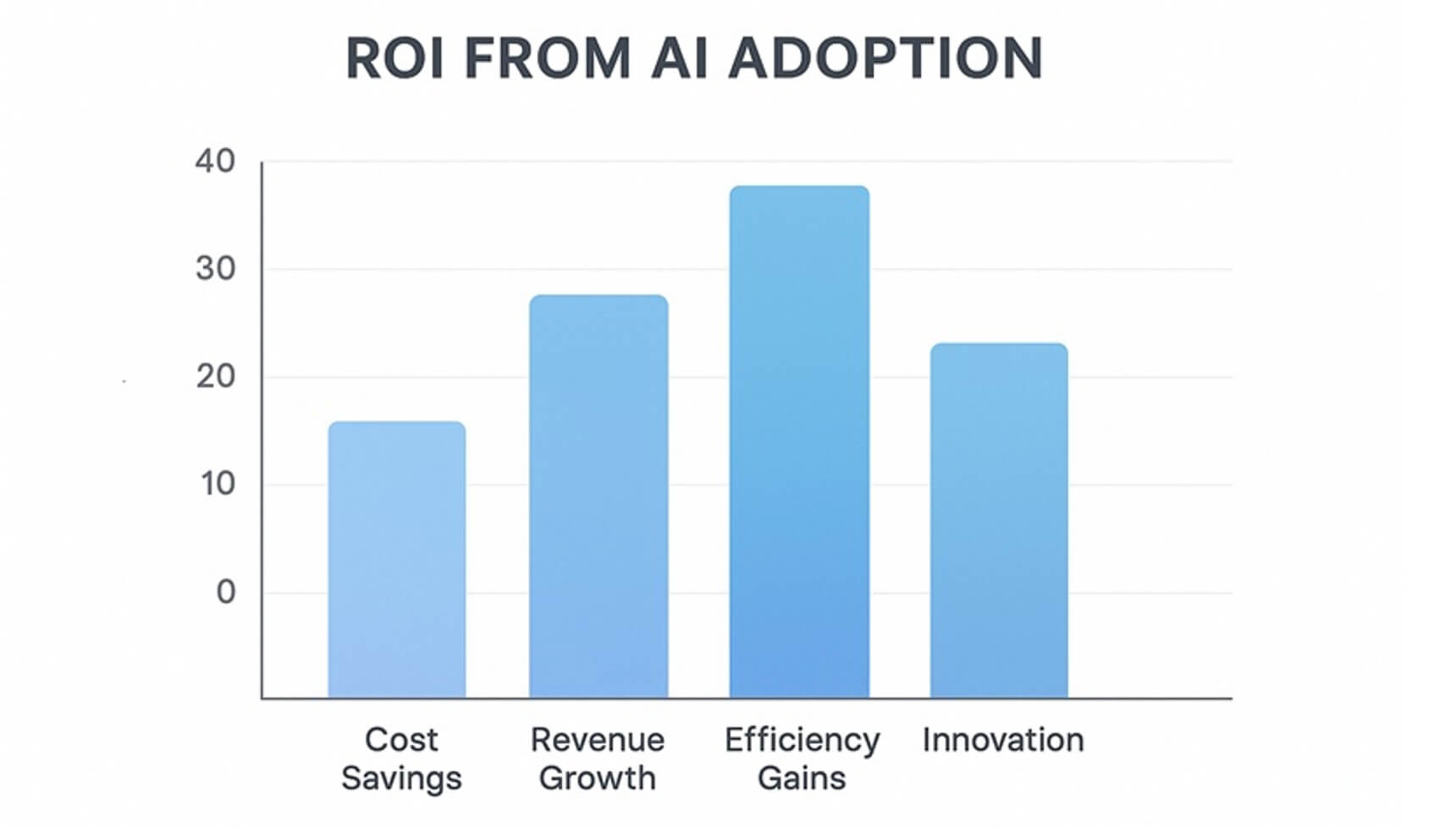

Money is a particular pain point. Thirty-nine percent of respondents report some impact of AI integration on EBIT, but generally less than 5%. Only 6% of companies fall into the category of true "high performers"—those whose AI contribution to EBIT exceeds 5% and whose integration is systemic, not cosmetic. Gartner confirms the gap from the other side: among mature companies, 45% keep AI projects running for more than three years, compared to only 20% of immature ones. Early adopters, on average, save 15.2% on costs and achieve a 22.6% productivity boost—meaning the benefits are real, they're just not shared.

Generative AI and large language models

The share of companies using generative models in at least one function increased from 33% in 2023 to 71% in 2024 and 79% in 2025. By comparison, the transition of companies to cloud services in the 2010s took many times longer—they took a decade, while the market here has completed the same journey in less than three years.This is explained not only by the quality of the models themselves, but also by the low barrier to entry: trying generative AI didn't require a separate IT infrastructure, a six-month budget cycle, or approval from dozens of stakeholders—all it took was a browser and a subscription.

This is precisely why the first wave of adoption was so rapid: employees began using the tools themselves before companies had time to establish official policies for their use. Organizations later caught up with this grassroots practice with formal regulations, licenses, and integration into corporate systems.

Generative AI has gained a foothold primarily in IT support—ticket automation, incident diagnostics, code writing and review—and in knowledge management: document search and synthesis, responding to internal queries, and summarizing large amounts of corporate information.

Marketing and sales are next—draft generation, content personalization, and proposal preparation—and product development, where models are increasingly used in prototyping and hypothesis testing.

Agent AI: From Hype to First Pilots

Agent systems—those that plan and execute multi-step tasks without constant human supervision—have become a major topic of conversation at the turn of 2025 and 2026 precisely because statistics on them are still scant, and everyone understands the risks are high.

62% of McKinsey's companies are at least experimenting with agents, but only 23% have actually reached scale—and these are mostly one or two features, not end-to-end integration. Google Cloud's research gives a similar figure: 52% of companies already use agents in some form, which is quite rapid for a technology that existed mainly on conference slides a year and a half ago.

The main risk analysts point to is that agent systems require a fundamentally different level of governance, access control, and decision auditing than traditional AI chatbots or copy-pilots—and most companies, by their own admission, are not yet infrastructurally ready for this.

Productivity, ROI, and implementation costs

There are positive indicators of AI's impact on business, but they are asymmetrical relative to expectations. Sixty-four percent of McKinsey respondents believe that AI fosters innovation within their organizations, and Google Cloud reports show that 74% of executives report a positive ROI within the first year of using AI tools. Moreover, early adopters with highly mature practices demonstrate an average 22.6% productivity gain and 15.2% operational cost savings—meaning the benefits are real, but not shared equally.

The key barrier to moving from pilot to production isn't the model itself, but the cost of AI integration: staff training, process redesign, data auditing, security, and regulatory compliance typically cost companies more than the AI service subscription itself or model development.

This is why companies that approach implementation as a process transformation project, rather than a tool purchase, are more likely to be among the top 6% of "high performers" — with a measurable contribution to EBIT.

The Labor Market: Displacement and Creation of New Roles

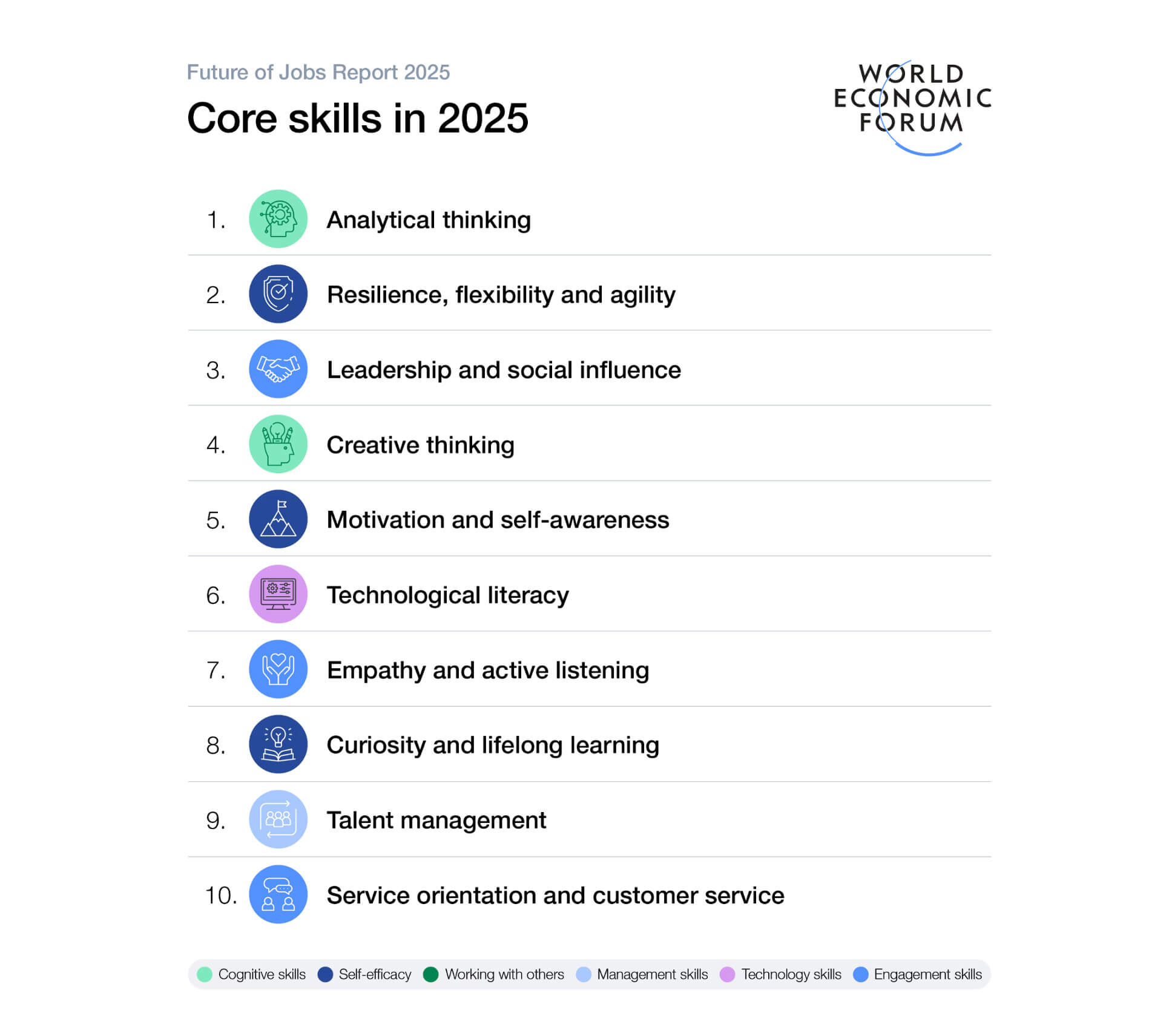

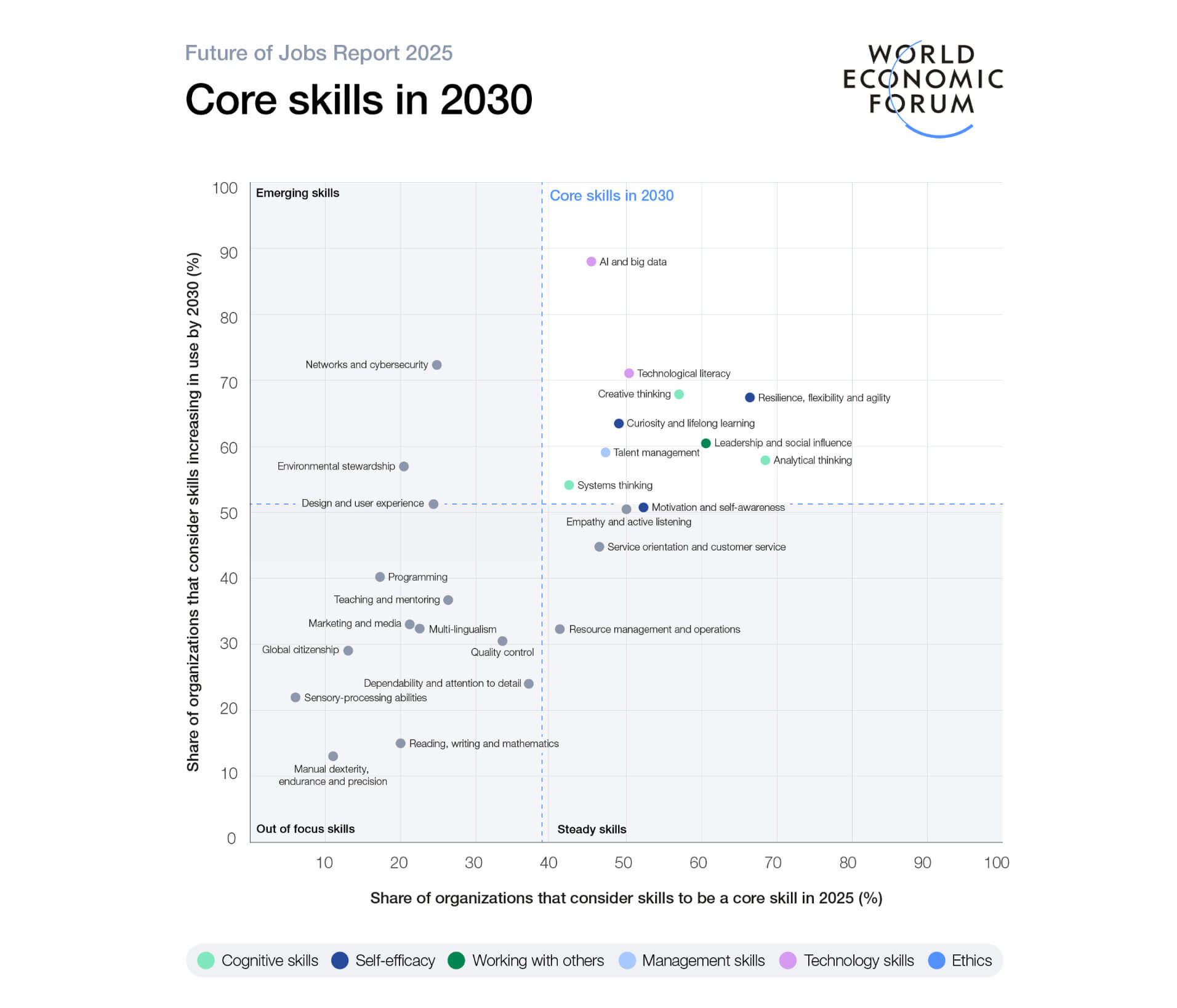

The primary source on this topic is the World Economic Forum's Future of Jobs Report 2025. Based on a survey of over 1,000 major employers across 22 industries and 55 countries, it's the source of the widely publicized figure: by 2030, technological advances will create 170 million new jobs and destroy 92 million existing ones. This represents 1.2 billion formal positions in the sample, and structural adjustments will affect 22% of them. Subtracting the lost jobs from the created ones yields a net gain of 78 million jobs.

86% of employers expect AI to transform their businesses by 2030. 39% of key skills will become obsolete or change significantly within five years—incidentally, this is lower than the 44% in the 2023 survey, and WEF analysts interpret this as a sign that companies have begun to more actively retrain people proactively rather than after the fact.

85% of employers cite retraining as a priority, while 63% complain about a shortage of necessary skills as the main barrier to transformation. Moreover, 41% of companies plan to reduce their workforce specifically due to automation—the growth of employment at the macro level does not negate the fact that changes at the level of specific professions will be painful.

Industry and regional breakdown

By industry, BFSI leads the way —banking, finance, and insurance account for 19-20% of all AI usage, according to Precedence Research. Healthcare is growing the fastest, at around 19% per year. However, the WEF expects a much more dramatic increase in automation in retail and wholesale consumer goods—up to 50% by 2030, while the forecast for financial services and capital markets is more modest, at around 40%.Geography is no less mixed. North America leads in almost every calculation method: in some places, it's 31.8% according to Fortune Business Insights, while in others, alternative estimates put it at 40%. This is easily explained—most of the capital and headquarters of large laboratories are located there. But if we look not at current share but at growth rate, the leader is different: the Asia-Pacific region is growing by about 47% year-on-year, driven by government digitalization programs and demand for automation in industry and finance.

Europe, by comparison, appears modest—according to Statista, its market will be worth approximately €42.6 billion in 2025, several times smaller than North America's. But it is growing steadily, largely due to the fact that the region's regulatory framework is finally consolidating into a unified system, rather than remaining a collection of disparate national regulations.

Risk management, governance and regulation

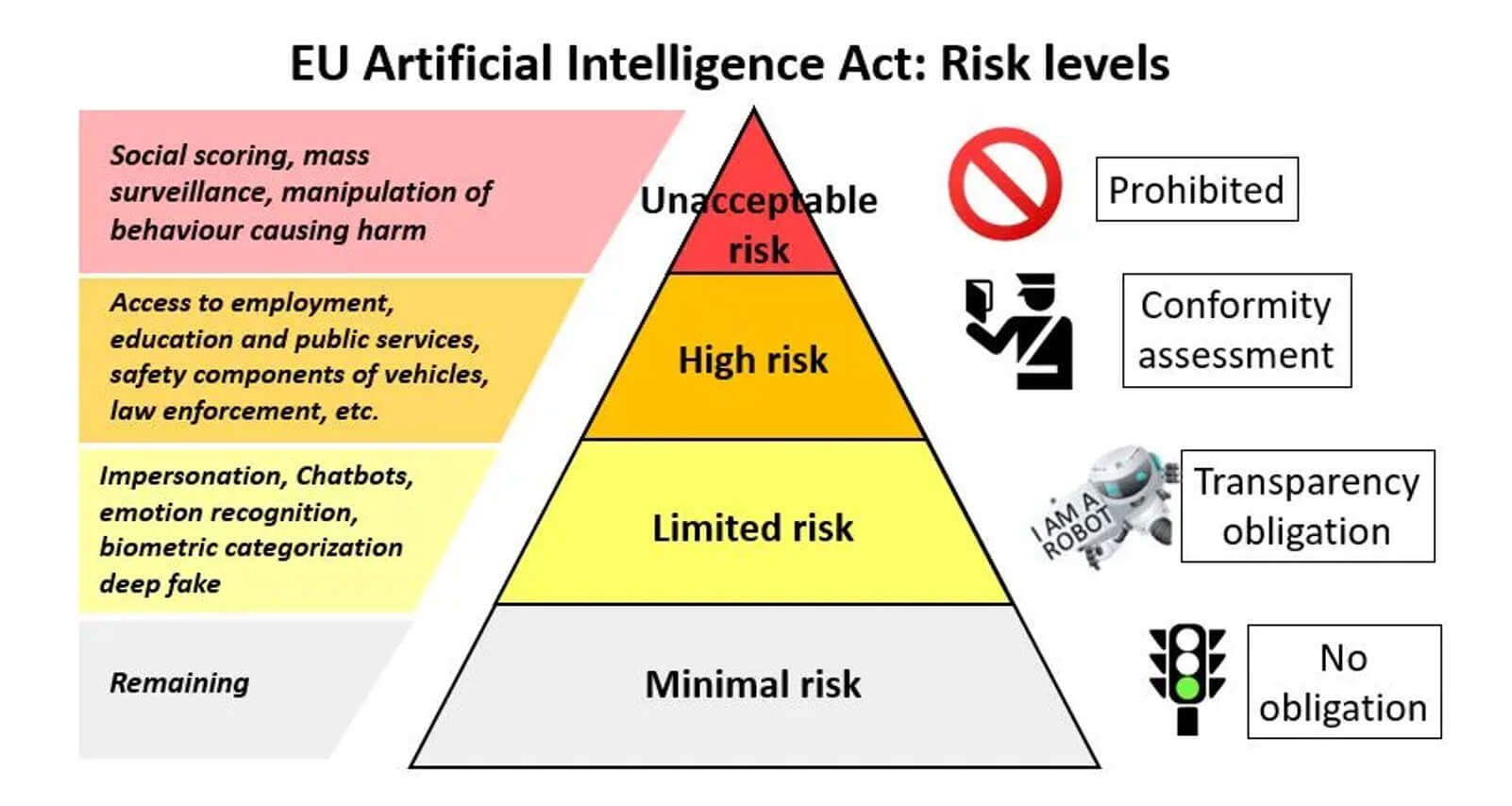

Regulatory pressure is growing alongside implementation—and this is entirely logical. The European AI Act is coming into effect in stages, with varying requirements depending on the level of risk: from virtually free use of low-risk systems to strict oversight of biometrics, scoring, and critical infrastructure. For businesses, this means one thing: internal AI governance policies need to be developed in advance, not only after the requirements become mandatory.

McKinsey found that almost half of companies cite ethical risks, privacy concerns, and a lack of expertise as the main barriers to AI adoption—a figure close to the 49% reported by other market surveys. What's telling is that among mature companies, the proportion that has formalized model auditing, bias control, and agent decision logging is significantly higher than among newcomers. Governance isn't an additional expense, but a prerequisite for truly scalable implementation rather than remaining stuck at the pilot stage.

A particularly alarming gap is between the speed of agent deployment (62% are already experimenting) and the maturity of practices for monitoring their actions, which is clearly lagging. Most companies do not yet have formalized audit protocols for what their AI agents do with real customer data or payments. Sooner or later, this will result in incidents—and will likely become the main regulatory issue of 2027.

Bottom Line: What Do These Numbers Say About the Real State of the Industry?

Putting all this together reveals a contradictory picture. On the one hand, the rate of AI penetration into business is truly unprecedented: 88% adoption in the four years since ChatGPT's launch is unparalleled in the history of corporate technology. On the other hand, the gap between "use" and "real value" is only widening: only 6% of companies are turning enterprise AI into a revenue driver, and two-thirds are still in the experimental phase without a clear scaling strategy.2026 isn't the end of the AI triumph story, but rather the moment when the market begins to separate the wheat from the chaff: companies capable of turning pilots into workflows from those simply following fashion. Data from primary sources is the best tool for making this distinction consciously, rather than relying on the latest headline.