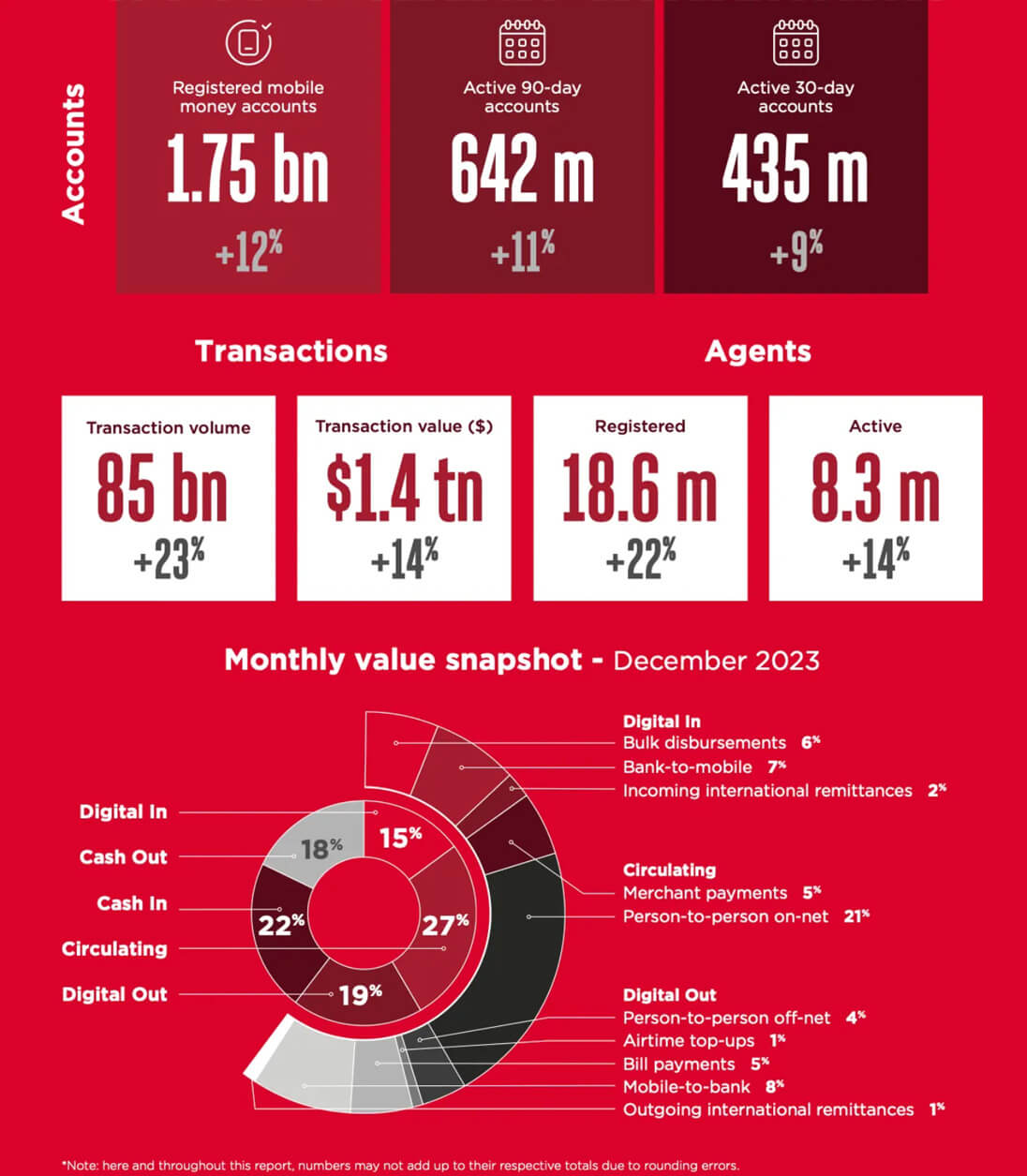

The global mobile banking market is no longer a growth story — it's infrastructure. By the end of 2023, 1.75 billion accounts were actively using mobile financial services, a 12% increase year-over-year. Online transaction volume crossed $1.4 trillion, up 14% from 2022. Android holds 67% of mobile banking users globally. The market is projected to grow at a CAGR reaching $7 billion by 2032.

These numbers define competitive pressure, not opportunity. If you're building a banking app in 2025, the question isn't whether users want mobile finance — it's whether your product meets the technical and compliance bar required to operate in this space. This guide focuses on exactly that: architecture decisions, security requirements, integration scope, and realistic development timelines based on projects we've shipped.

Types of Banking Apps: Define Your Product Before Writing a Single Line of Code

The term "banking app" covers fundamentally different products with different regulatory requirements, backend architectures, and go-to-market timelines. Conflating them is the first mistake teams make in scoping a project.

| Type | Core Function | Key Technical Requirement | Typical Timeline |

|---|---|---|---|

| P2P Payment App | Fund transfers between users (e.g., Venmo, PayPal model) | Payment gateway integration, real-time transaction processing, AML screening | 3–5 months (MVP) |

| Traditional Bank Mobile App | Frontend for existing bank core system | Core banking API integration, strict security layer, multi-account management | 4–8 months |

| Neobank / Virtual Bank | Full-stack digital bank without physical branches | Microservices architecture, KYC/AML pipeline, card issuing API, regulatory compliance | 6–12 months |

| Crypto Banking / Digital Wallet | Multi-chain wallet with fiat/crypto operations | Blockchain node integration, non-custodial key management, DEX connectivity | 3–6 months per platform |

| Crypto Payment Processor | B2B infrastructure for accepting crypto payments | Multi-blockchain support, liquidity pool management, partner API, AML module | 3–4 months (Enterprise) |

Knowing your product type determines technology stack, compliance scope, and — critically — what you can realistically deliver in a first release versus what belongs in version two.

Banking App Architecture: Monolith vs. Microservices

A monolithic codebase can launch faster, but creates a bottleneck the moment you need to scale transaction processing independently from user authentication or notification delivery. For financial products handling real money, this tradeoff is rarely worth the short-term development speed gain.

Microservices architecture — where each functional domain runs as an independent deployable service — is the production standard for fintech for a reason: it lets you update your AML logic, swap a payment gateway, or add a new blockchain without touching the core transaction engine.

In a crypto payment processing project we delivered for a European client, the microservices breakdown looked like this:

(1) Blockchain interaction layer — wallet address generation, balance monitoring, transaction status tracking across BTC, ETH, USDT ERC20/TRC20, Solana, BNB, Cardano;

(2) Payment provider service — operation initiation, status tracking, finalization, and financial reconciliation;

(3) Liquidity pool management — automatic and on-demand balance checks, swap execution against the pool when own funds are insufficient;

(4) AML / risk module — real-time screening of incoming transactions, automated return of high-risk operations without financial loss to the business;

(5) API gateway — external integration layer for exchanges (Binance, Kraken), bots, and partner systems;

(6) Admin and super-admin layers — separated permission systems, partner management, tariff configuration per project. Reliability baseline: duplicate server infrastructure in geographically separate regions, daily backups of all instances.

The AML module deserves particular attention. Teams routinely underestimate the complexity of ongoing automated counterparty checks versus one-time screening. These are architecturally different problems: one fires on every incoming transaction in real time; the other runs as a scheduled compliance process. Different data flows, different trigger mechanisms, different failure modes.

Core Features of a Banking App

Feature scope drives cost, timeline, and team size. Below is a realistic breakdown of what belongs in an initial release versus what can be deferred to subsequent iterations.

Must-Have: Release 1.0

| Module | Functionality |

|---|---|

| Account & Auth | Registration (email + password), Google 2FA, SMS OTP, login/logout, password recovery, session management |

| User Profile | Personal data management, KYC document upload, 2FA enable/disable, notification preferences, authorized IP history |

| Deposit | Payment gateway selection UI, data entry, API key-based gateway connection, confirmation flow |

| Withdrawal | Wallet address input, transfer confirmation form, gateway-specific min/max limits, commission calculation |

| Transaction History | Filterable by type (deposit/withdrawal), status, and time range; real-time status updates via webhooks |

| Balance Display | Real-time balance per account/wallet, demo and real account separation |

| Push Notifications | Transaction alerts, suspicious activity warnings, balance updates, promotional offers |

| Admin Panel | User list with KYC confirmation, withdrawal approval queue, transaction monitoring, dashboard with real-time KPIs |

Advanced Features for Version 2+

- Multi-account management — consolidated view across cards and accounts from a single dashboard;

- TradingView charts integration — for apps with investment or crypto functionality;

- Cardless ATM withdrawal — NFC and QR-based cash access without a physical card;

- AI-powered support — automated 24/7 response to common queries with escalation logic;

- Voice payment — contactless transaction confirmation via voice assistant;

- Smart device sync — transaction notifications and balance checks on wearables;

- Affiliate / referral program — with partner dashboard, FTD tracking, revenue share configuration, and campaign analytics;

- Perpetual futures / DEX trading — for crypto-native apps requiring advanced trading functionality with cross/isolated leverage, TP/SL orders, and order book.

Security Architecture: Non-Negotiable Requirements

Security in a banking app is not a feature layer — it's a foundational architecture decision. The threat model must be defined before UI/UX design begins: what data is stored, who has access at each role level, and what the breach surface looks like per endpoint.

Authentication Stack

Across the financial products we've shipped, the authentication implementation consistently includes: email and password registration with enforced complexity rules; Google Authenticator-based 2FA as the primary second factor; SMS OTP as a fallback channel; and session-level IP address whitelisting in the admin panel. Password recovery requires multi-step verification — single-channel recovery (email only) is insufficient for a regulated financial product.

KYC / Verification Flow

KYC is a regulatory requirement, not a UX feature. The implementation scope includes: document upload interface in the user profile (passport, government ID, proof of address); admin-side confirmation queue with approve/reject actions; account-level blocking and unblocking with audit trail; and authorized IP address history per user account. For products targeting US users, KYC requirements must align with FinCEN's Customer Identification Program (CIP) rules. Third-party KYC providers (Onfido, Sumsub, Veriff) can automate document verification — this reduces manual admin workload but adds a per-verification cost and an additional API integration to scope.

Admin Panel Security Layer

(1) Independent login with email, password, and mandatory 2FA via Google Authenticator;

(2) Role-based access control — granular permissions per administrator, editable without code changes;

(3) Administrator audit log — all actions attributable to a specific admin account;

(4) Withdrawal approval workflow — request queue with explicit confirm/reject actions, not automatic processing;

(5) IP whitelisting at the admin session level;

(6) New administrator creation with explicit permission assignment — no default full-access accounts.

This is the layer security auditors and regulators will review first in any compliance assessment.

Compliance Baseline for the US Market

If you're targeting US users, the minimum compliance checklist before launch includes: PCI DSS for any card data handling; FinCEN registration as a Money Services Business (MSB) if you're moving funds; Bank Secrecy Act (BSA) AML program with documented procedures; and state-level money transmitter licenses, which vary significantly across jurisdictions and can take months to obtain. None of these are development afterthoughts — they define what your data model, logging infrastructure, and audit trail must look like from the first sprint.

Payment Gateway Integration: Realistic Scope

Payment integration is not plug-and-play. Each gateway has its own API structure, webhook logic, error handling, and reconciliation requirements. Treating integration as a single task rather than a set of independent deliverables is how teams consistently underestimate backend effort.

In a trading platform with financial infrastructure we shipped, the gateway integration scope covered: deposit pages with gateway selection UI and API key configuration; withdrawal flows with wallet address input, confirmation forms, and transfer notifications; commission management per gateway with configurable min/max limits in the admin panel; transaction history filterable by type, status, and time range; and webhook/callback handling for real-time status updates on all operations.

For crypto-native applications, the scope expands significantly. Multi-chain wallet support (ERC20, TRC20, BEP20 at minimum) requires separate integration work per blockchain network. Network fee estimation, transaction confirmation depth thresholds, and liquidity pool connectivity are each independent technical deliverables.

(1) Deposit — selection UI, data entry form, API key mapping, confirmation callback;

(2) Withdrawal — wallet/account address input, min/max limits per currency, commission calculation, confirmation form, transfer notification;

(3) Webhook handling — real-time status updates for all operation states including failed transactions;

(4) Reconciliation — periodic financial cross-checks between platform records and gateway statements;

(5) Error handling — gateway-specific failure states and retry logic;

(6) Admin view — full transaction history per gateway with filter and export capability.

For multi-chain crypto products: each new blockchain (new chain, new token standard) added post-launch requires a separate scoping and development effort — it is not a configuration update.

Development Process: Parallel Workflows and Version Control Architecture

When a client has an existing financial product and needs a new module integrated — for example, adding perpetual futures trading to a non-custodial crypto wallet — the development process requires careful version control architecture. Pushing directly into the client's main repository is rarely viable: it creates merge conflicts with the client's own active development and compresses the review cycle into a single shared branch.

In a non-custodial wallet project built on TrustWalletCore, we integrated a full perpetual futures trading module — including markets list, order book, cross/isolated leverage mode, TP/SL orders, funding rate display, and full position management — using exactly this approach. The client's team continued shipping their own roadmap while our module was developed on a forked branch, with a structured pull request review process managed by their tech lead.

Async development on a forked repository requires process discipline to compensate for reduced visibility. The minimum viable communication structure for this model: weekly sprint reports with completed task list and blockers; bi-weekly demo calls with working functionality; clearly defined acceptance criteria per pull request before review begins.

Tech Stack Considerations

Stack selection in fintech is constrained by security requirements, platform targets, and the existing infrastructure you're integrating with. There's no universal answer — but there are common traps.

Mobile Layer

React Native and Flutter are the dominant cross-platform choices for banking apps targeting both iOS and Android. Both deliver near-native performance for standard financial app interactions. The exception: if your app integrates with device-level security APIs (biometric authentication, Secure Enclave on iOS, Android Keystore), native mobile banking app development (Swift / Kotlin) gives you more direct control and fewer abstraction-layer issues. For non-custodial crypto wallets specifically, TrustWalletCore is the established library for cross-platform key management — it handles wallet generation, signing, and chain-specific transaction formatting across 60+ blockchains.

Backend Layer

Node.js and Go are the common choices for high-throughput transaction services. PostgreSQL handles relational financial data; Redis handles session state and real-time balance caching. For event-driven architectures — critical when you need real-time transaction status propagation across services — Kafka or RabbitMQ handles the message bus. WebSocket connections (or Pusher for managed delivery) cover real-time UI updates for transaction confirmations and balance changes.

Charts

TradingView's charting library is the production standard for financial apps requiring candlestick charts, order book visualization, and technical indicators. It integrates via JavaScript embed for web and via WebView wrapper for mobile. Standalone advanced charts require a separate commercial licensing agreement — factor this into your cost estimates from the start.

How Much Does It Cost to Build a Banking App

Development cost is a function of feature scope, team location, and platform targets. The ranges below reflect realistic market rates for a professional development team:

| Scope | Description | Estimated Cost | Timeline |

|---|---|---|---|

| MVP / Basic | Single platform (iOS or Android), core auth, one payment gateway, basic transaction history, admin panel | $40,000 – $60,000 | 2–3 months |

| Mid-tier | iOS + Android, multiple payment gateways, KYC flow, push notifications, TradingView charts, full admin panel | $60,000 – $100,000 | 3–5 months |

| Enterprise / Full-stack | Microservices architecture, multi-blockchain support, AML module, liquidity pool, partner API, super-admin, compliance infrastructure | $100,000 – $200,000+ | 4–8 months |

| White-label deployment | Existing validated platform rebranded and reconfigured: new logo, color system, gateway API keys, domain connection | $5,000 – $15,000 | 1–2 weeks |

(1) Compliance infrastructure — KYC pipeline, AML module, audit logging, and regulatory reporting add 20–30% to backend scope;

(2) Multi-blockchain support — each additional chain beyond the BTC/ETH/USDT baseline is a separate integration effort;

(3) Server reliability infrastructure — duplicate servers in geographically separate regions, daily backups, and failover routing are required for a production financial product;

(4) Payment gateway reconciliation — automated financial cross-checks between your platform and each gateway require dedicated backend logic;

(5) Admin panel depth — a production admin panel with full user management, KYC confirmation, role-based access control, and withdrawal approval workflow typically represents 25–35% of total backend development effort.

Any quote that excludes these categories is incomplete.

Development Roadmap: From Concept to Launch

| Phase | Deliverables | Duration |

|---|---|---|

| Discovery & Architecture | Requirements specification, service boundary definition, tech stack selection, compliance checklist, API contract documentation | 2–3 weeks |

| UI/UX Design | Wireframes, UI design system, user flow prototypes, admin panel mockups, client design review | 3–4 weeks |

| Backend Core | Authentication service, user/KYC module, transaction engine, first payment gateway integration, admin panel API | 6–10 weeks |

| Mobile Development | iOS and Android apps, gateway UI flows, notification system, real-time balance updates, TradingView integration (if in scope) | 6–10 weeks |

| QA & Security Audit | Penetration testing, load testing on transaction flows, KYC workflow verification, admin permission audit | 2–3 weeks |

| Launch & Warranty | Production deployment, server infrastructure setup (primary + failover), monitoring configuration, 30-day warranty period | 1–2 weeks + 30 days |

FAQ

How long does it take to build a banking app?

An MVP with core functionality (auth, one payment gateway, basic admin panel) takes 2–3 months. A full-featured product with microservices architecture, multi-gateway support, KYC pipeline, and AML module typically requires 4–8 months depending on scope. White-label deployments of existing validated platforms can be delivered in 1–2 weeks.

What's the difference between a neobank app and a crypto wallet app?

A neobank operates in the traditional financial system — it requires a banking license or partnership with a licensed bank, handles fiat currency, and must comply with BSA/AML regulations and state money transmitter licenses. A crypto wallet app manages blockchain-based assets; non-custodial models don't hold user funds and have a different regulatory profile. That said, the technical complexity of a production crypto wallet — especially with multi-chain support, DEX connectivity, and perpetual trading — is comparable to or exceeds that of a neobank MVP.

Do I need microservices architecture from day one?

For an MVP with a single payment gateway and limited initial user base, a modular monolith ships faster and is manageable. The architectural inflection point comes when you need to scale transaction processing independently from other services, or when updating your AML logic requires deploying the entire application. If those scenarios are 12+ months away, a well-structured monolith with defined domain boundaries is a valid starting point — provided you plan the eventual service extraction from day one.

What compliance requirements apply to banking apps in the US?

The minimum compliance stack for a US-facing financial app: FinCEN registration as a Money Services Business if you're transmitting funds; a BSA-compliant AML program with documented customer identification procedures; PCI DSS compliance for any card data in scope; and state-level money transmitter licenses — which vary significantly between states and can take months to obtain. None of these can be retrofitted post-launch without significant rearchitecting of your data model and logging infrastructure.

Can an existing platform be rebranded and redeployed for a new client?

Yes — white-label deployment of a validated platform is a viable approach for trading platforms, crypto payment processors, and similar products where core functionality is already built and tested. The scope covers: UI/UX adaptation (logo, color system, brand styling), payment gateway key reconfiguration (new API keys for the client's accounts), domain connection, and redeployment to a new server environment. Delivery time is 1–2 weeks, contingent on the client providing gateway credentials and domain access promptly.

How is KYC implemented in a banking app?

KYC is implemented as a dedicated module within the user profile: document upload interface (government ID, passport, proof of address), admin-side confirmation queue with approve/reject actions, account-level blocking capability with audit trail, and authorized IP address history per account. For US products, CIP requirements under the BSA define the minimum data you must collect and verify. Third-party KYC providers (Onfido, Sumsub, Veriff) can automate document verification — this reduces manual admin workload but adds a per-verification cost and an API integration to scope.

What does a banking app admin panel need to include?

A production admin panel requires: user management with KYC confirmation, balance visibility, deposit/withdrawal history, and account block/unblock capability; withdrawal approval queue with explicit confirm/reject workflow; transaction monitoring across all operations; role-based access control with granular per-admin permissions; dashboard with real-time KPIs (total users, transaction volume, commission turnover); and trading pair / market configuration for apps with trading functionality. Admin authentication must use 2FA independent from user-facing auth.