A white label investment platform is a pre-built software solution that a financial institution, fintech startup, or wealth management firm licenses and brands as its own — instead of building the technology from scratch. In 2026, that definition covers a lot of ground: from a simple branded execution interface to a full-stack ecosystem with a matching engine, CRM, KYC/AML compliance tooling, robo-advisor, and mobile apps bundled into a single deployable system.

The opportunity is clear. In contrast to a standard investment platform, a White Label approach works equally well with venture capital funds, business angels, and individual retail investors — simplifying deal signing, investor onboarding, and the full transaction lifecycle. Even an investor with no technical background can assess project data, manage payments, and track returns through a well-designed dashboard. That accessibility is exactly what drives adoption.

What Type of Investment Platform Are You Building?

Before evaluating white label solutions, you need clarity on the platform category. The technology requirements, regulatory obligations, and vendor landscape differ significantly across types.Execution-only investing platform: users invest in stocks, ETFs, and funds through a self-directed interface. No personalized advice is provided. The simplest US regulatory path: route trades through a registered broker-dealer API (Alpaca, DriveWealth, Interactive Brokers) to avoid direct FINRA registration. Examples: Robinhood, eToro's stock investing feature.

Robo-advisor / automated portfolio management: AI-driven portfolio construction based on user risk profile and investment horizon. Includes automatic rebalancing and tax-loss harvesting. US regulatory requirement: Registered Investment Advisor (RIA) registration. Examples: Betterment, Wealthfront.

Wealth management platform: discretionary or advisory management for high-net-worth clients. Requires full compliance infrastructure, suitability documentation, and custody arrangements with a regulated custodian.

Alternative investment platform: crowdfunding, P2P lending, real estate tokenization, venture funding. Each has its own SEC framework — Regulation CF, Regulation D, Regulation A+. The most complex compliance path, but the largest gap in available white-label solutions.

How a White Label Investment Platform Works

How investment platforms work and their core advantagesThe business challenges of a startup investment platform are solved with out-of-the-box and customizable features including:

- signing deals and trading transactions;

- verifying the investor's qualifications and solvency;

- marketing campaigns and transaction processing;

- document management, commissions and report generation.

Most white label platforms are peer-to-peer: investors directly fund startups or trade assets, with the platform acting as a secure intermediary. Low transaction costs ensure competitive returns. Off-the-shelf protocols can be modified and customized per your requirements.

Recognizability and reliability as the basis for investor attraction

Having your own investment platform raises any startup to a new level by increasing its recognizability. The availability and flexibility of white label platforms guarantees connection to existing websites, portals, and back offices handling assets, liabilities, and trading operations. Customization takes place during development, scaled to the growth stage.

Investment platforms differ from crowdfunding platforms by individual decision logic. In a venture project with higher risk profiles, the return rates and minimum investment thresholds are configured differently than in a retail savings product. Customizing reward tiers to development stage and investor type is standard practice — not an advanced feature.

To attract savings from individuals, the platform needs to demonstrate reliability compared to a standard bank deposit: growth charts, profit calculators, and transparent fee structures are the primary trust-building tools.

Secure accounts with reporting capabilities

Integration with an existing client base and real-time mobile applications are standard requirements. A secure investor account with two-factor authentication, AML and KYC verification, and a personal dashboard for each profile enables both registration and ongoing reporting. Dynamic updating of reports and PDF generation via depository integration increases investor confidence across all experience levels.

White Label vs Custom Development vs Build From Scratch

Most organizations considering a white label investment platform face the same core decision: rent, build on a proven base, or build entirely from scratch.| SaaS White Label | Custom White Label (Development) | Build From Scratch | |

|---|---|---|---|

| Time to launch | 2–6 weeks | 6–16 weeks | 8–24 months |

| Setup cost | $15K–$50K | $40K–$180K | $200K–$800K |

| Monthly cost | $2K–$15K/month license | Infrastructure only | Infrastructure only |

| Ownership | Rented — vendor controls roadmap | Full code ownership | Full ownership |

| Customization | Constrained by vendor | High — any feature buildable | Unlimited |

| Compliance tooling | Included (generic) | Built to your jurisdiction | Custom build |

| Vendor dependency | High — pricing can change | None after delivery | None |

| Best for | Fast market validation | Specific requirements, long-term independence | Novel protocol needs |

The aspect that stands ahead is savings. Creating the investment platform at the start of a crypto business is an opportunity to save money — the difference between creating from scratch and using a white label base is significant. It is easier to use a well thought-out and thoroughly tested platform with the ability to customize the panel of functions, especially since at the start of the project the budget is rarely extra hundreds of thousands of USD.

We've worked with clients who wanted to switch from their SaaS provider after 18 months of growth and discovered their user data was stored in a proprietary format that required significant engineering work to migrate. The exit terms of a SaaS contract deserve the same scrutiny as the onboarding features. Technical support of white label platform creators is valuable for new startups — but dependency on that support creates risk when business scale or requirements diverge from what the vendor anticipated.

Core Features: Platform Capabilities by Tier

| Feature | Basic Platform | Advanced Platform | Institutional |

|---|---|---|---|

| Account types | Individual brokerage | + Joint, IRA, Roth IRA | + Corporate, trust, custodial |

| KYC / AML | Email + ID + selfie verification | + Accredited investor verification | + Enhanced due diligence, FATCA/CRS |

| Asset types | US stocks + ETFs | + Options, mutual funds, crypto | + Alternatives, private equity, bonds |

| Portfolio view | Holdings + P&L | + Performance attribution, benchmarks | + Factor analytics, risk metrics, drawdown |

| Robo-advisor | Risk profile questionnaire | + Auto-rebalancing, tax-loss harvesting | + Custom allocation models, glide paths |

| Copy trading | No | Follow top performers | + Strategy API, risk-adjusted copying |

| Real-time data | Level 1 quotes (last price, bid/ask) | + Level 2 order book, earnings calendar | + Options chain, alternative data feeds |

| Notifications | Push price alerts | + Earnings, news, analyst changes | + Custom trigger-based signal alerts |

| Reporting | Basic portfolio summary | + Tax reporting (1099-B prep) | + Regulatory reporting, GIPS compliance |

| Mobile app | Responsive web | Native iOS + Android | Native apps + advisor desktop portal |

| API access | None | REST API for account data | + FIX protocol, WebSocket streaming |

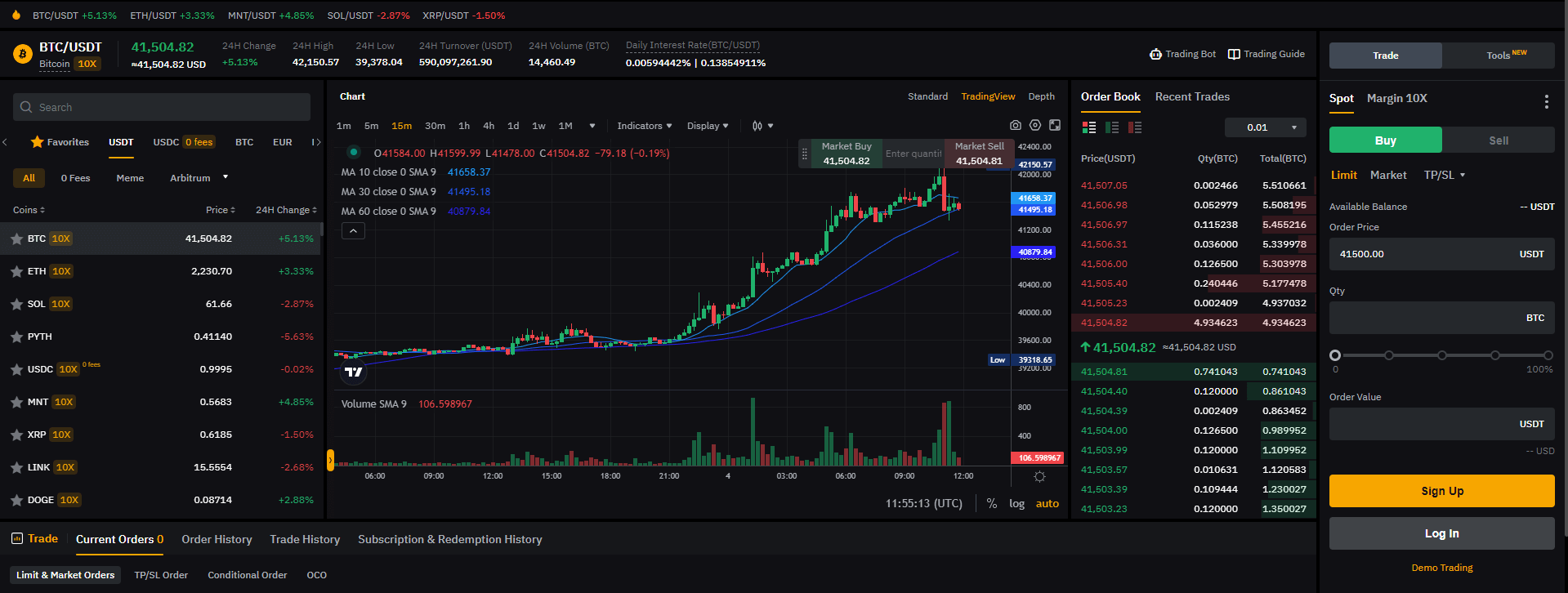

Multi-market solutions and spot/margin trading: platforms that provide the ability to trade commodities, assets, stocks, and futures work well across financial markets. Spot trading is suitable for all investor profiles; margin trading is selected by more experienced participants who evaluate the possibility of rising or falling asset rates. The ability to copy algorithms and traders' strategies — or create custom solutions based on them — adds significant retention value. Customizing access to spot and margin depending on account tier and KYC level is a standard configuration for white label crypto exchange protocols.

Robo-advisor and automated portfolio management: for platforms targeting retail investors, a built-in robo-advisor module presents the most compelling acquisition narrative. The investor sets a target return profile, risk level, and investment period. The system then presents allocation scenarios matching those parameters — from conservative fixed-income-heavy portfolios to aggressive growth-focused allocations. If the client is prepared to take higher risk, venture-stage and growth-oriented options are surfaced accordingly. This is meaningfully different from manual portfolio construction: the advisor layer guides undecided investors toward a decision, which directly improves conversion from onboarded user to funded account.

Unification, Customization and White Label Support

Individual brand design on a white label platform includes not only a logo, colors, and customized domain, but also digitally signed documents on letterhead and direct investor-to-investor interaction features. The client portal is designed for individuals who have decided to invest their savings. Custom templates and CRM integration unifies client data.API protocol enables integration of multiple services with minimal friction. White label's standard software includes risk management tools, bar charts and graphs, alerts, and built-in systems to monitor assets and trading volumes. Secure payment protocols using two-factor authentication and blockchain-grade encryption handle the security of registration and execution of electronic trading operations.

The WL model is popular among brokers and cryptocurrency market participants. Branding customization — color scheme, logo, visualization, buttons — increases company recognition. Professionally developed software that works without glitches or failures reinforces the brand credibility that new platforms need to establish trust.

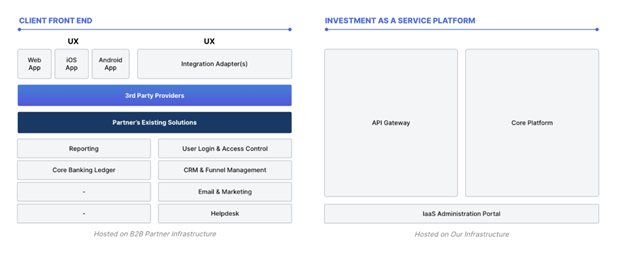

Technology Architecture: What's Under the Hood

A white label investment platform isn't a website with a "buy" button and a portfolio table. Behind the interface, a production platform includes: a real-time market data layer, a portfolio accounting engine, a risk profiling module, a rebalancing engine for robo-advisor configurations, an order execution layer with broker-dealer API integration, a KYC/AML compliance module, and a reporting engine for tax and regulatory purposes.

The back-end of a quality white label platform is arranged so that the user can:

- customize the investment terms and allocation parameters;

- choose the level of risk and investment horizon;

- select discretionary or advisory portfolio management mode;

- view the full activity log;

- reconcile assets and transactions in real time.

Advanced platforms support analysis of investment results by:

- estimating a company's capitalization and growth trajectory;

- yield calculation with dividend and split refinement;

- comparison against benchmark or index performance;

- risk-adjusted returns using Sharpe, Sortino, Omega, and Calmar ratios;

- dividend payment history, drawdown, and volatility charts.

When a price update arrives, it publishes to a channel; all subscribed clients receive the update in parallel without sequential bottlenecks. Portfolio accounting precision is another underestimated requirement: investment platforms handle fractional shares, corporate actions (splits, dividends, spin-offs), lot-level cost basis tracking (FIFO, LIFO, specific identification), and multi-currency positions.

A rounding error in cost basis calculation results in incorrect tax reporting — which is both a compliance problem and a trust problem with users. In financial platforms we've built, we implement automated daily reconciliation as a core system requirement: verifying that the sum of all individual user positions matches the total position held at the custodian. Any discrepancy triggers an alert before it compounds into a larger reconciliation problem.

Security architecture: to increase the security of communication channels, advanced platforms use cryptographic key exchange with constant or automatic rotation. Asymmetric cryptography is standard — one key encrypts and the other decrypts, using well-established cryptographic standards. Secure payment protocols, two-factor authentication, and blockchain-verifiable transaction records are baseline requirements for any platform handling real investor funds.

A service token in a blockchain network ensures that nodes can synchronize transactions independently, captured by distributed recorders. This is a significant advantage for transaction openness and auditability. The presence of a service token is used for blockchain-verified reporting and shareholder voting functions.

US Compliance: What Your Platform Needs

For investment platforms targeting US users, compliance requirements depend on the services provided — not just on whether you handle money.Execution-only platforms routing through a broker-dealer API (Alpaca, DriveWealth, Interactive Brokers): the broker-dealer partner handles FINRA registration, clearing, and custody. Your platform is a front-end with an API connection. You're still responsible for KYC verification for account opening and AML monitoring for suspicious transactions.

Registered Investment Advisors (RIA): platforms that provide investment advice, portfolio recommendations, or automated rebalancing must register as RIAs. Under $100M AUM: state-level registration. Over $100M: SEC registration. RIA platforms are subject to fiduciary duty — meaning every recommendation must demonstrably serve the client's best interest, not the platform's revenue.

Alternative investment platforms (crowdfunding, P2P lending, tokenization): each SEC framework has specific investor verification requirements. Regulation CF allows up to $5M/year from unaccredited investors. Regulation D is limited to accredited investors only. Regulation A+ allows up to $75M with lighter ongoing disclosure. The platform type determines which applies.

Cost of White Label Investment Platform

Depending on how much functionality you need to include, the price will vary significantly. In 2026, the market has stratified more clearly than earlier pricing guides reflect.| Tier | Scope | Timeline | Cost |

|---|---|---|---|

| SaaS White Label | Vendor-hosted branded platform, limited customization, standard feature set | 2–6 weeks | $15K–$50K setup + $2K–$15K/month |

| Custom Basic | Execution-only: stocks + ETFs, KYC/AML, portfolio view, mobile app, basic reporting | 8–12 weeks | $40,000–$80,000 |

| Custom Advanced | Basic + robo-advisor, copy trading, tax reporting (1099-B), SEC/RIA compliance layer | 12–20 weeks | $80,000–$180,000 |

| Custom Enterprise | Full wealth management: alternatives, institutional compliance, custodian integration, API, mobile | 4–8 months | $180,000–$400,000 |

A sophisticated White Label crypto exchange platform with a price of $180,000–$400,000 implements and tests 20–30 software components and modules. This includes tracking client dynamics, incoming financial flows, costs and profits, loan portfolio volume, and discount rate indicators. Complex solutions require significant time for development and implementation — from 4 to 8 months.

Frequently Asked Questions

What is a white label investment platform?

A white label investment platform is a pre-built software solution that a financial institution, fintech startup, or wealth management firm licenses and brands as its own. In 2026, a competitive white label solution includes trading infrastructure, CRM, KYC/AML compliance tooling, payment processing, and mobile apps — not just a branded interface. Depending on the model, it can be a SaaS product (vendor-hosted, monthly pricing) or a custom-built platform with full code ownership.

How much does a white label investment platform cost?

SaaS white label: $15,000–$50,000 setup plus $2,000–$15,000/month. Custom-built basic platform (execution-only, mobile app, KYC): $40,000–$80,000, 8–12 weeks. Advanced with robo-advisor and compliance layer: $80,000–$180,000. Enterprise wealth management: $180,000–$400,000. Infrastructure adds $2,000–$8,000/month. RIA registration and legal setup adds $30,000–$100,000 separately.

What's the difference between a white label investment platform and a trading platform?

An investment platform focuses on mid-to-long-term investors: portfolio construction, automated rebalancing, tax-loss harvesting, and performance tracking over time. A trading platform focuses on short-term active traders: real-time order execution, technical charting, and derivatives. Many modern platforms serve both audiences, but the regulatory requirements differ — investment platforms often require RIA registration, trading platforms require FINRA broker-dealer registration or a registered broker-dealer API partnership.

Do I need a license to run a white label investment platform in the US?

Yes, in virtually every configuration. If your platform provides automated portfolio management or investment advice: RIA registration (state-level under $100M AUM, SEC-level above). If your platform executes trades: FINRA broker-dealer registration, or routing through a registered broker-dealer API. Alternative investment platforms (crowdfunding, tokenization) use SEC exemption frameworks — Regulation CF, D, or A+. The compliance structure determines your technology architecture — decide on the regulatory path before selecting a platform.

What features should a white label investment platform include?

At minimum: KYC verification, AML transaction monitoring, portfolio tracking with real-time pricing, basic reporting, and secure account management with 2FA. Advanced platforms add: robo-advisor with risk-profile questionnaire and auto-rebalancing, copy trading, options and alternatives access, tax reporting (Form 1099-B preparation), and mobile apps. Enterprise platforms add institutional compliance tooling, custodian integration, FIX API access, and multi-currency support.

Can I customize a white label investment platform?

It depends on the model. SaaS white label solutions allow branding (logo, colors, domain) and some feature configuration, but you're constrained by the vendor's roadmap. Custom-built white label platforms built by a development company allow any customization — unique features, proprietary AI models, specific compliance flows, custom mobile apps. The decision depends on whether your product differentiation requires features a SaaS vendor won't or can't build for you.

How long does it take to launch a white label investment platform?

SaaS white label: 2–6 weeks from contract signing to live platform. Custom-built basic platform: 8–12 weeks. Advanced platform with robo-advisor and compliance layer: 12–20 weeks. Enterprise wealth management: 4–8 months. RIA registration runs in parallel and takes 1–3 months at state level, up to 6 months with SEC. Start the licensing application on day one of the project — it cannot be accelerated by finishing development faster.

What is a robo-advisor and should my investment platform include one?

A robo-advisor is an automated portfolio management feature that builds and rebalances investment portfolios based on user-defined parameters: risk tolerance, investment horizon, and financial goals. The user completes a questionnaire; the system allocates across asset classes and rebalances automatically when drift exceeds a threshold. For platforms targeting retail investors who want passive exposure rather than active trading, a robo-advisor significantly increases funded account conversion rates. Adding robo-advisor capability requires RIA registration in the US and adds $20,000–$50,000 to development cost depending on the sophistication of the allocation model.