Think of a Coinbase clone script as the fastest way to launch a fiat-first crypto exchange — one where users connect their bank accounts, buy Bitcoin with a debit card, and hold assets in a custodial wallet, just like Coinbase. Not just any exchange. A specific model: beginner-oriented, US-compliant by design, and built around fiat on-ramps from day one.

That's the distinction most articles skip. A Binance clone is built for volume traders and altcoin markets. A Kraken clone is built for professional traders who want deep order books and margin. A Coinbase clone script is built for the person who searches "how to buy Bitcoin" and ends up on your platform instead of Coinbase. Different architecture, different compliance requirements, different audience.

For startups, this model has a clear advantage. Building a crypto platform from zero can cost millions and take years. A Coinbase clone script cuts that down to weeks or months, with investment starting at a fraction of the cost. That's why entrepreneurs, fintech companies, and regional financial services businesses are choosing this route.

Why Entrepreneurs Choose the Coinbase Model

Launching a crypto exchange isn't just about code — it's about trust, speed, and regulation. That's where the Coinbase architecture wins, especially if you're targeting US retail users or any market where fiat access is the primary barrier to crypto adoption.

First, it saves time. Instead of hiring a team of 20 developers and waiting a year for an MVP, you can be live in weeks. The heavy lifting — fiat rails, wallet infrastructure, KYC flows, admin panel — is already built and tested.

Second, the Coinbase model is proven at scale. Millions of users already understand the UX pattern: link bank account → buy crypto → track portfolio. A Coinbase clone script lets you adopt that framework for your own market, whether that means serving a specific region, adding local payment rails, or launching with a niche focus.

Finally, it reduces risk. Building from scratch means higher chances of bugs, downtime, and security holes. A solution comes with battle-tested features, regular updates, and support. For entrepreneurs who care about compliance and reputation — especially in regulated markets — that's often the deciding factor.

In our exchange deployments, the clients who succeed fastest are the ones who know exactly who their first 1,000 users are before they write a line of code. The architecture follows the audience — not the other way around.

Launch your crypto exchange

get a personal technical solution

Contact us

Coinbase Clone vs Binance Clone vs Kraken Clone: Which Is Right for You?

Before choosing an architecture, it's worth being precise about what each model is actually optimized for.

|

Coinbase Clone |

Binance Clone |

Kraken Clone |

| Primary audience |

Beginners, US retail, fiat-first users |

Global volume traders, altcoin market |

Professional traders, compliance-focused |

| Fiat integration |

Core — ACH, cards, bank wire |

Secondary, less native fiat UX |

Strong — EUR SEPA, USD wire |

| Trading depth |

Spot + basic order types |

Spot, margin, futures, options, copy |

Spot, margin, futures, OTC |

| US compliance |

Native — built for US regulatory model |

Complex — originally offshore-optimized |

Strong — licensed in multiple US states |

| Native chain |

Base L2 (Coinbase-built Ethereum L2) |

BNB Smart Chain |

None |

| Subscription model |

Yes — Coinbase One replicable |

No |

No |

| Starting cost |

From $40,000 |

From $40,000 |

From $40,000 |

| Best for |

US market, fiat-first exchange, retail onboarding |

High-volume global exchange, derivatives |

Trust-first exchange, regulated markets |

If your target user is a retail investor buying their first ETH with a debit card — Coinbase architecture is the right model. If your target is a professional trader running margin strategies — it isn't. Architecture follows audience.

Core Features: Full Module Checklist

A crypto exchange is never just a "buy" and "sell" button. What makes a platform like Coinbase work is the combination of dozens of moving parts — a Coinbase clone script puts those parts together from day one.

| Module |

What's Included |

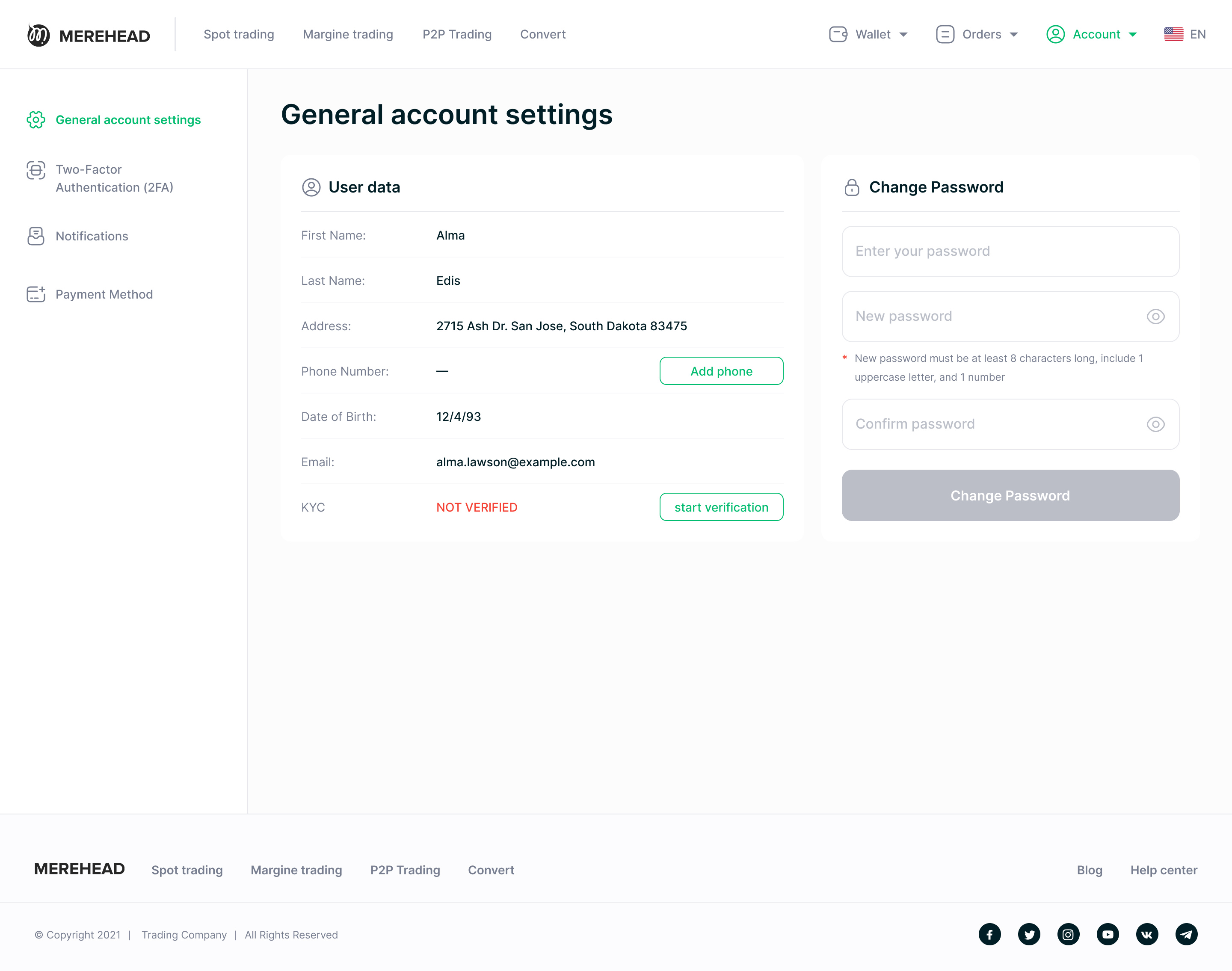

| User Onboarding |

Email/phone/social registration; progressive KYC (Level 1: email only; Level 2: ID + selfie; Level 3: bank account link); mobile-first flow |

| KYC / AML |

SumSub or Jumio integration; automated ID verification; AML transaction monitoring; SAR reporting tools for compliance officers |

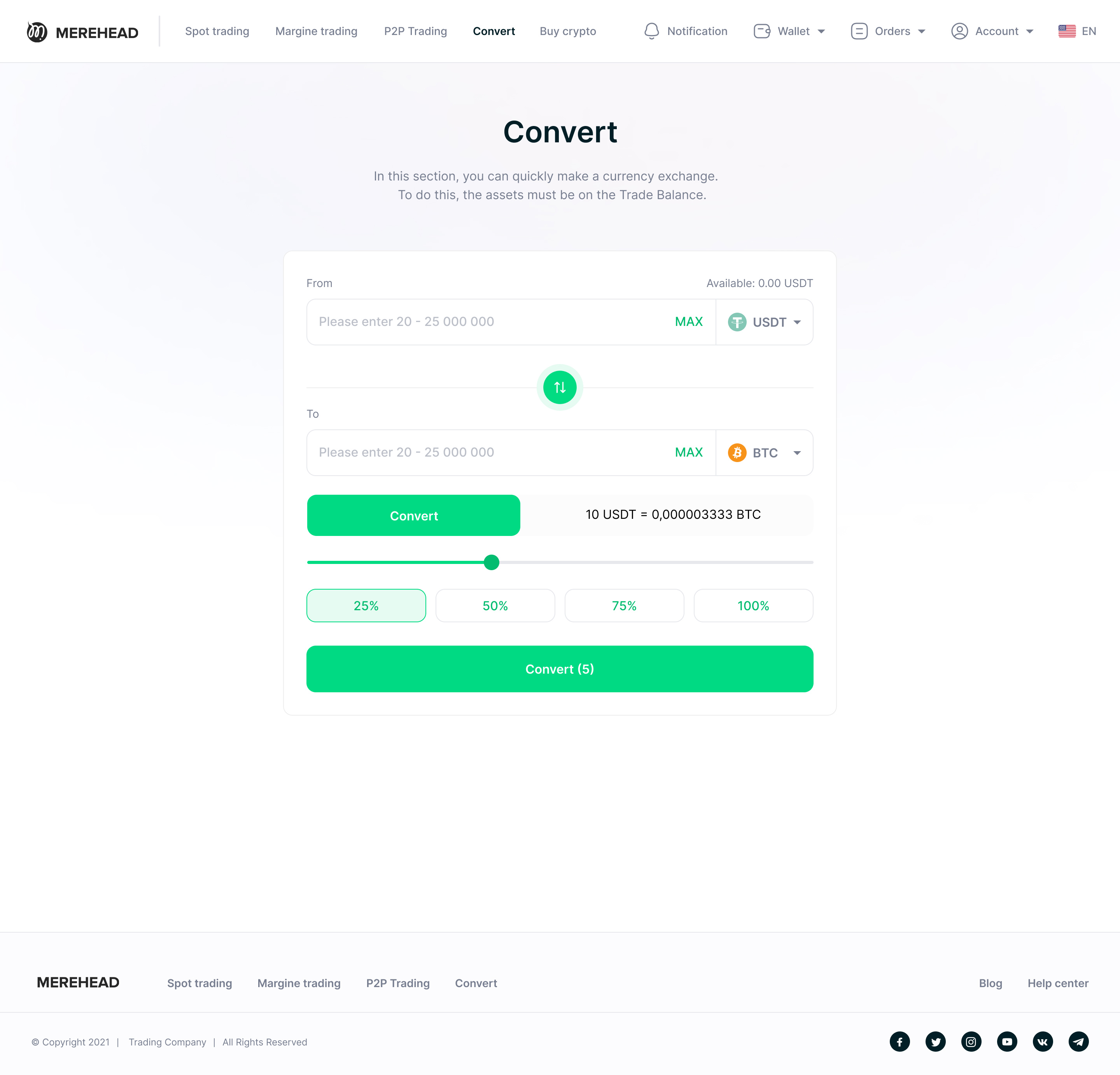

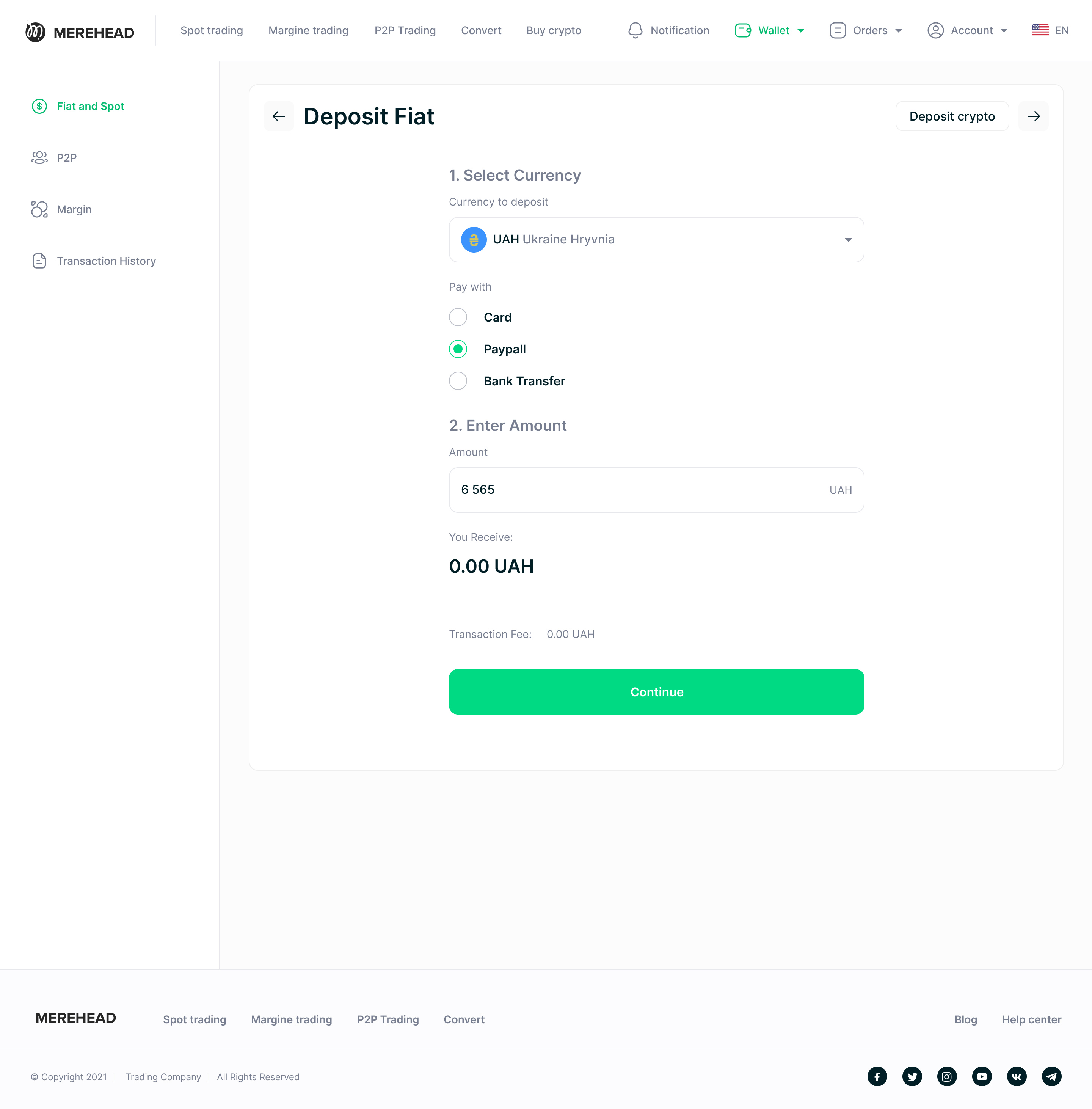

| Fiat On/Off-Ramp |

ACH bank transfer (US); SEPA (EUR); debit/credit card via Stripe or Checkout.com; wire transfer; instant buy/sell at market rate with spread |

| Crypto Wallets |

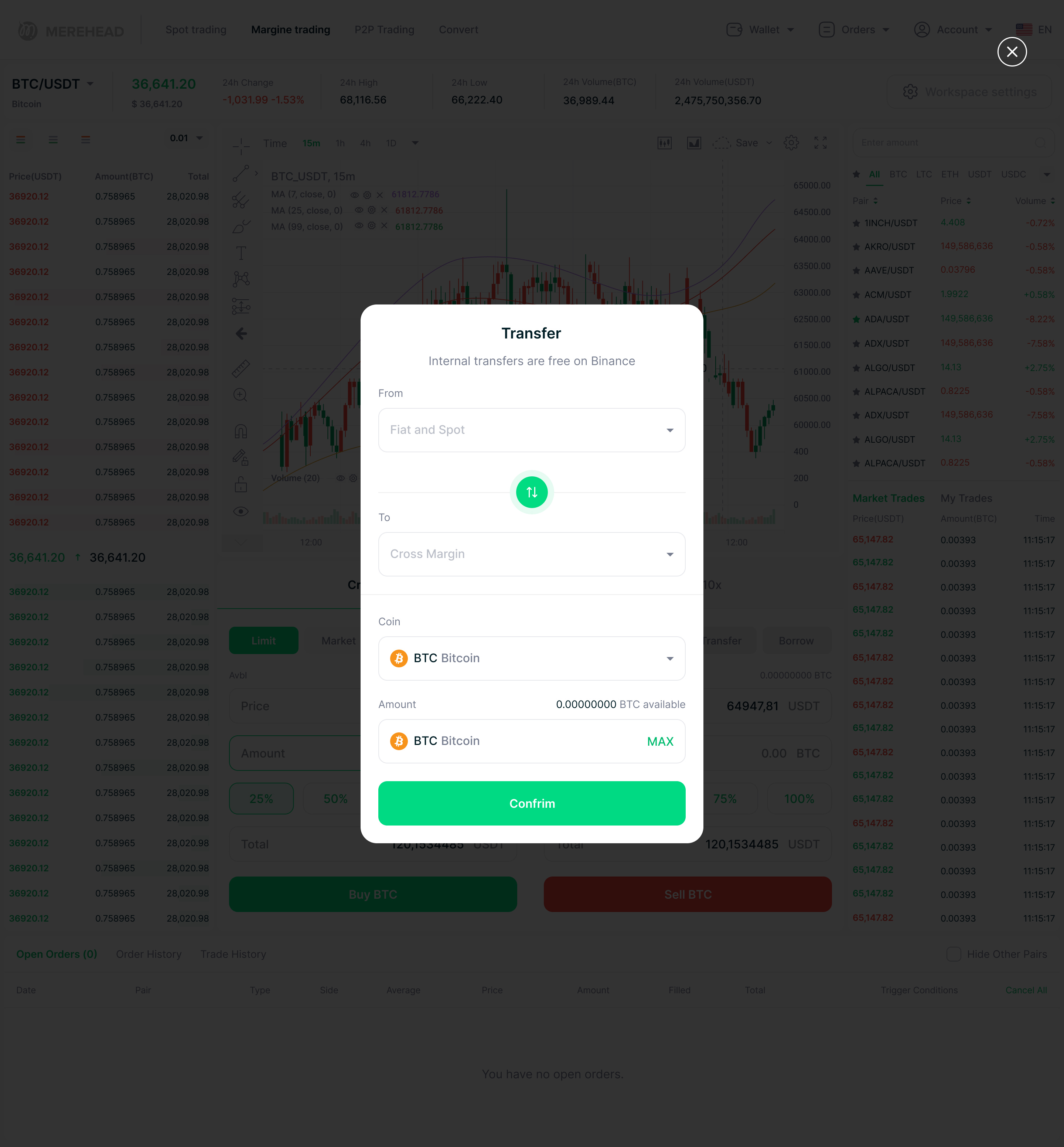

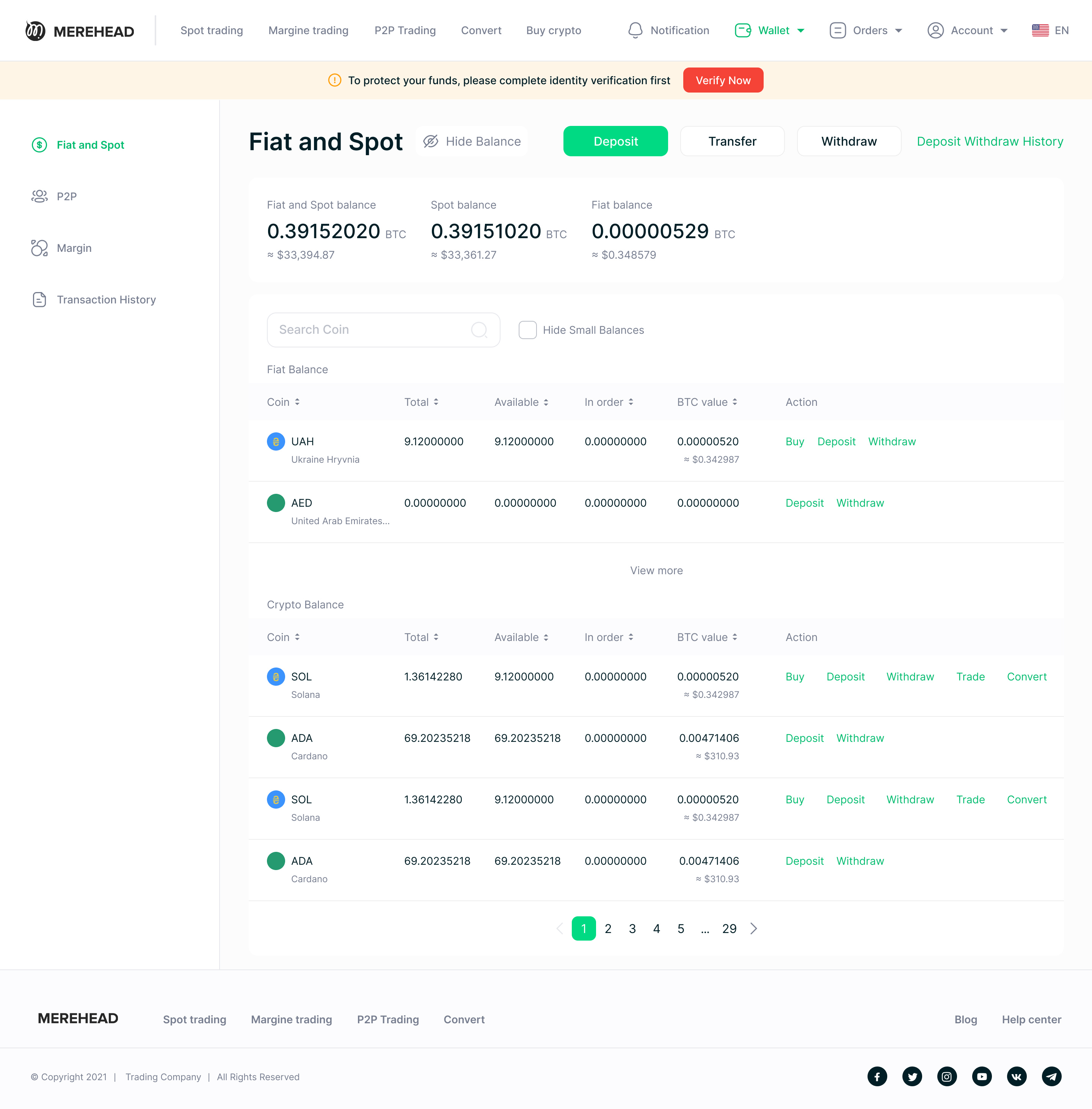

Per-user wallet generation per chain; hot/warm/cold segregation; BTC, ETH, USDT (ERC20/TRC20/BEP20), Base network, SOL, MATIC; multi-sig on treasury movements |

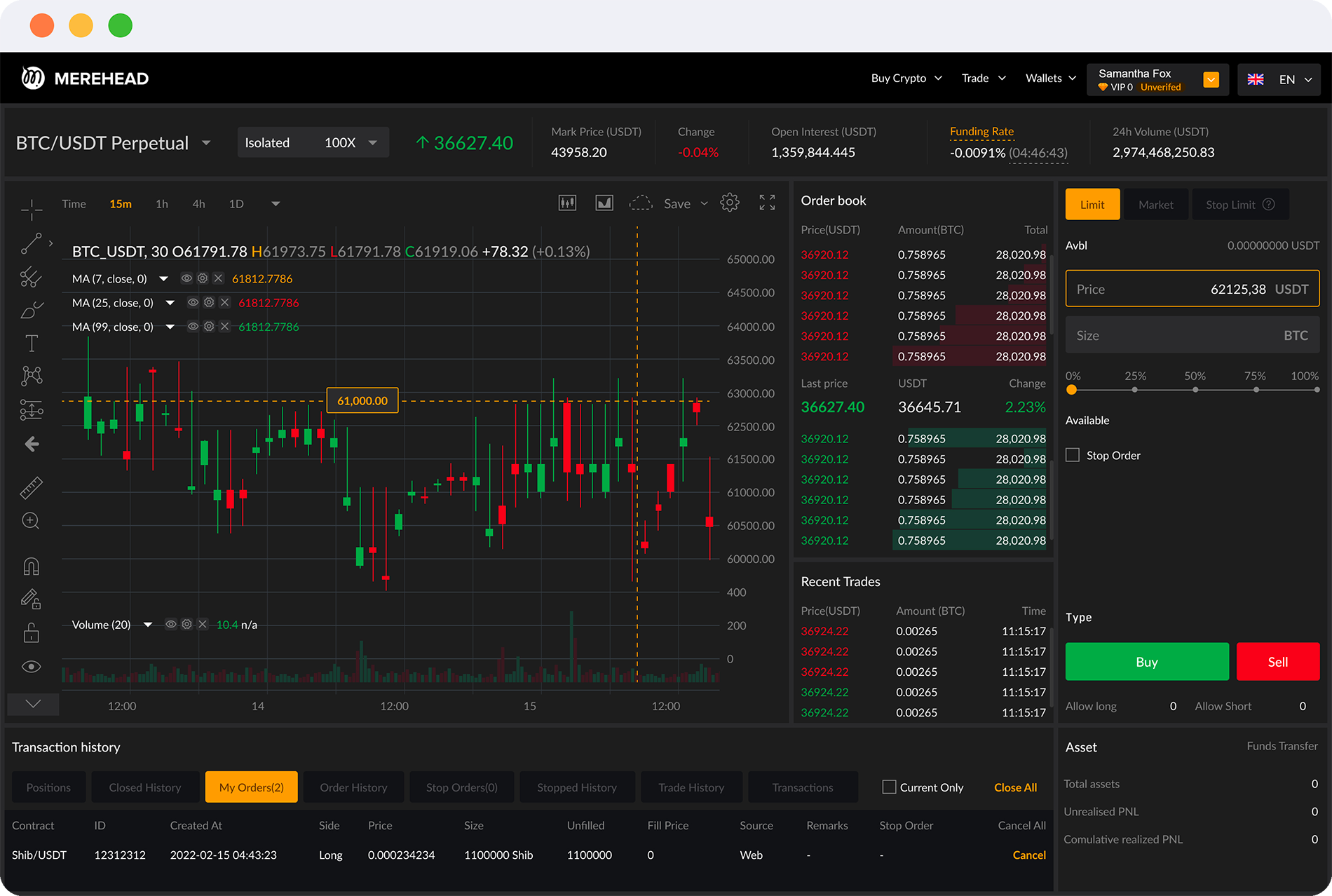

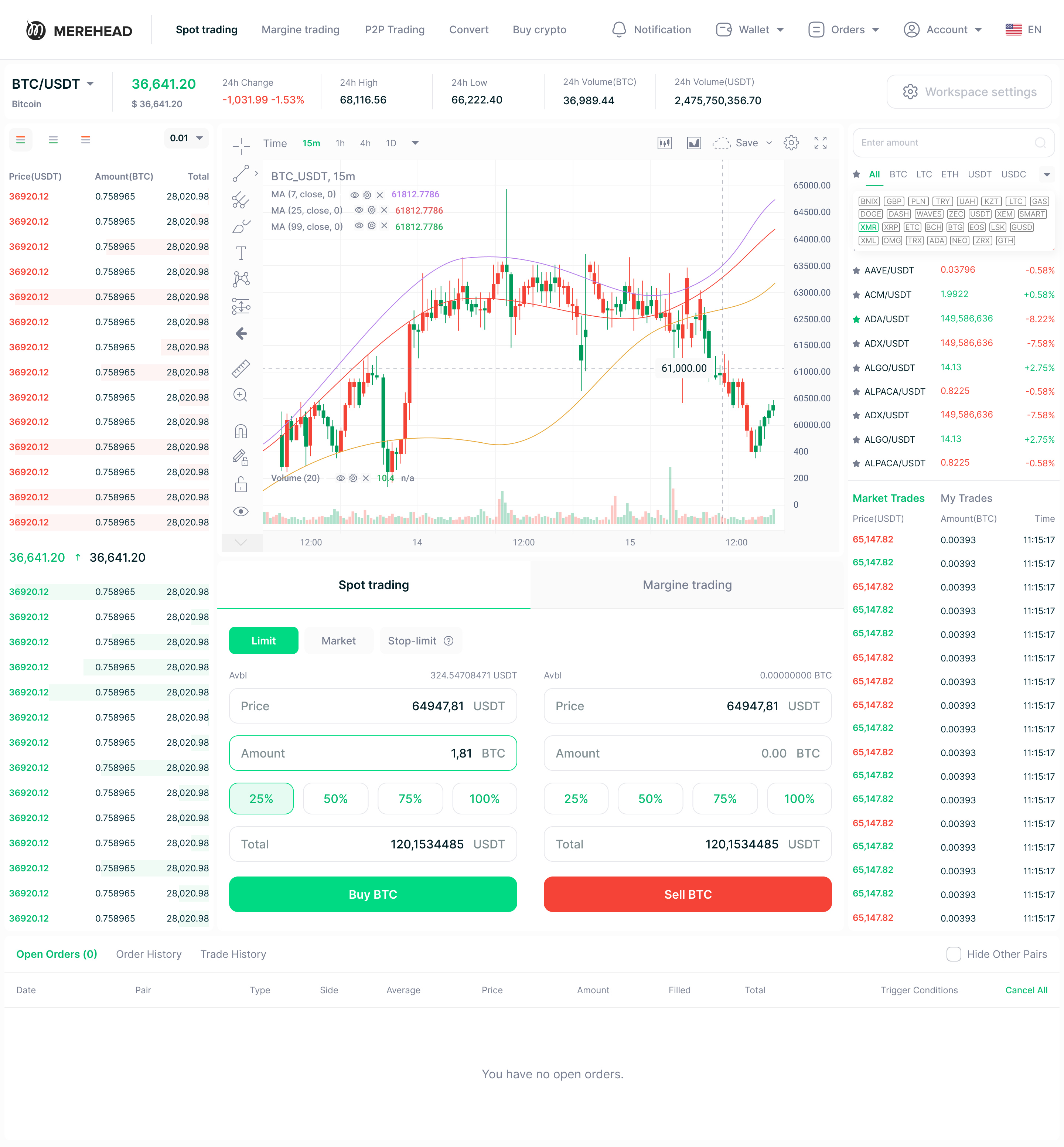

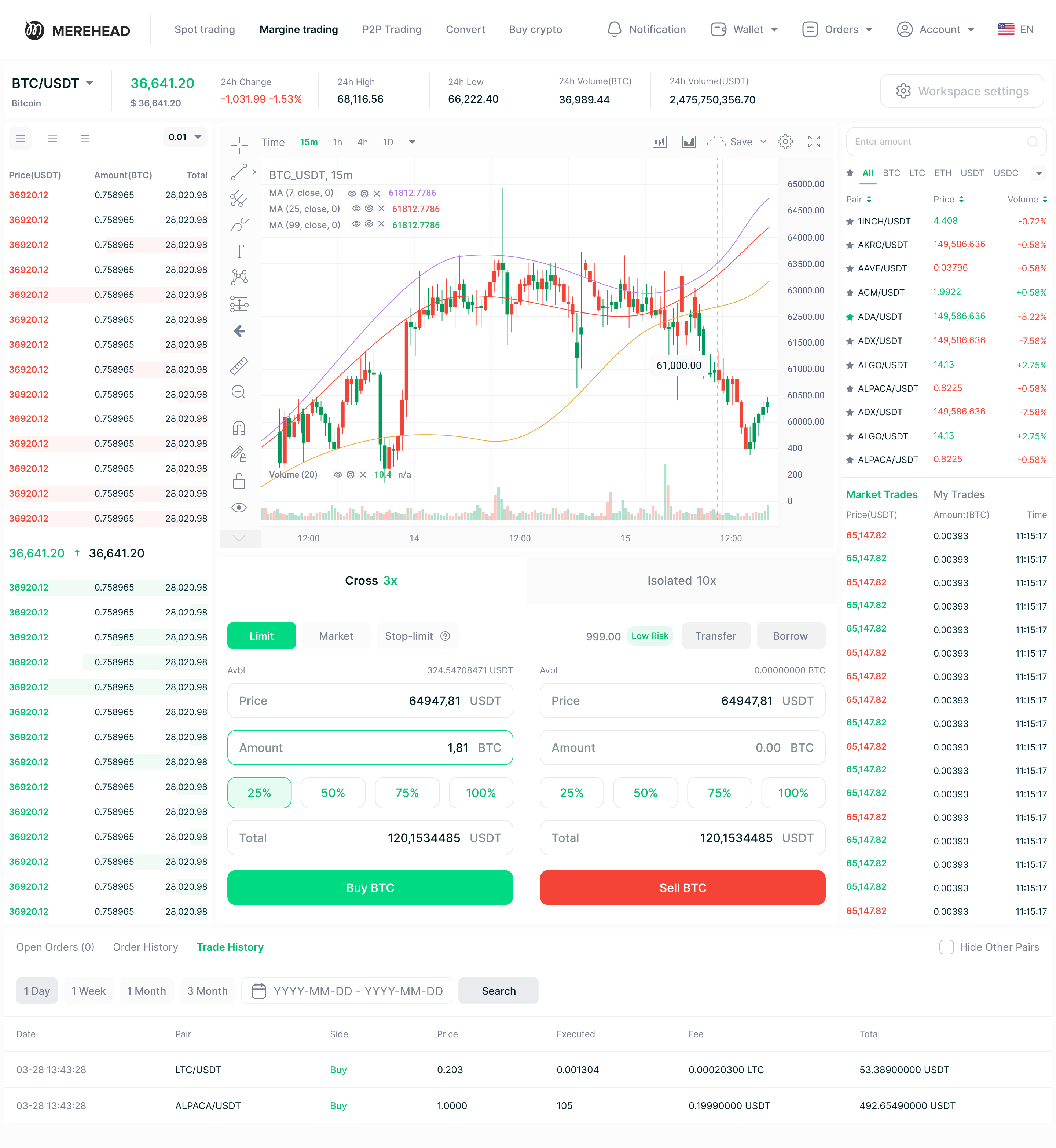

| Trading |

Market and limit orders; simple buy/sell (beginner mode); advanced order book (pro mode); real-time price feeds via WebSocket |

| Staking & Earn |

Flexible staking with configurable APY per asset; locked staking tiers; earn history dashboard; admin APY management panel |

| Subscription Tier |

Optional Coinbase One-style monthly/annual fee that removes trading commissions; configurable fee structure per tier |

| Admin Panel |

User management; KYC approval queue; withdrawal review; fee configuration; liquidity settings; compliance reporting dashboard |

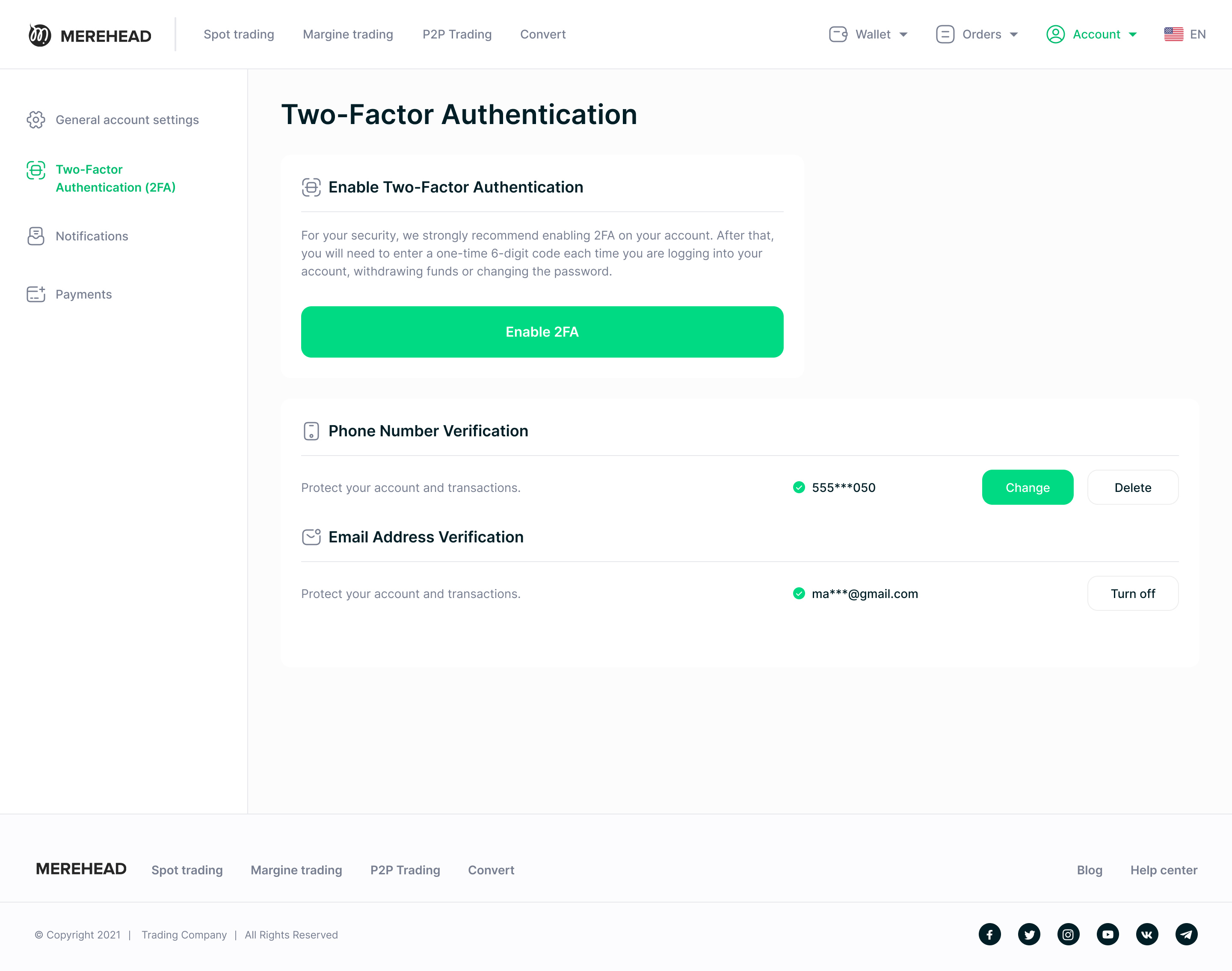

| Security |

2FA (TOTP + SMS); anti-phishing codes; IP whitelist for admin access; session management; withdrawal address whitelisting with confirmation delays; DDoS protection |

| Mobile Apps |

Native iOS (Swift) + Android (Kotlin); biometric login (Face ID / fingerprint); push notifications; real-time portfolio view |

| Blockchain Nodes |

Self-hosted: BTC, ETH, Base, USDT multi-chain — or third-party RPC (Alchemy, Infura) |

| Compliance Tools |

Transaction history exports (CSV/PDF); IRS Form 1099-DA generation; automated suspicious activity flagging; FBAR support |

| API |

Private REST API for institutional users; WebSocket price feeds; Plaid for bank link; TradingView for charting |

Example of KYC verification flow in a Coinbase-style exchange

Fiat Integration: The Technical Reality

Fiat integration is what separates a Coinbase-style exchange from every crypto-only platform. It's also where most clone script vendors give the shortest answers — because it's genuinely complex.

ACH (US Bank Transfers)

Requires partnering with an ACH processor — Plaid for bank account verification, Dwolla or Synapse for the actual transfer. Standard ACH settles in 2–4 business days. ACH Instant is faster but has lower per-transaction limits. Your platform needs to handle "pending" fiat balance states — money the user has initiated but hasn't settled — and decide whether to extend buying power before settlement (Coinbase does this, with associated risk management).

Card Payments

Visa/Mastercard's merchant category code for crypto purchases is 6051 (Quasi Cash) — many card issuers block or add surcharges for this category. Your payment provider (Stripe, Checkout.com, or Banxa) must handle chargebacks, which in crypto carry asymmetric risk: a user receives crypto, initiates a chargeback, and the crypto has already been sent. Chargeback reserves and velocity limits are standard operational requirements.

SEPA (EUR)

Straightforward for EUR-denominated accounts. SEPA Instant is available across most EU countries. The compliance burden differs from ACH — GDPR requirements apply to KYC data, and PSD2 open banking can simplify bank account verification flows.

In one of our instant exchange deployments, we integrated SEPA and USD fiat flows simultaneously. The technical work involved separate deposit/withdrawal state machines for each payment rail — because SEPA and ACH have different confirmation webhooks, different settlement windows, and different dispute processes. A unified "fiat balance" that reconciles across both rails required careful accounting logic. We also implemented Telegram and Slack alerts on pending fiat transactions older than 24 hours — a simple operational monitor that prevented several reconciliation issues from becoming user-facing problems.

US Compliance: What You Actually Need

If you're building a Coinbase-style exchange for US users, the compliance layer is not a checkbox you add before launch — it's infrastructure you design around from day one.

FinCEN MSB Registration

Any US exchange that transmits money — which includes crypto-to-fiat conversions — must register as a Money Services Business with FinCEN. This is federal-level, takes up to 180 days to process, and requires BSA/AML program documentation, a designated compliance officer, and ongoing suspicious activity reporting.

State Money Transmitter Licenses (MTLs)

Separately from FinCEN, most US states require a Money Transmitter License. As of 2026, 49 states have MTL requirements, with New York's BitLicense being the most demanding. The practical approach for most new exchanges: launch in states with lighter requirements first, expand as licenses are obtained. Operating without required state MTLs exposes you to enforcement actions.

SEC and CFTC Considerations

If your exchange lists tokens that qualify as securities or offers derivatives (futures, options), SEC and CFTC oversight applies. A Coinbase-style spot exchange limited to major cryptocurrencies (BTC, ETH, stablecoins) sits in a significantly cleaner regulatory position than one offering broad token listings or leveraged products.

Tax Reporting (1099-DA)

As of 2026, US exchanges must generate IRS Form 1099-DA for users with over $10,000 in digital asset proceeds. This requires cost-basis calculation (FIFO, LIFO, or specific identification) integrated into transaction history — a non-trivial technical feature that most generic clone scripts do not include.

Building for the US market means building compliance into sprint one, not as a post-launch add-on. Retrofitting KYC reporting, licensing infrastructure, and tax tooling onto a live exchange is significantly more expensive — and more disruptive — than building it correctly from the start.

Base L2: Why Your Coinbase Clone Should Support Coinbase's Own Chain

In 2023, Coinbase launched Base — its own Ethereum Layer 2 built on the OP Stack. By 2026, Base has become one of the highest-activity L2 networks, with billions in TVL, significant DEX volume, and a growing DeFi ecosystem.

For a Coinbase-style exchange, Base integration isn't optional context — it's a product decision with direct user impact:

Lower transaction costs. Base transactions cost a fraction of Ethereum mainnet gas. Offering Base as an alternative deposit/withdrawal network significantly reduces user costs — which directly affects how often users move funds.

Native USDC. Circle's USDC is a first-class asset on Base. For a fiat-first exchange where USDC is a primary stable pair, native Base USDC means near-instant, near-free USDC transfers compared to ERC-20 USDC on mainnet.

DeFi bridge opportunity. An exchange supporting Base can offer users a path between their custodial balance and Base DeFi protocols — earning, lending, liquidity provision — without leaving your platform's interface.

From a technical perspective, Base is an Ethereum-compatible RPC integration — same library stack as ETH, different chain ID and RPC endpoint. For exchanges already running Ethereum nodes, adding Base support is a matter of weeks. The indexing, wallet generation, and transaction monitoring logic reuses from the ETH implementation with configuration changes. It's one of the highest ROI integrations available for a Coinbase-style exchange in 2026.

How Coinbase Makes Money — and What to Replicate

When Coinbase first launched, it was little more than a wallet with a buy button. Today, it's a multi-billion dollar business with revenues streaming in from multiple directions. The lesson for anyone building on a

Coinbase clone script is simple: exchanges thrive when

their crypto business model isn't tied to just one source of income.

Revenue streams in a Coinbase-style exchange

The most visible stream: trading fees. Every buy or sell generates a commission. Coinbase uses a spread model for simple trades (built-in margin between buy and sell price) and a maker-taker model for the advanced order book. Both are configurable in a Coinbase clone script from day one.

Beyond that, Coinbase One-style subscription tiers are increasingly common — a flat monthly fee that eliminates per-trade commissions in exchange for predictable revenue. For high-frequency retail users, this is attractive. For the platform, it converts variable fee revenue into recurring subscription income.

Additional streams worth building in from launch: staking and earn products (take a spread on the APY you offer users vs. what the protocol pays), listing fees for new tokens, fiat withdrawal fees, and eventually custody services for institutional clients once volume justifies it.

A strong exchange doesn't rely on one faucet. It builds a network of revenue streams that keep cash flowing in bull and bear markets alike. Trading fees are the foundation — subscriptions, staking, and institutional services are what scale it.

How to Approach Development: From Templates to Full Custom Builds

Not every crypto business starts from the same place, and the

way you build your trading platform will depend on budget, timeline, and how much you're willing to own operationally.

Some founders test the waters with a simple clone script. Think of it as an off-the-shelf package: sign-up, wallet, buy/sell, live in weeks. It's inexpensive, but fragile — security gaps, limited features, and little room to scale.

Exchange UI/UX mockups for a Coinbase-style platform

Others take the middle road with a Coinbase clone script. The foundation is solid, the infrastructure is production-tested, and you can rebrand it, add payment methods, or expand to new chains. Vendors provide updates and support. That's why most funded startups use this route — speed to market without sacrificing credibility.

Then there are teams who build fully custom. Complete control, unique architecture, but expensive, slow, and requires a strong in-house engineering team to maintain.

Merehead Crypto Exchange — white label base with full customization

In reality, the path is often hybrid: launch with a proven solution, validate the business, then gradually rebuild with custom features as revenue justifies it.

Merehead software

Crypto Exchange

A ready-made solution with a wide range of functions. Software that can be installed in a couple of days. Launch your online trading platform!

Gallery

Start with us

Costs and Timelines: What It Really Takes to Launch

Here's the part most founders underestimate. Building a crypto exchange isn't just about writing code — it's about capital, compliance, and ongoing operational costs.

| Configuration |

Scope |

Timeline |

Starting Cost |

| Spot MVP |

Spot trading, basic KYC, external liquidity API, hot/cold wallets — no fiat |

8–10 weeks |

From $40,000 |

| Fiat-Enabled Exchange |

MVP + ACH/SEPA, bank verification (Plaid), card payments, FinCEN compliance tools |

12–16 weeks |

From $80,000 |

| Full Coinbase-Style Platform |

All above + staking, subscription tier, mobile apps, US tax reporting (1099-DA), multi-state MTL support |

16–24 weeks |

From $150,000 |

| Custom + Institutional |

Full platform + custody APIs, OTC desk, prime brokerage integrations, CFTC derivatives module |

6–12 months |

From $300,000 |

Ongoing infrastructure costs: $2,000–$6,000/month depending on trading volume — blockchain node hosting, cloud infrastructure, KYC API calls, payment processor fees.

The most common cost surprise is fiat payment processing. The technical integration of ACH or SEPA adds $15,000–$25,000 in

development cost and 3–4 weeks to the timeline. But the ongoing cost is what most clients don't model upfront: payment processors charge 0.5–2% per fiat transaction plus chargeback reserves of 5–10% of monthly volume. On a platform processing $1M/month in fiat, that's $5,000–$20,000/month in processor fees before any exchange revenue. We build this into client financial models from day one to avoid post-launch surprises.

Step-by-Step Deployment: What the Timeline Actually Looks Like

Weeks 1–2: Architecture and compliance decisions. Lock your initial jurisdiction (which US states, which countries), KYC provider, fiat payment processor, and initial trading pair list. Apply for FinCEN MSB registration on day one — processing takes up to 180 days and cannot be accelerated. Start blockchain node synchronization immediately: Bitcoin takes 5–10 days, ETH and Base sync in 1–3 days each.

Weeks 2–4: Core platform configuration. Configure trading engine, wallet architecture (hot/warm/cold), and initial trading pairs. Begin UI/UX customization — branding adaptation takes 2–3 weeks.

Weeks 3–5: KYC/AML integration. Integrate KYC provider API, configure identity verification flows, build KYT transaction monitoring on all deposits, set AML risk scoring with threshold-triggered account flags. Configure IRS 1099-DA cost-basis tracking for US deployments.

Weeks 4–7: Fiat integration. Integrate bank verification (Plaid), ACH transfer processing, and card payment gateway. Build fiat deposit/withdrawal state machines (pending → processing → settled → failed). Configure chargeback monitoring. Test with real small-denomination transactions — sandbox behavior differs from live networks.

Weeks 6–8: Security hardening. Admin panel IP whitelisting, 2FA enforcement for all admin actions, withdrawal address whitelisting with confirmation delays, penetration testing on auth and withdrawal flows, load test at 2x projected peak volume.

Weeks 8–10: Staking, mobile apps, and monitoring. Configure staking module (APY per asset, lock periods, reward distribution). Deploy iOS and Android apps with biometric authentication. Set up operational monitoring: Telegram/Slack alerts on node health, pending withdrawals, AML flags.

Weeks 10–12: QA and launch. End-to-end testing on all flows including fiat deposit → trade → crypto withdrawal. Soft launch with invitation-only group, then public.

The single most common delay we see isn't development — it's payment processor onboarding. Processors run their own compliance review of your exchange before approving you, which takes 4–8 weeks independently. Start the processor application at week one alongside development, not after.

Find out

how much it

costs to develop

your crypto exchange

Share your requirements with our Solutions Architect — we'll send back a per-module hour breakdown within 48 hours, at no cost.

Request an estimate

Conclusion: Why a Coinbase Clone Script Could Be Your Fastest Path to Market

Launching a crypto exchange from scratch is expensive, slow, and risky. That's why so many founders are choosing the

Coinbase clone script route. It gives you a proven foundation — fiat rails, wallets, KYC, trading engine, security — without waiting years or burning millions in development.

But remember: the script is just the starting point. What decides whether your platform succeeds is the compliance infrastructure you build around it, the fiat payment rails you connect, and the trust you establish with your first users. The architecture gives you speed. The execution gives you longevity.

If you're targeting the US market or any region where crypto adoption depends on fiat access — a Coinbase clone script is the most direct path to a platform that meets users where they are.

Frequently Asked Questions

Is a Coinbase clone script legal in the US?

Yes — clone script software is legal. The legal requirements apply to operating the exchange, not the software itself. In the US, you need FinCEN MSB registration, Money Transmitter Licenses (MTLs) in the states where you operate, and SEC/CFTC compliance if listing securities or derivatives. The timeline for full US licensing typically runs 6–18 months depending on target states. Most exchanges launch with federal MSB registration and a subset of state licenses, then expand.

What's the difference between a Coinbase clone and a Binance clone?

Architecture and audience. Coinbase is fiat-first — designed around converting USD to crypto, with bank account linking, ACH integration, and beginner-friendly UX. Binance is volume-first — designed for high-frequency trading, altcoin markets, and derivatives. A Coinbase clone is the right foundation if your target user is a US retail investor buying their first ETH. A Binance clone is right if you're building for professional traders running margin and futures strategies.

Does a Coinbase clone support the Base network?

It can and should. Base is Coinbase's own Ethereum L2 with near-zero gas costs and a growing DeFi ecosystem. For a Coinbase-style exchange, Base integration enables cheaper USDC transactions, lower ETH gas costs for users, and a bridge between custodial exchange balances and DeFi protocols. Base uses the same Ethereum-compatible stack — adding it to an ETH-capable exchange takes 2–3 weeks, not months.

How much does fiat integration add to cost and timeline?

ACH/SEPA/card integration adds $15,000–$25,000 in development cost and 3–4 weeks to the timeline. The larger factor is payment processor onboarding — processors run their own compliance review of your exchange before approving you, which takes 4–8 weeks independently. Start the processor application on day one alongside development, not after it finishes.

What KYC levels are required for a US exchange?

At minimum: Level 1 (email + phone) for small balances, Level 2 (government ID + selfie via SumSub or Jumio) for withdrawals above $100/day, Level 3 (bank account via Plaid, proof of address) for fiat ACH access and limits above $10,000. FinCEN BSA rules require identity verification for transactions above $3,000 and SAR filing for suspicious activity above $5,000.

How long does it take to launch a Coinbase clone?

Spot trading only, no fiat: 8–10 weeks. With ACH/SEPA fiat integration: 12–16 weeks. Full platform with staking, mobile apps, and US tax reporting: 16–24 weeks. The single longest delay factor is payment processor onboarding — start this at week one of the project.

Does a Coinbase clone support staking?

Yes. A staking module handles flexible and fixed-term lock-ups, APY configuration per asset in the admin panel, daily reward calculation and crediting, staking history per user, and an optional subscription tier offering premium APY for paid members — replicating the Coinbase One value proposition.

What are the ongoing operational costs?

Infrastructure runs $2,000–$6,000/month for servers, blockchain nodes, and monitoring. KYC API costs $0.50–$2.00 per verification. Payment processing adds 0.5–2% of fiat transaction volume plus a chargeback reserve. Development partner retainer for support and updates: $3,000–$8,000/month. Total at low volume ($500K/month fiat): approximately $15,000–$25,000/month operational cost before exchange revenue.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}