A complete guide to developing a crypto banking app: key features, development steps, cost, and expert tips.

Introduction to Crypto Banking

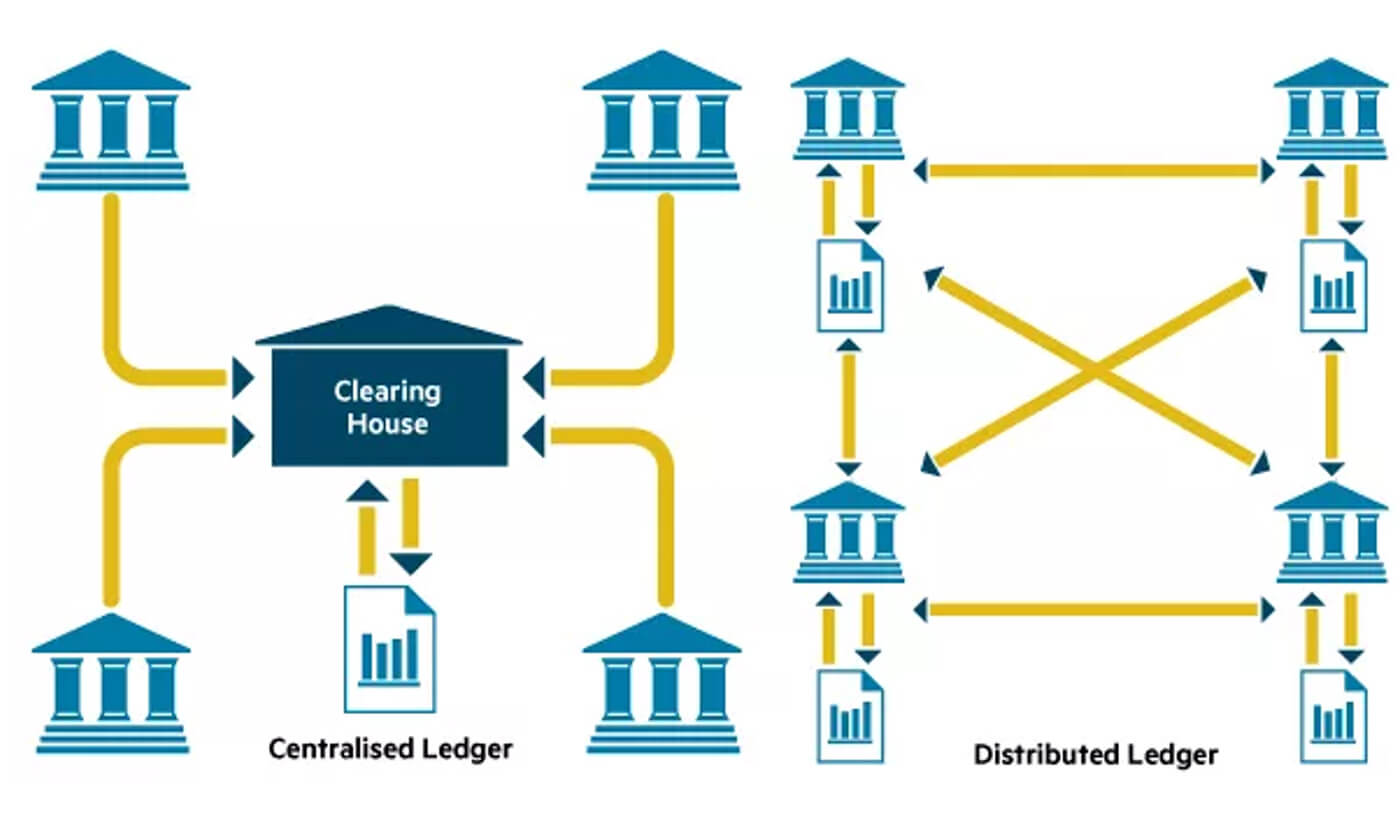

Crypto banking has emerged as a revolutionary force in the financial sector, transforming the way individuals and institutions interact with money. By integrating cryptocurrencies into traditional banking systems, crypto banking bridges the gap between digital innovation and established financial practices. This fusion has paved the way for a new era of banking systems, where efficiency, security, and accessibility are at the forefront.Unlike traditional banking, which relies on centralized authorities and legacy infrastructure, crypto banking leverages advanced technologies to deliver faster, more transparent, and borderless financial services. As a result, both consumers and businesses are experiencing unprecedented flexibility and control over their financial assets, signaling a fundamental shift in how banking is perceived and delivered.

What is a Crypto Bank?

Cryptobank — a modern financial application or digital platform that provides banking services based on cryptocurrencies and digital assets. Unlike traditional banks that operate through centralized structures and regulated financial networks, cryptobanks rely on blockchain technologies, smart contracts, and decentralized protocols, providing customers with a high level of autonomy, transparency, and accessibility. Many cryptobanks offer a user controlled wallet, giving users full autonomy over their digital assets and private keys.Cryptobanks combine the best of both worlds — they provide familiar financial services, but they do so in Web3 format, where the user has expanded control over assets, and interaction processes become more flexible and efficient. Cryptobanks also streamline banking operations, reducing costs and increasing efficiency compared to traditional banks.

Digital banking features are integral to cryptobanks, enabling users to access a wide range of services similar to those found in traditional banks but within a digital context.

Evolution of Banking Systems

The journey of banking systems has been shaped by continuous technological innovation. From the early days of brick-and-mortar branches to the rise of online and mobile banking apps, each advancement has brought greater convenience and accessibility.However, the advent of cryptocurrencies has sparked a paradigm shift, introducing decentralized, digital banking systems that operate independently of traditional financial institutions. This evolution has given rise to crypto banks—specialized platforms that offer a comprehensive suite of digital banking services using crypto assets. These crypto banks empower users to save, invest, borrow, and make payments with digital currencies, all within user-friendly banking apps.

As digital banking becomes increasingly mainstream, financial institutions are adapting to this new landscape, integrating digital assets and blockchain-driven solutions to remain competitive and relevant in a rapidly changing market.

Banking Industry Overview

The banking industry is currently experiencing a profound transformation, fueled by the rapid adoption of digital technologies and the growing demand for crypto banking solutions. Financial institutions are recognizing the immense potential of cryptocurrencies to enhance their service offerings, streamline operations, and reduce costs.As a result, many banks are actively exploring or developing crypto banking platforms that deliver a host of benefits, such as heightened security, faster transaction processing, and a superior customer experience. These crypto banking solutions are not only reshaping the way banks operate but are also setting new standards for innovation and efficiency within the banking industry.

By embracing crypto banking, financial institutions are positioning themselves at the forefront of the digital revolution, ready to meet the evolving needs of modern consumers and businesses with cutting-edge banking solutions.

Key functions of cryptobanks:

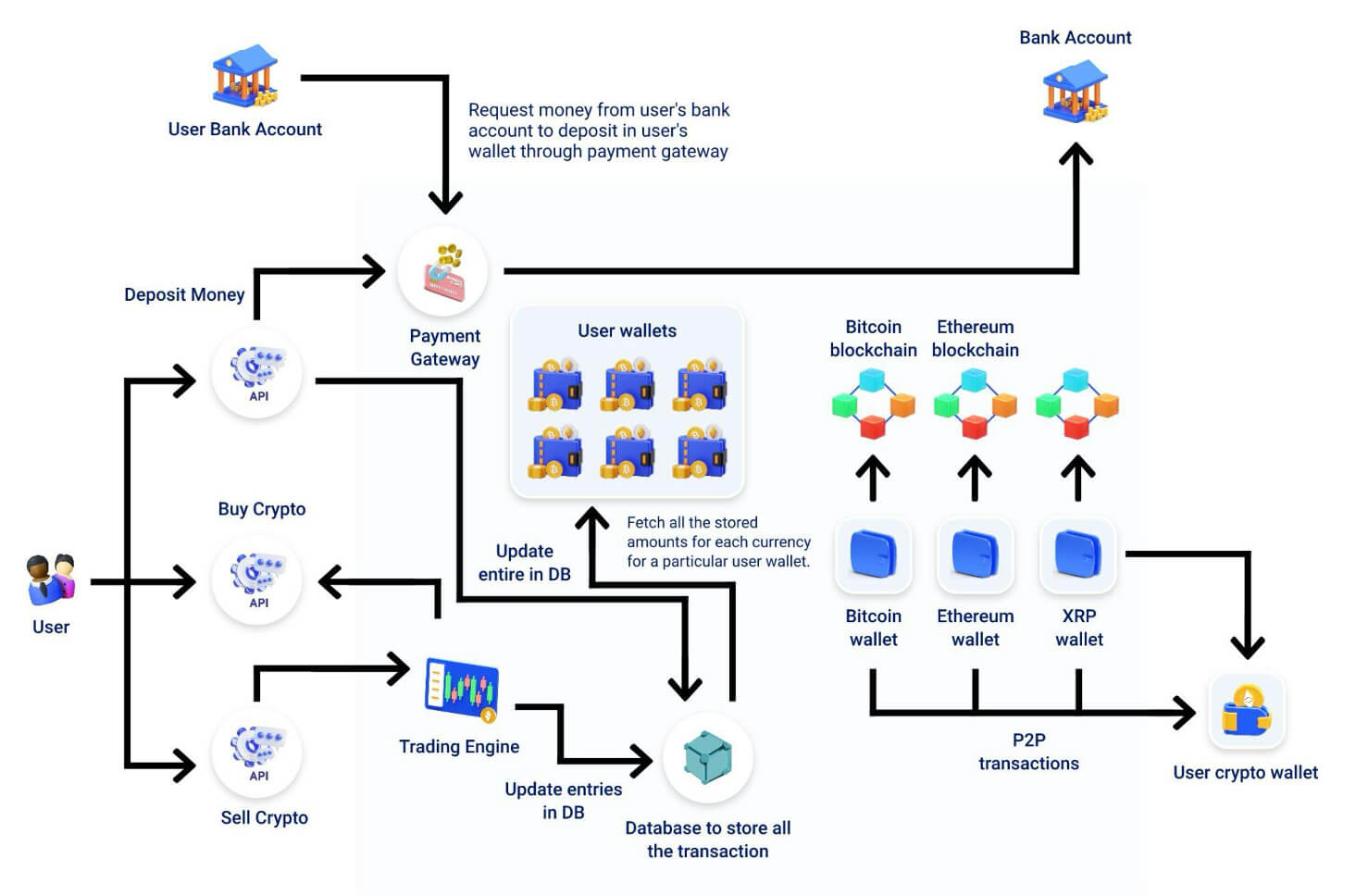

- A wallet for storing cryptocurrencies: Solutions are offered both in the format self-custody (user controls the private keys themselves), as well as custodial (storage of assets on the bank's side with protection through insurance and audit).

- Exchange services: Mechanisms for the rapid conversion of crypto assets into fiat currencies and vice versa, as well as between different cryptocurrencies based on spot prices or through DeFi-pools of liquidity.

- Deposits and staking: Users can place cryptocurrencies at an interest rate, similar to bank deposits. Profitability is achieved through DeFi-protocols, loyalty programs, or internal lending platforms.

- Lending and loans: Issuing crypto loans secured by digital assets, or providing loans without intermediaries through smart contracts.

- Payment solutions: Issuance of virtual and physical crypto-cards for payments in stores, online payments and cash withdrawals at ATMs, with instant asset conversion.

- Integration with CeFi and DeFi ecosystems: Many cryptobanks create hybrid solutions, combining centralized infrastructure with access to DeFi-protocols to optimize profitability and increase customer capabilities.

- Fiat gateways: Support for bank transfers via SWIFT, SEPA, ACH and other payment systems for convenient deposit and withdrawal of funds.

Through the use of blockchain, cryptobanks provide a high level of transparency, process automation, low transaction costs, and the ability to access globally without the need for a local banking infrastructure.

Top examples of cryptobanks

1. Revolut

Revolut — is one of the largest European fintech startups, which has been actively integrating cryptocurrency-related services into its ecosystem since 2018. Although the company initially focused on traditional banking and payment services, today Revolut is steadily developing towards combining classic finance and digital assets in one mobile application.

The company aims to combine traditional and digital finance in one mobile interface, where users can simultaneously manage their traditional funds and crypto assets — easily, securely and in real time.

2. Nexo

Nexo — one of the most recognizable CeFi-cryptobanks offering loans secured by cryptocurrencies, high-yield deposits (up to 16% per annum), as well as a multifunctional wallet.

The project operates under licenses in a number of European jurisdictions (including Lithuania and Switzerland), which allows it to ensure a high level of regulatory compatibility. In addition, Nexo actively implements KYC/AML standards, cooperates with well-known auditors (for example, Armanino) and uses asset insurance through specialized custody platforms (such as BitGo and Ledger Vault).

3. SwissBorg

SwissBorg — this is a new generation Swiss platform that combines the capabilities of a cryptobank and an investment application. The project focuses on simplifying access to investments in digital assets for a wide audience through the use of algorithmic portfolio management and automated transaction optimization.

It combines cryptobanking functions (storage, staking, analytics) with a flexible user interface and licensed activities in Europe.

With its focus on the investment component and intuitive interface, SwissBorg is becoming one of the most promising solutions for users who want to manage their crypto portfolio within a regulated ecosystem.

4. Bankera

Bankera — an ambitious European project focused on building a complete analogue of a traditional bank based on blockchain. Initially initiated by the SpectroCoin team, Bankera aims to combine cryptocurrency technologies with familiar financial services for individuals and businesses. It includes debit cards, multi-currency accounts, loans, and even IBAN numbers for SEPA transfers.

The project is actively developing towards licensing and compliance with the regulatory requirements of the European Union. Bankera is registered as a provider of virtual asset services (VASP) in some EU jurisdictions, and is also working on obtaining additional licenses to provide a wider range of financial products.

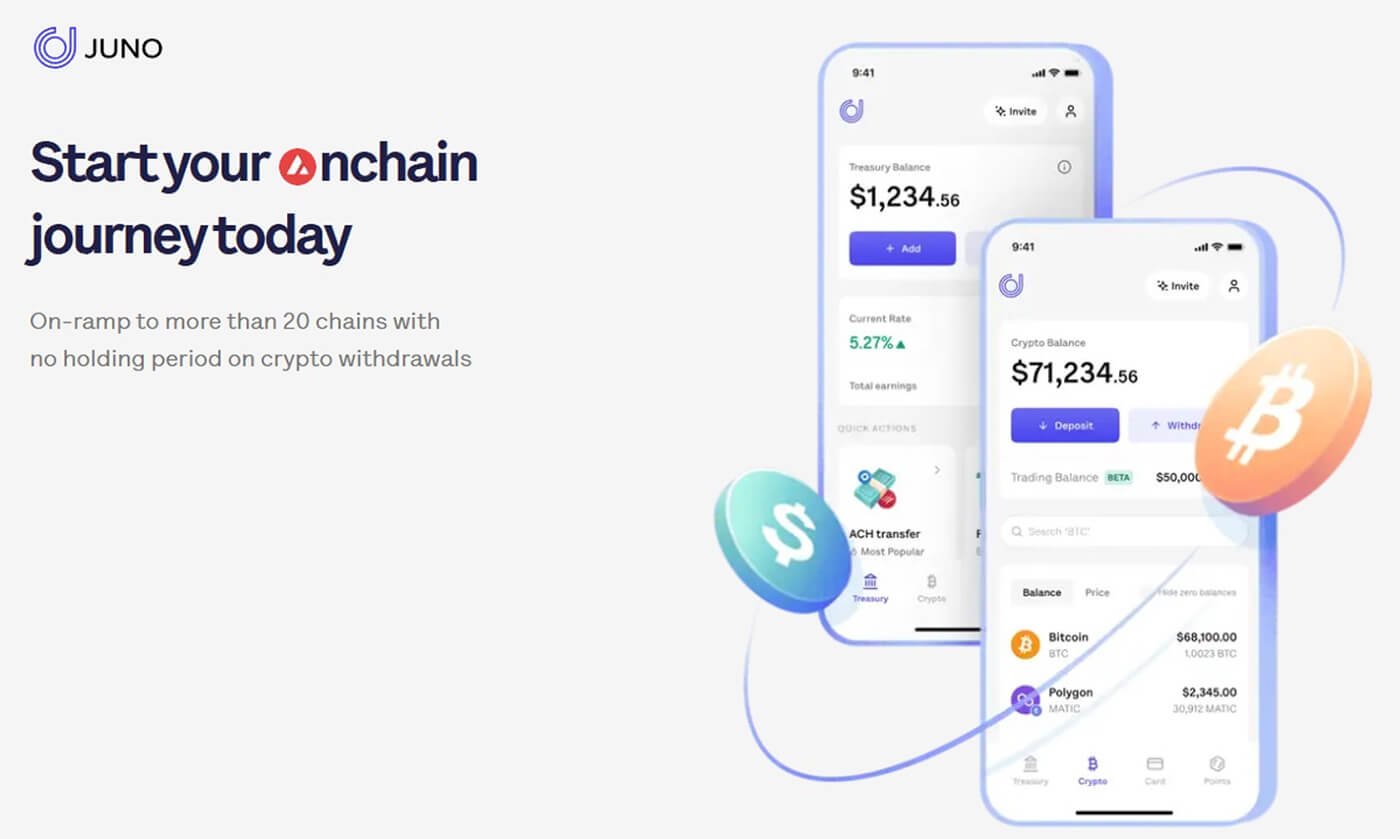

5. Juno

Juno — this is a modern American platform aimed at integrating traditional banking services with the possibilities of working with cryptocurrency. It is a unique hybrid between a classic banking application and a crypto bank, providing a convenient transition between the two financial worlds.

Users can directly receive a salary in USD, store and convert cryptocurrencies, as well as use a debit card with support for digital assets.

The company focuses on the US market and aims to become a bridge between fiat money and the crypto economy, offering users maximum flexibility in managing their digital and traditional finances through a single application.

How Does a Crypto Bank Work?

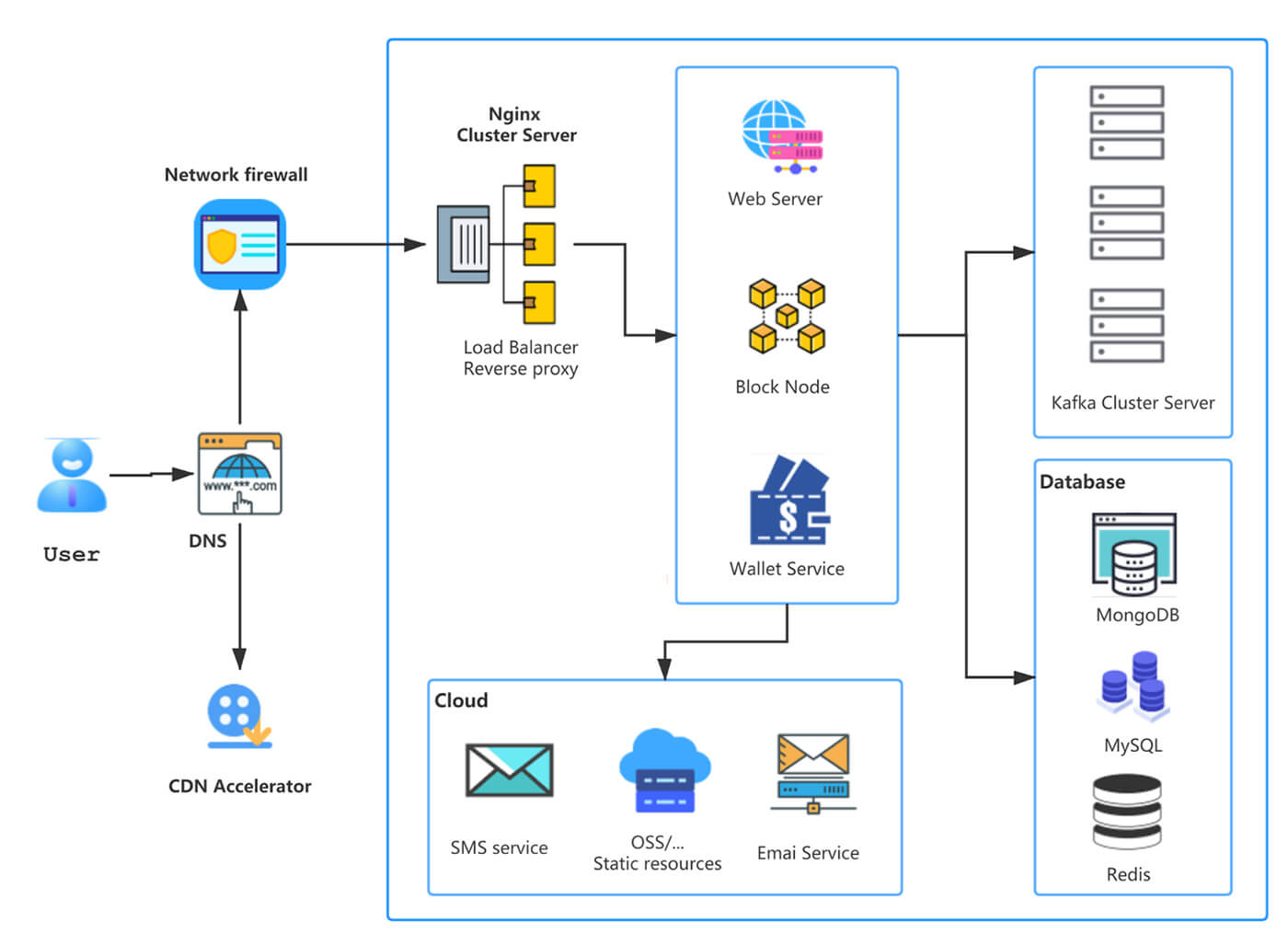

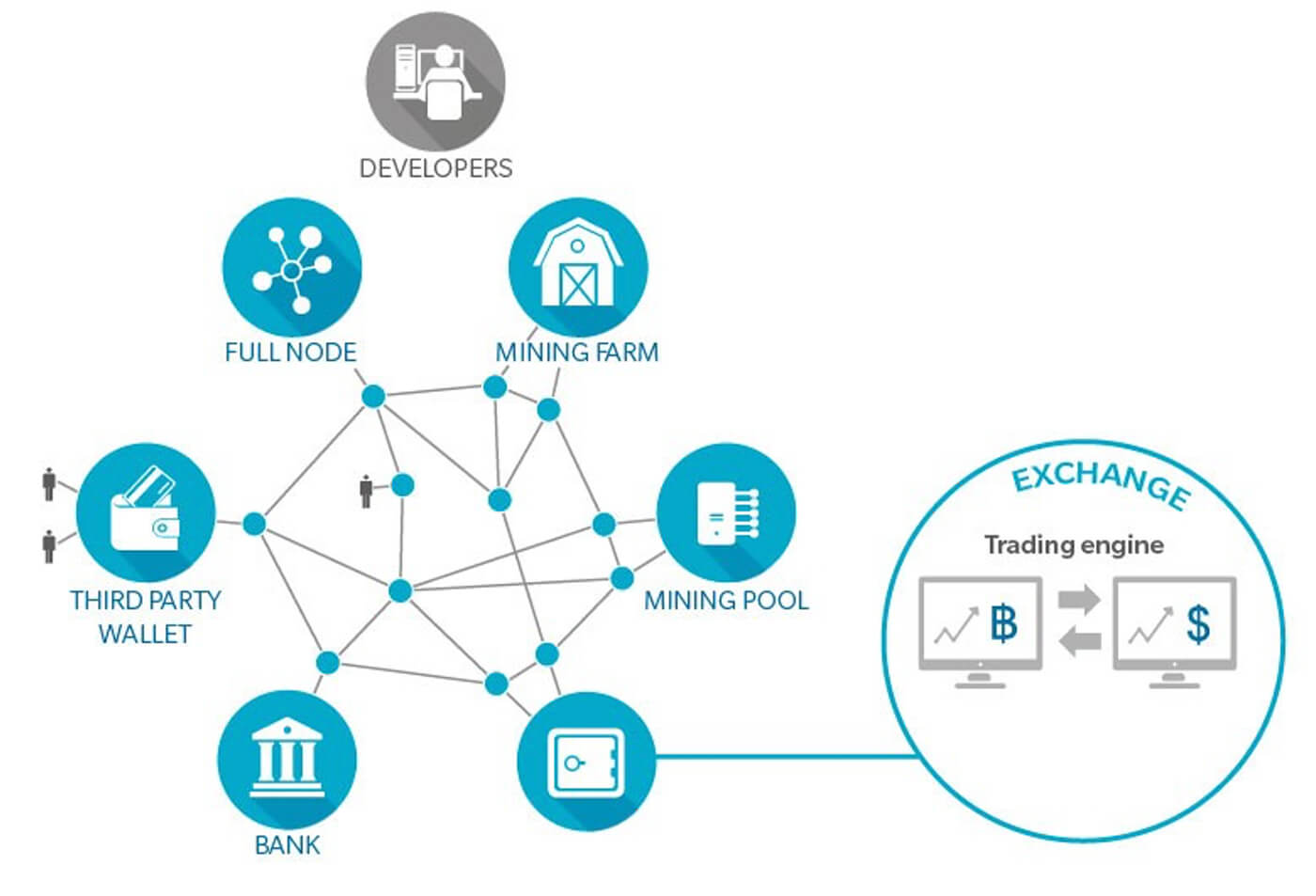

Cryptobank’s work is a symbiosis of traditional banking infrastructure and decentralized technologies. It is based on a distributed architecture that combines the functions of storing, managing, exchanging and moving digital assets with interfaces understandable to users accustomed to classic online banking.Crypto banks enable cost effective international transactions by leveraging blockchain technology and multi-currency support, reducing fees and processing times compared to traditional methods.

Each transaction in a cryptobank is initiated through a user interface, but technically it includes interaction with the API of third-party liquidity providers, blockchain nodes and a risk management module that monitors abnormal actions in real time.

Regulatory uncertainty remains a challenge for crypto banks, as evolving compliance requirements can impact operations and service offerings.

Modern cryptobanks are also implementing intelligent algorithms that automatically redistribute assets between different liquidity pools or staking protocols to ensure maximum profitability for customers, while integrating robust security features to protect user assets and ensure safe transactions.

In addition, many platforms are developing internal tokenomics and loyalty programs that stimulate user activity through cashbacks, bonuses, and commission reductions when using the service frequently.

Key components of a cryptobank:

Multi-currency wallet

The heart of any cryptobank — a wallet that supports the storage of various cryptocurrencies (BTC, ETH, USDT, etc.), tokens (ERC-20, BEP-20, etc.), as well as often stablecoins and fiat currencies. Depending on the model, the wallet can be:- Custodial — user's funds are stored in wallets managed by the bank.

- Non-custodial — user controls the private keys himself, and the bank provides only the interface and access to the functions.

Integration with blockchains and exchangers

Cryptobank interacts with various blockchain networks through nodes, API connections, and liquidity aggregators (for example, 1inch, Uniswap, Changelly) to ensure instant asset conversion, transaction processing, and staking.Fiat gateways (on/off ramps)

Through payment providers (Simplex, Moonray, Mercuryo, etc.), cryptobanks allow users to deposit and withdraw funds in fiat currency, use bank cards, Apple Pay, SEPA, or SWIFT-transfers.KYC/AML- modules

To comply with legal requirements, especially in the EU and the USA, customer identification (KYC) and anti money laundering (AML) systems are being integrated into cryptobank, for example, using SumSub, Onfido, Chainalysis. Anti money laundering measures are essential for preventing financial crimes and ensuring that crypto banks adhere to regulatory compliance frameworks.Functions DeFi/CeFi

Depending on the model, the platform may offer, leveraging decentralized finance (DeFi) to enable cryptobanks to provide innovative financial products without intermediaries:- Deposits and interest-bearing accounts (based on CeFi or DeFi)

- Lending secured by crypto assets

- Cryptocurrency cards with cashback and instant conversion

Mobile and web application

The interface through which users access the cryptobank functionality is as close as possible to traditional online banking, but with enhanced crypto capabilities.How does Trustee Plus work?

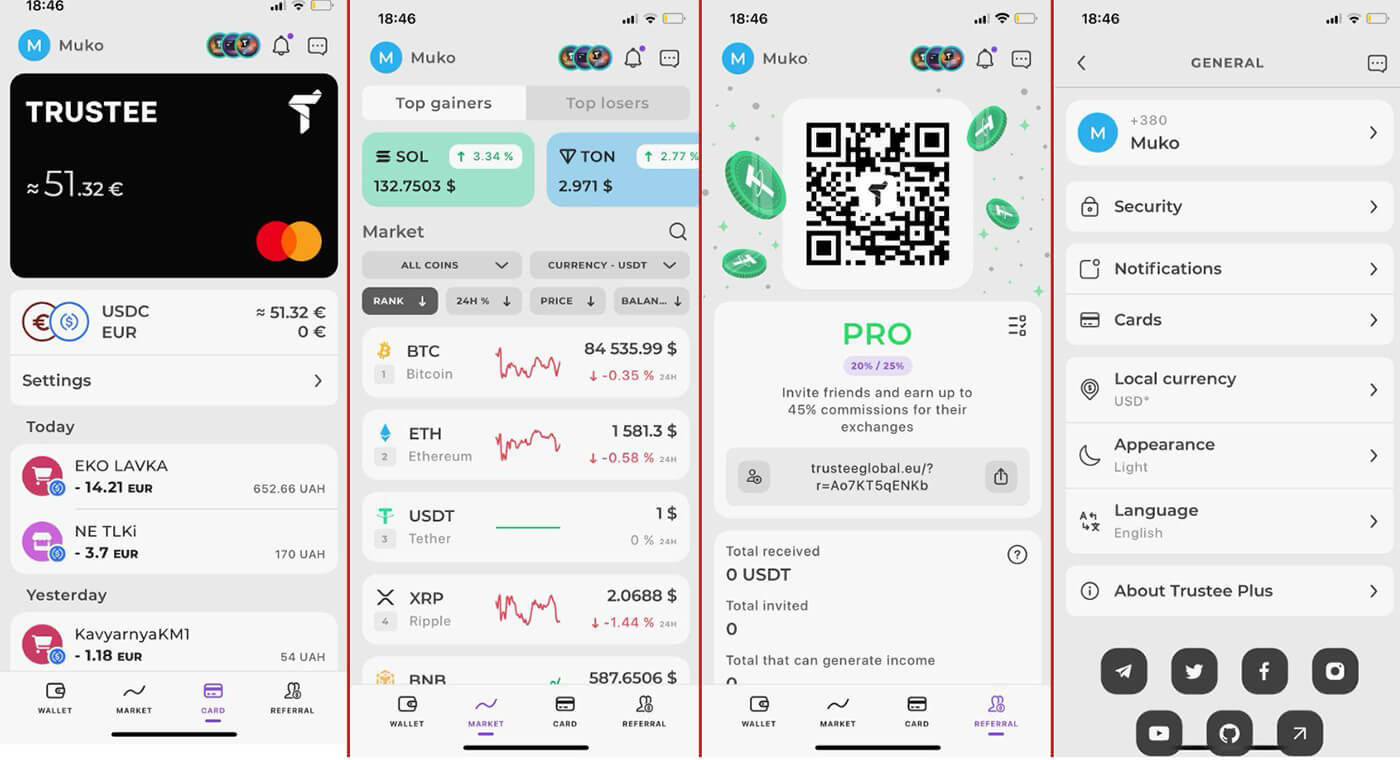

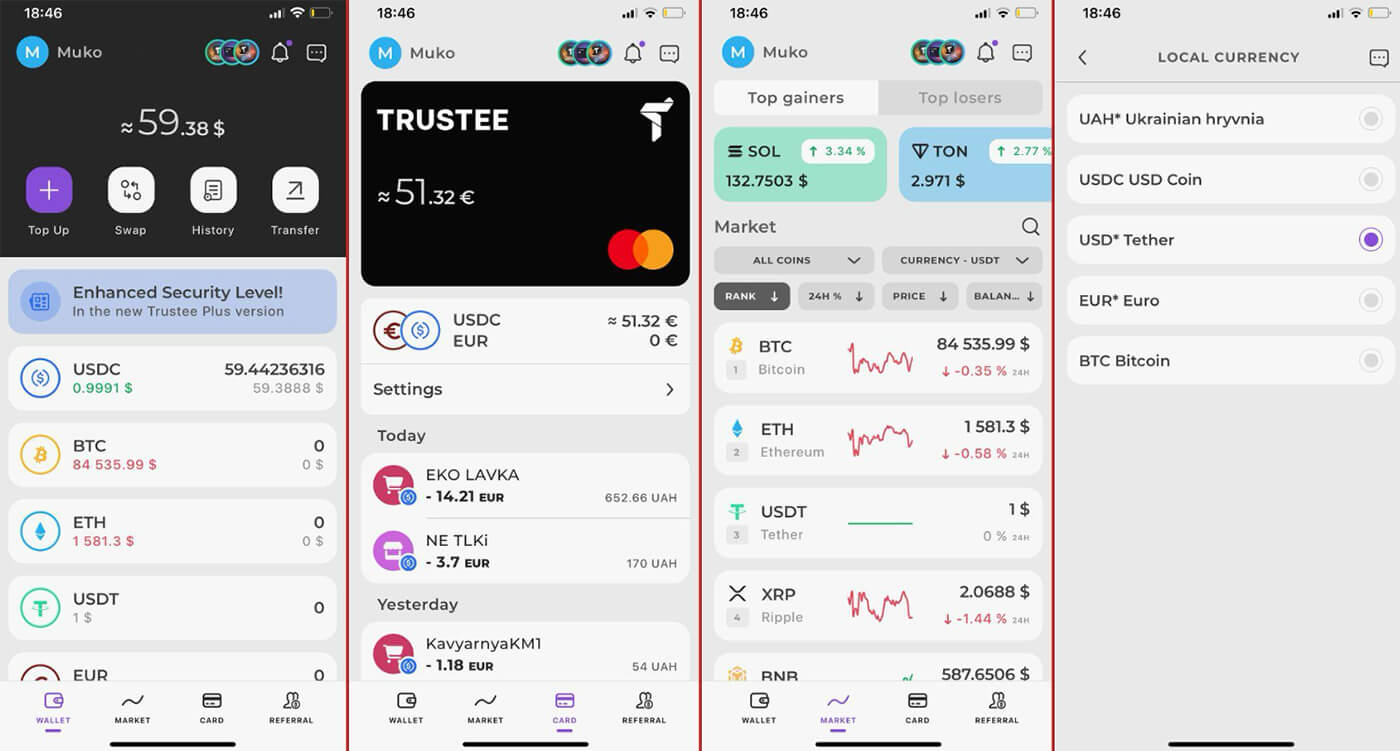

Trustee Plus — one of the leading crypto banks in the CIS and Europe, offering a convenient platform for managing digital assets with deep integration of fiat and cryptocurrency transactions.

Trustee Plus is actively developing as an «all-in-one» platform, offering users access to the cryptocurrency market without having to switch between different applications. The functions of storage, exchange, purchase, withdrawal and P2P trading are combined in one interface, which makes the service convenient for both beginners and experienced investors.

The platform provides competitive rates through the use of an exchange aggregator that automatically selects the best price among the connected partners. This allows users to get more favorable terms without manually comparing offers on external exchanges.

That's how his job works:

- Registration and verification: the user goes through the KYC procedure directly in the mobile application. After verification, access to the purchase of cryptocurrencies from a bank card, P2P and other operations open.

- Multi-currency wallet: Trustee Plus supports BTC, ETH, USDT, TON, BNB and dozens of other assets. The application implements a non-custodial wallet: the private keys remain with the user, but all the functions of a classic bank are available.

- Exchange and purchase: The platform is integrated with liquidity aggregators and fiat gateways, allowing transactions to be carried out quickly and at the best market rates. The user can buy cryptocurrency from the card, exchange it for other assets, withdraw it to a bank account or a crypto wallet.

- P2P platform: Trustee Plus provides a secure and regulated environment for buying and selling cryptocurrencies between users with automatic funds blocking until the transaction is completed.

- Investment products: Clients can receive passive income from staking or use third-party DeFi products integrated into the application.

- Fiat transactions: Trustee Plus offers users the ability to store funds in fiat currencies, as well as access to a payment card with the ability to make payments in cryptocurrency and cashback.

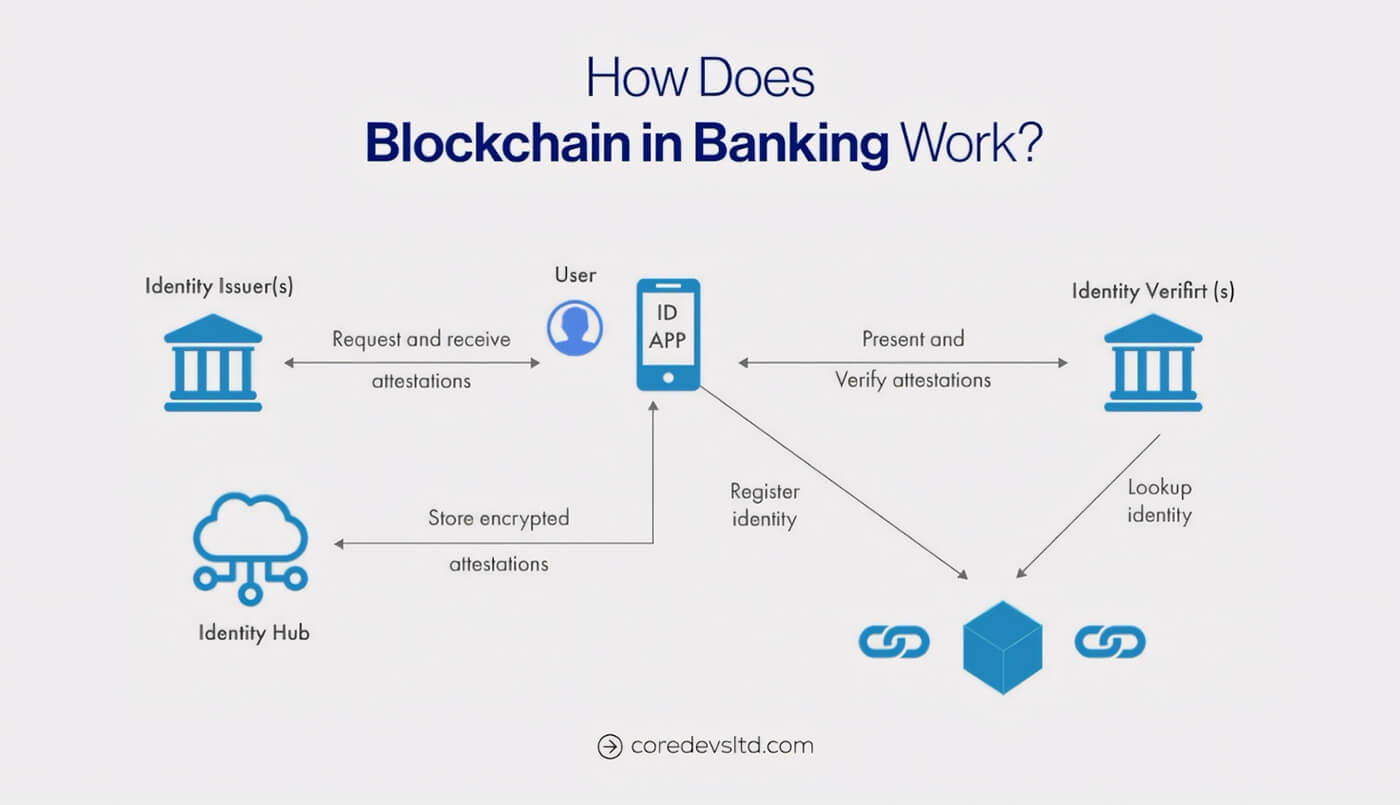

What Blockchain Do Crypto Banks Use?

Choosing a blockchain — one of the key factors in creating a cryptobank. The right choice of platform depends on the speed and cost of transactions, the level of security, scalability, as well as access to DeFi infrastructures, NFT protocols, CBDC integrations and other Web3 services. Advanced technology underpins the reliability and innovation of modern crypto banking platforms, making it essential to select a blockchain that leverages the latest advancements.Understanding the features of blockchains helps to create reliable and efficient cryptobanking platforms that can evolve along with the growing demands of users and the market.

Below is a list with an analysis of the most popular blockchains for cryptobanks:

Access to real time market data is a key advantage for trading and investment-focused cryptobanks, enabling timely decision-making and improved performance. When considering scalability, it is crucial to choose a scalable solution that can handle increasing transaction volumes and user growth efficiently.

1. Ethereum

Ethereum — main choice for cryptobanks working with DeFi infrastructure, tokenized assets and staking. Thanks to the support of smart contracts and high liquidity, the platform is widely used for custody solutions, lending and digital asset management.- Advantages:

- The most developed DeFi ecosystem

- Wide protocol support

- High security

- Disadvantages:

- High fees, especially during peak periods

- Relatively low speed (up to 15 transactions per second)

2. BNB Chain

BNB Chain is suitable for cryptobanks aimed at the mass user: for P2P exchanges, in-game payments and other operations requiring high speed and low cost. It is often used for debit cards and cashback services.- Advantages:

- Low commissions

- High throughput

- Support for the Ethereum Virtual Machine (EVM)

- Disadvantages:

- Centralization

- Strong dependence on Binance

3. Polygon

Polygon (POS) is ideal for cryptobanks focused on everyday transactions, micropayments, and Web3 functions. It is especially popular among NFT applications and platforms with high user activity.- Advantages:

- Low commissions

- Compatibility with Ethereum

- Support for zk-technologies

- Disadvantages:

- Partial centralization

- Problems with scaling under high load

4. Solana

Solana is used in cryptobanks offering instant transfers, payment cards, and interfaces that require high speed. It is also used in mobile applications and retail payment solutions.- Advantages:

- Very high speed (up to 65,000 transactions per second)

- Low fees

- Disadvantages:

- A complicated architecture

- There have been network failures in the past

5. TON

TON is chosen by cryptobanks targeted at the Telegram audience. It is ideal for P2P wallets, Telegram bot integrations, Web3 superapps, and custom financial mini-applications.- Advantages:

- Flexible architecture

- Excellent integration with Telegram

- High transaction speed

- Disadvantages:

- The infrastructure is still under development

- Weak DeFi-ecosystem

6. StarkNet

StarkNet is often used in cryptobanks as a Layer-2 solution for Ethereum, providing fast and cheap transactions while maintaining a high level of security. Suitable for custodial solutions and confidential DeFi products.- Advantages:

- Security due to Zero-knowledge evidence

- High scalability

- Compatibility with EVM via the Cairo language

- Disadvantages:

- The complexity of development

- The network is still new and developing

7. Tron

Tron is suitable for cryptobanks with a focus on international transfers, especially in countries with limited access to traditional banking services. It is most often used for USDT and other stable assets.- Advantages:

- Almost zero fees

- High transaction speed

- It is popular in Asian countries

- Disadvantages:

- Low level of decentralization

- Limited DeFi-landscape

8. Avalanche

Avalanche is suitable for cryptobanks working with institutional clients or complex DeFi products. The ability to create your own Subnets makes it a flexible tool for custom financial solutions.- Advantages:

- High speed

- Flexible architecture with the ability to create a Subnet

- EVM compatibility

- Disadvantages:

- More complex integration

- Fewer popular dApps

9. Bitcoin (through Lightning Network)

Bitcoin is used by cryptobanks to store BTC and instant P2P transfers using Lightning-networks. This is relevant for banking products with a focus on bitcoin and long-term investments.- Advantages:

- High reliability and liquidity of Bitcoin

- Lightning Network provides instant transactions

- Disadvantages:

- Limited functionality of smart contracts

- More complex implementation in applications

10. Algorand

Algorand is promising for cryptobanks working with the corporate sector, government digital currencies (CBDC) and institutional investments. The PoS algorithm ensures environmental friendliness and stability of operations.- Advantages:

- High speed

- Low commissions

- Energy-efficient consensus algorithm Pure Proof-of-Stake

- Disadvantages:

- Limited number of popular dApps

- Low recognition in the global market

Why choosing a blockchain is Important for a cryptobank:

- Speed and scalability For cryptobanks with a large number of micropayments, it is critically important to support tens of thousands of transactions per second. Here the advantage is given Solana, Polygon and BNB Chain.

- Cost of operations. High fees (for example, in Ethereum) make it less profitable for mass use, especially for small transfers. Therefore, Layer 2 solutions or alternative blockchains are often chosen.

- DeFi-integration. Platforms with a rich DeFi infrastructure allow cryptobanks to offer profitable products (staking, pharming, loans), which increases the value of the service.

- The level of decentralization. For banks operating in jurisdictions with high regulatory oversight, it may be important to choose networks with proven decentralization, such as Ethereum or Algorand.

- Combined architecture. Many cryptobanks use a multi-blockchain infrastructure: for example, the main logic works through Ethereum/BNB, micropayments — through Tron or Polygon, and tokenization and staking — through Solana or TON. Integrating with traditional financial systems in such architectures enables seamless transactions and spending between crypto assets and conventional banking, bridging digital assets with established financial infrastructure.

How to Build Own Crypto Bank?

Creating a cryptobank — is a complex process that requires not only technical competence, but also deep study of business logic, legal nuances and user experience. Crypto friendly bank development is crucial to support digital assets and seamless blockchain integration in modern financial services.Such a product must be secure, scalable, and comply with regulatory requirements. Crypto friendly banking solutions play a key role in providing secure and reliable services tailored for crypto users. Adherence to regulatory frameworks is essential for legal operation and market acceptance, while regulatory compliance must be maintained throughout the development process. Implementing security measures and robust security measures, such as encryption and multi-factor authentication, is vital to protect user data and funds.

Below we will look at the key stages of the development of a crypto banking application.

1. Cryptobank architecture development

At the first stage, it is important to correctly design the structure of the future product: how the modules will interact with each other, what services will be required, and what external integrations should be provided. Architectural errors can lead to vulnerabilities, scaling issues, or limited functionality in the future.- The business model is being determined: multicurrency wallet, crypto cards, DeFi functions, purchase/sale of cryptocurrencies, staking. At this stage, it is also important to plan for the integration of advanced features to enhance the platform's capabilities.

- The architecture of the components is being created: frontend, backend, databases, API, and blockchain nodes.

- The approach to storage is chosen: custodial (via MPC, HSM) or custodial (via a seed phrase and local encryption).

- Issues of scalability, fault tolerance and updatability are being worked out.

2. Choosing a blockchain and a smart-contract platform

Choosing a blockchain infrastructure — one of the strategically important points when creating a cryptobank. Transaction fees, transaction processing speed, user security, and integration capabilities with external services such as DeFi protocols, stablecoins, NFT platforms, and CBDC systems depend on it.- Ethereum remains the benchmark for creating complex DeFi products thanks to its vast ecosystem and mature developer However, high fees at times of network congestion make it not always the optimal choice for mass payment services.

- Polygon and BNB Chain — popular solutions for low-cost and frequent They provide EVM compatibility, which makes it easy to transfer code from Ethereum without major reworking.

- Solana and TON They are suitable for applications where high bandwidth and minimal delays are required — for example, for instant transfers, integration of cryptographic cards or superapps.

- By relying on ZK-technologies (StarkNet, zkSync, Scroll), you can achieve not only high scalability, but also an increased level of user privacy — a critical aspect for some financial products.

- Avalanche and Algorand suitable for more specialized solutions, such as corporate finance or working with CBDCs and tokenized assets.

3. UX/UI-design and prototyping

The interface of a cryptobank should be not only beautiful, but also intuitive, especially for users who have not previously encountered Web3. Mistakes in UX can cost the client money, and the product — reputation.- User scenarios are analyzed: registration, KYC, transfers, exchange, bank card connection, etc.

- UX routes are being worked out taking into account the specifics of cryptotransactions (waiting for confirmations, commissions).

- Design layouts are created in Figma/Sketch, including dark and light themes.

- Prototypes are tested in focus groups.

4. Developing the backend part

The cryptobank's backend — is the «heart» of the system, ensuring stable and secure operation of all functions. It must process thousands of transactions per second, interact with blockchains, provide KYC and connect to external services.- The logic of creating and managing wallets and synchronizing balances is implemented.

- External API are integrated: exchange rates, AML/KYC providers, banks and exchangers.

- Task queues and transaction processing systems are configured.

- Languages are used: Node.js, Go, Rust; databases: PostgreSQL, Redis; queues: RabbitMQ, Kafka.

5. Frontend development (web and mobile client)

Frontend — this is the main link in the user's interaction with the system. It should be responsive, fast, and secure. It is also necessary to provide support for all modern devices.- Mobile applications are created in Flutter, React Native or native languages.

- Web applications are developed on React/Vue with the ability to connect Web3-wallets.

- Notifications, QR-payments, biometrics and multiaccount support are implemented.

- Special attention is paid to data protection, prevention of XSS, CSRF and other vulnerabilities.

6. Integration with the blockchain and deployment of smart contracts

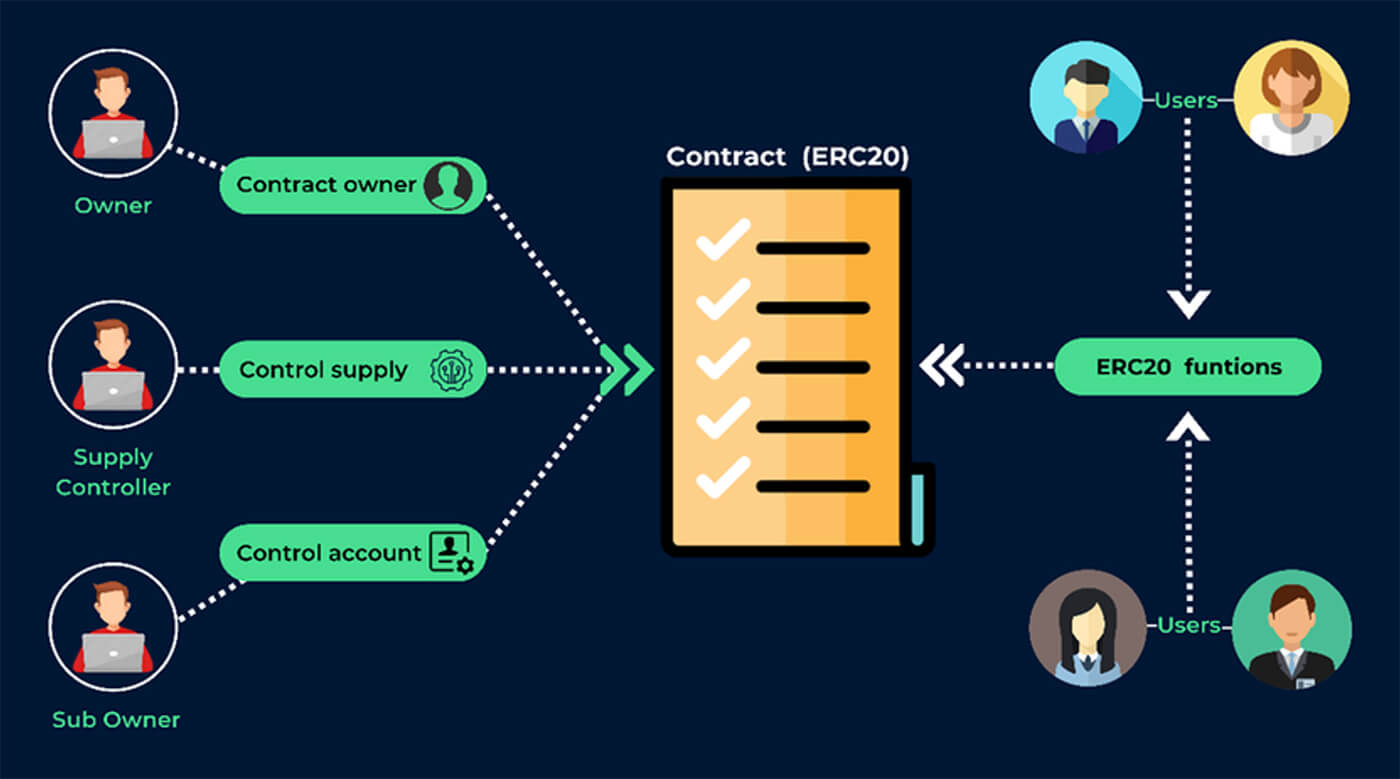

The stage of integration with the blockchain — the exit of the cryptobank from the testing mode for the real infrastructure. By this time, the blockchains and token standards used (ERC-20, BEP-20, SPL, etc.) should already be defined, as well as all necessary smart contracts prepared.- Smart contracts are being developed and tested (Solidity, Cairo, Rust).

- Code security is being audited (for example, through OpenZeppelin, MythX).

- Nodes and RPC services are deployed, and their fault tolerance is ensured.

- DeFi protocols and external liquid pools (Uniswap, Curve, PancakeSwap) are connected.

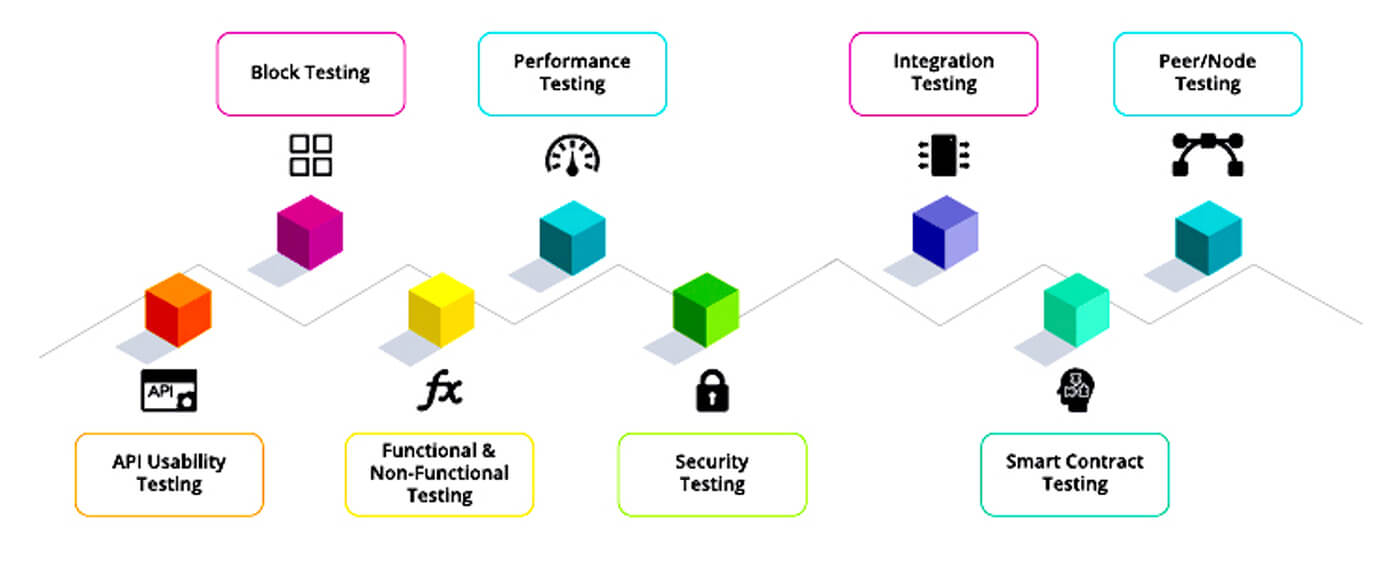

7. Testing and QA

Testing — key stage that determines the reliability, security and readiness of a cryptobank to enter the market. When working with real money and digital assets, any mistakes can lead to serious financial losses and reputation damage. Therefore, the QA (Quality Assurance) process must be comprehensive and systematic.Multi-level testing:

- Unit tests check the correctness of individual modules: smart contracts, API, deposit interest calculations, commission accrual mechanism, etc.

- Integration tests evaluate the interaction of various components of the platform — for example, the correctness of transaction processing between the frontend, backend and blockchain.

- End-to-end testing simulates the full user path — from registration and verification to opening a deposit account, obtaining a loan and withdrawing funds.

- Security audits (Smart Contract Audits) conducted by third-party companies to identify potential vulnerabilities in the code and architecture.

8. Legal aspects and licensing

The legal part — one of the most difficult and costly stages. Without legalization, it is impossible to fully connect bank accounts, cards and cooperate with payment systems. A cryptobank is recognized as a financial institution and must comply with relevant licensing and regulatory requirements.- A jurisdiction with suitable legislation is selected: Estonia, Lithuania, Switzerland, United Arab Emirates, Salvador.

- Licenses are obtained: EMI, VASP, MSB (depending on the country and model).

- KYC/AML-platforms (SumSub, Veriff) are integrated.

- Legal documents are being prepared: Terms of Use, Privacy Policy, KYC/AML Policy.

| Jurisdiction | Advantages | Features for cryptobanks |

| Switzerland | Clear crypto regulation, licenses FINMA | Suitable for asset storage, DeFi and investment products |

| Liechtenstein | TVTG blockchain law, loyalty policy | Easy access to licenses, tokenization support |

| Singapore | Transparent MAS rules, well-developed fintech industry | An excellent choice for hybrid solutions CeFi+DeFi |

| Estonia | Fast license issuance VASP, digital economy | Suitable for crypto payments and multi-currency wallets |

| United Arab Emirates (Dubai, Abu Dhabi) | Proactive regulation (VARA, ADGM) | Ideal for scaling international projects |

| Salvador | Bitcoin — official currency | The ability to integrate BTC into the infrastructure |

| Gibraltar | Regulated area for crypto companies | It is popular among crypto exchanges and banking platforms |

9. Launch, support and scaling

Launching a cryptobank — this is not the end point, but the beginning of the product lifecycle. Launching crypto banks is crucial for expanding access to digital financial services and reaching new markets. After entering the market, the most important tasks are to ensure the stable operation of the platform, the constant development of its functionality and strategic scaling.

Deployment and infrastructure:

After passing all the testing stages, the cryptobank is deployed on a highly reliable cloud infrastructure (for example, AWS, Google Cloud, Hetzner). Solutions that provide scalability, backup, and fault tolerance are selected. If necessary, containerization (Docker, Kubernetes) is used for flexible updates.

An important aspect is the constant work on protecting user data and funds.

- Regular software patches and updates;

- Vulnerability monitoring;

- Implementation of anti-fraud systems;

- Multi-factor authentication (MFA) and biometric protection.

The platform must evolve:

- Connection of new blockchains (for example, integration of Layer 2 solutions or networks such as Aptos, Sui);

- Adding support for new tokens, stablecoins, and national currencies;

- Geographical expansion — launch of localizations for countries with promising crypto markets (for example, Latin America, Southeast Asia);

- Legalization in new jurisdictions to increase the number of users.

A clear roadmap of development is being formed for 6-12 months ahead. Key milestones are included: the integration of new financial services (for example, brokerage services), partnerships with traditional banks, the creation of their own investment products, staking pools or NFT-marketplaces.

Crypto Banking Solutions

Cryptobanks, like any other digital financial platforms, can choose one of two approaches to create their service: using ready-made solutions based on the White Label model or developing a unique system from scratch based on ready-made solutions.A white label banking platform enables rapid deployment of branded crypto banking services, allowing financial institutions and crypto businesses to quickly enter the market. A digital banking solution integrates various financial services, including crypto transactions, merchant payments, and often a merchant payment gateway to facilitate global payments. Digital banking solutions are essential for modern financial platforms, providing seamless, secure, and innovative services.

Crypto digital banking solutions leverage blockchain technology to offer a wide range of services, supporting both crypto and fiat currencies for maximum flexibility. These solutions enable the delivery of digital financial services tailored to customer needs, helping businesses attract and retain users in a competitive landscape.

Both approaches have their advantages and disadvantages, and the choice depends on the business goals, budget, and time frame of the project.

1. Ready-made solution White Label

What is a White Label?

White Label crypto bank — a ready-made solution provided by a third-party developer, which can be adapted to the needs of a specific client. In the context of cryptobanks, it can be a platform that already includes all the necessary tools for operation: wallets for cryptocurrencies, deposits, loans, currency exchange and other banking services. The main principle of White Label is that the client can implement these solutions into their business processes with minimal effort and without significant development costs.

Advantages:

- Fast development and launch: Unlike building a system from scratch, White Label solutions can reduce development time, as many functions have already been implemented and tested.

- Low initial costs: Using a ready-made solution is significantly cheaper compared to full-fledged custom development.

- Tested and secure infrastructure: Ready-made solutions have often already been tested on real users, providing a higher level of security and reliability.

- Less risk: No need to develop everything from scratch reduces technical risks.

Disadvantages:

- Limited Flexibility: White Label solutions provide limited customization options, which can be a problem if something unique is needed.

- Vendor Dependency: The customer is completely dependent on the solution developer for updates, fixes, and further changes.

- Limited differentiation: Such platforms are often used by other cryptobanks, which makes it difficult to create a unique image.

2. Developing a project based on a ready-made solution

For larger and more scalable cryptobanks that strive to provide unique services with a high degree of customization and integration with other services, the best option may be to develop a project based on a ready-made solution. In this case, the company uses a ready-made platform as the basis and modifies it according to specific requirements.Unlike using a White Label solution «as is», in this case the company develops its own unique functions and integrates additional services such as custom smart contracts, special staking mechanisms, loans or complex DeFi-protocols.

Advantages:

- Higher customization: The ability to deeply customize all aspects of the system, including design, functionality, and integration.

- Fewer restrictions: The platform can be customized to meet unique business needs, including support for specific cryptocurrencies or non-standard financial transactions.

- Expansion opportunities: Such solutions are easier to scale and adapt to new functions and markets.

Disadvantages:

- Long development time: The development and testing process can take from several months to a year, depending on the complexity of the system.

- High cost: Creating a unique product, even if a basic solution is used, requires large investments in development and testing.

- Technical risks: We need a highly qualified development team to create a high-quality and secure solution.

How Much Does It Cost to Develop a Crypto Banking App?

The development of a cryptobank depends on its scale and functionality. The crypto banking industry is rapidly growing, which influences both development costs and market competition. Compared to the traditional banking sector, the cost structure for cryptobank development can differ significantly due to the use of blockchain technology and digital assets.The estimated cost of development is shown below, depending on the project level:

- The small project

- Cost: $20,000 – $40,000

- Development time: 4-6 months. Small projects usually have basic functions such as cryptocurrency wallets, exchanges, and simple deposits. This solution is ideal for startups or small crypto banks.

- The medium project

- Cost: $40,000 – $80,000

- Development time: 6-9 months. Medium-sized projects include additional features such as integration with multiple blockchains, lending, staking, and comprehensive security features.

- The major project

- Cost: $80,000 – $160,000

- Development time: from 9 months or more. Major projects cover a variety of functions, including extensive customization options, support for multiple blockchains, scalability, and provision of complex financial services such as DeFi, complex loans, and innovative smart contracts.

Estimated costs after the launch of the cryptobank

| Expense category | Description | Estimated cost (per year) |

| User support | Customer service, technical support, chabot’s. | $30,000 – $50,000 |

| Updates and security | Regular system updates, bug fixes, security patches, and audits. | $20,000 – $40,000 |

| Infrastructure (cloud servers) | Data storage platform, databases, cloud services (for example, AWS, GCP). | $50,000 – $100,000 |

| Legal and regulatory expenses | Compliance with legislation, licensing, and auditing. | $10,000 – $30,000 |

| Marketing and promotion | Advertising campaigns, user engagement, and partnerships. | $20,000 – $50,000 |

| Scaling and optimization | Development of infrastructure for scaling, improvement of speed and security. | $30,000 – $70,000 |

Benefits of Owning a Crypto Bank

Owning a crypto bank opens the door to a wealth of opportunities in the rapidly expanding digital finance landscape. Crypto banks can tap into new and growing markets, unlocking additional revenue streams and enhancing their competitive edge. By offering a diverse range of services—including crypto trading, lending, and seamless payment solutions—crypto banks attract a new generation of customers seeking innovative, secure, and user-centric financial products.The integration of blockchain technology ensures that all financial transactions are secure, transparent, and efficient, fostering greater trust and confidence among users. Additionally, crypto banks can deliver personalized banking tools, support for multiple currencies, and comprehensive banking functionalities that cater to both individuals and businesses.

This multi currency support and flexibility make crypto banks an appealing choice for those looking for a modern, reliable, and efficient banking solution. Ultimately, owning a crypto bank not only streamlines business operations and reduces costs but also positions organizations to thrive in the evolving world of digital assets and financial technology.

FAQ

What kind of blockchain do cryptobanks use?

Crypto banking app can use different blockchain platforms depending on the purposes and type of services offered. The most commonly used blockchains include Ethereum, which is ideal for smart contracts and DeFi-applications, as well as Binance Smart Chain (BSC) and Polygon — with lower fees and high throughput, which is ideal for crypto payments and bulk transactions. Solana and Avalanche are popular for high-speed operations and real-time applications. Also, blockchains such as StarkNet and zkSync support solutions based on zero-knowledge proofs to ensure scalability and privacy.

What kind of cryptocurrency do banks use?

Crypto banking apps usually use Bitcoin (BTC) and Ethereum (ETH). as the main cryptocurrencies for storing and transferring funds, as they are the most liquid and recognized in the world. Stablecoins such as USDC, DAI, and Tether (USDT) are also widely used, which provide price stability and can be used for exchange, lending, and deposits. In some cases, cryptobanks also support less popular altcoins or their own tokens for specific services and functions, for example, for staking or use within DeFi-protocols.

How do open own cryptobank?

Opening your own crypto bank app requires careful preparation and compliance with several key steps. First of all, it is necessary to choose a jurisdiction with favorable regulation of cryptocurrency transactions, such as Estonia, Switzerland or Singapore. After that, you should choose a suitable technology platform — can either develop the platform from scratch, or use a white label solution that allows you to launch the product faster. Next, it is important to obtain the appropriate licenses and be checked for compliance with regulatory standards. It is also necessary to integrate cryptocurrency wallets, payment gateways and DeFi-protocols to ensure transactions with cryptocurrencies. At the final stage, you should set up marketing and attract the first customers by offering attractive financial products.

What are the best cryptobanks right now?

Among the best applications for cryptocurrency banking are Revolut, SwissBorg, Crypto.com, and BlockFi. These platforms offer a wide range of services, from storing cryptocurrencies to exchanging, lending, and generating returns on deposits. Revolut is well known for its integration with fiat currencies and ease of use. SwissBorg attracts users with its flexibility in asset management using algorithmic solutions. Crypto.com and BlockFi are focusing on loan products and opportunities to generate returns from cryptocurrency assets. It is important to choose an application that meets your financial goals and security requirements, as cryptocurrencies require additional attention to asset protection.

How to ensure security in a cryptobank?

Security in a crypto banking app is a priority, as it works with digital assets that may be subject to hacking and fraud risks. To ensure security, it is important to use multi-level protection: multi-factor authentication (MFA) for users, data encryption both on the client side and on the server, as well as cold storage for storing large amounts of cryptocurrencies. It is also necessary to conduct regular security audits, test vulnerabilities using penetration testing, and integrate solutions to monitor suspicious activity and prevent fraudulent transactions.