Artificial intelligence (AI) has moved far beyond laboratory demonstrations and highly specialized applications. Today, it is being integrated on a massive scale into global technologies and products.

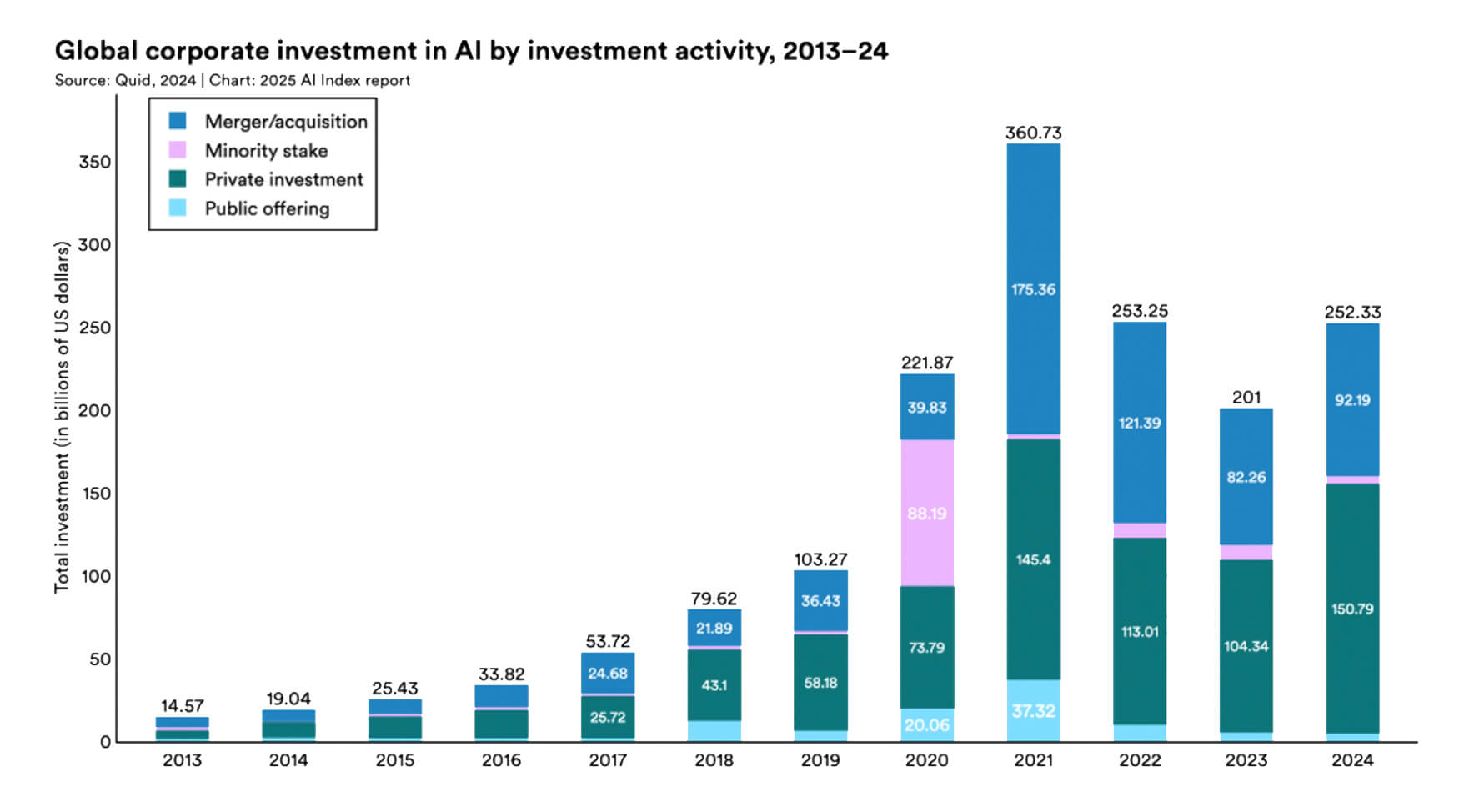

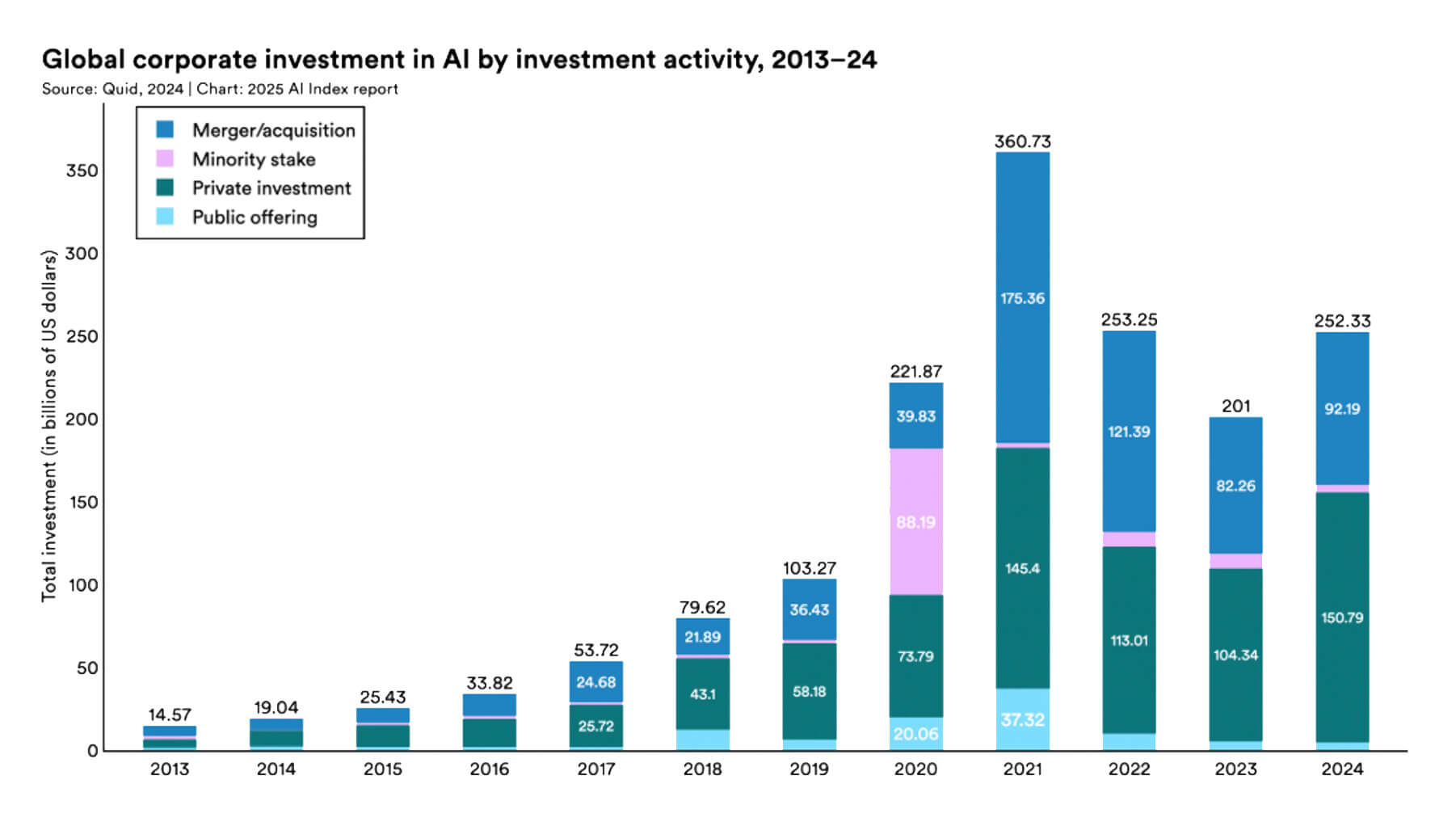

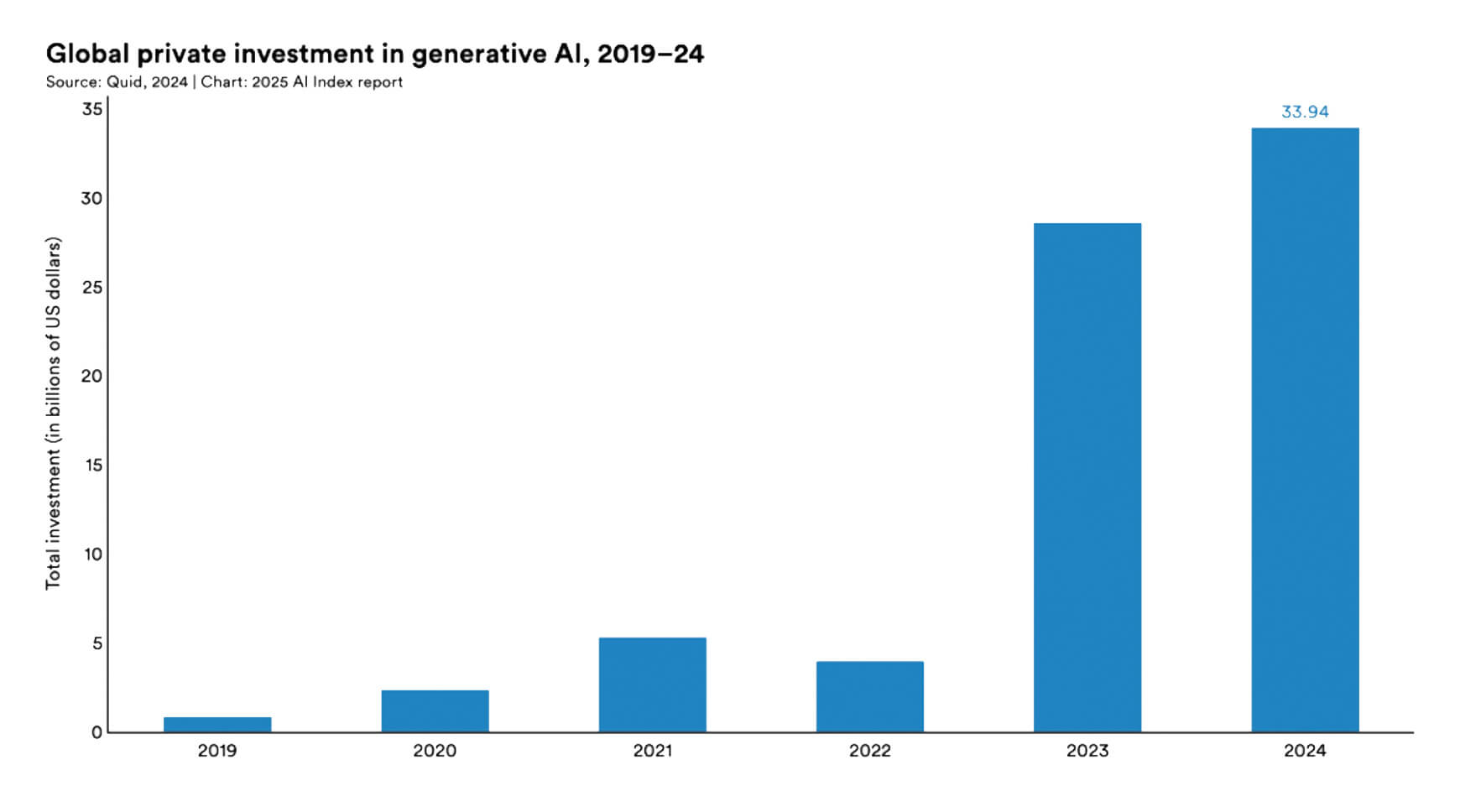

For businesses, AI is already becoming a strategic investment target: by the end of 2024, capital investments in artificial intelligence technologies amounted to $252.3 billion from corporate investors and $33.9 billion from private investors

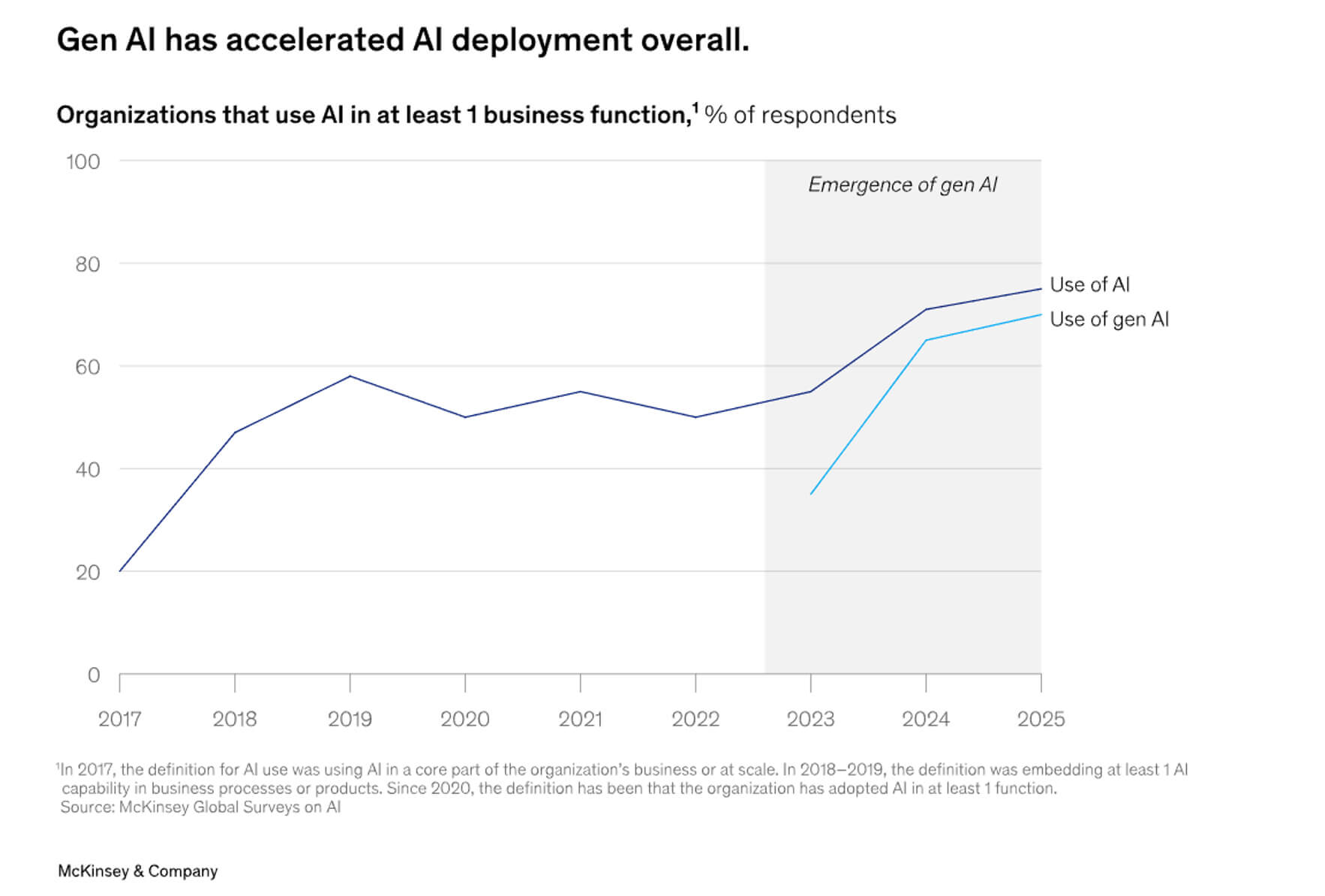

According to a report from HAI Stanford University, 78% of American and European organizations used AI in 2024, which indicates its growing popularity and widespread adoption in the corporate sector.

According to research by ELON University, 52% of the adult American population used services such as ChatGPT, Gemini, Claude, Copilot in 2025, making LLM (large language models) programs the most actively implemented in the world.

According to market analysis by McKinsey, 92% of companies will increase their investment in the AI sector over the next three years in order to move from pilot projects to large-scale results.

AI models and their performance

Over the current year, AI models, especially large language models (LLMs), have demonstrated active progress and technological improvements, and this trend will continue in 2026. They are rapidly adapting to various subject areas and integrating with new tasks through fine-tuning and retraining.The results of several benchmarks show that LLMs are not only increasing in size or computing power, but also improving in capabilities, especially in reasoning, programming, and problem solving.

According to a study by HAI Stanford University, between 2023 and 2024, AI systems demonstrated growth of 18.8% and 48.9% in the MMMU and GPQA benchmarks, respectively.

In 2024, performance indicators in the SWE-bench benchmark (software engineering tasks/real coding tasks) increased to 71.7% (in 2023, this indicator was at 4.4%).

A key trend this year is that many models are no longer simply universal. There is a growing trend toward specialization for specific tasks, industries, and contexts.

For example, OpenAI's o3 and o3-mini models are designed for more efficient analysis, code writing, and scientific problem solving. In particular, the o3 model scored 87.7% on the GPQA-Diamond benchmark (expert scientific questions) compared to lower scores from earlier models.

In the SWE-bench Verified benchmark (real information about issues on GitHub), o3 scored around 71.7% compared to much lower scores for earlier or less specialized models.

Models are expanding their context windows and multimodal inputs: for example, Llama 4 Scout/Maverick includes both image and text input, supports long context windows (1 million tokens, and in some cases more), and is adapted for multilingual and multimodal tasks. Such models are better suited for domain-specific applications (law, medicine, engineering, customer service, etc.) and are increasingly used in enterprise environments where general LLM performance is insufficient.

In 2026, the performance gap between different language models is expected to narrow as more market players gain access to more advanced computing and data.

Thus, GPT-4.1 provides approximately 21% higher encoding performance compared to GPT-4o and 27% higher performance compared to GPT-4.5.

According to OpenAI's internal reports, GPT-5 makes factual errors nearly 45% less often than the “old” versions of GPT-4 in a set of test queries.

Next year will see even more specialized models, and models trained in specific subject areas will become the norm. Hybrid training methods based on a base model with functional adjustments and retraining will become more optimized, reducing costs and increasing performance. The ability to work with longer contexts and multimodal data will also expand, allowing models to process larger documents, more complex types of input (e.g., video+text+audio), and maintain consistency during prolonged interactions.

AI agents and autonomy

AI agents are specialized software systems that plan, make decisions, and perform multi-step tasks with minimal human involvement. Today, they have moved from research demonstration projects to real corporate products and will be actively implemented in the coming years.In the US and European markets, such technologies have a wide range of applications:

- automation of sequences of actions;

- coordination of tools and management of end-to-end workflows in customer service, marketing, IT, and operations.

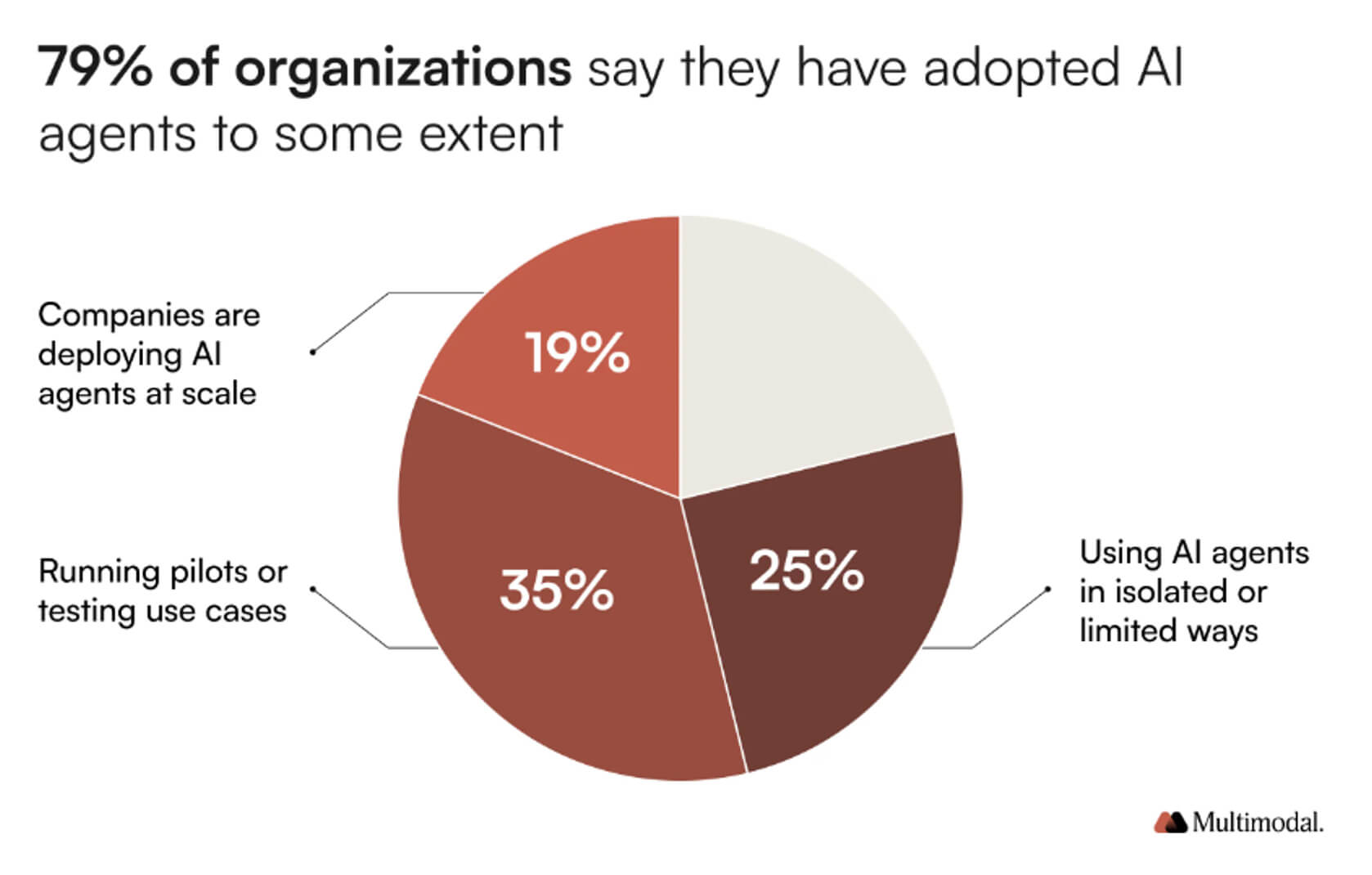

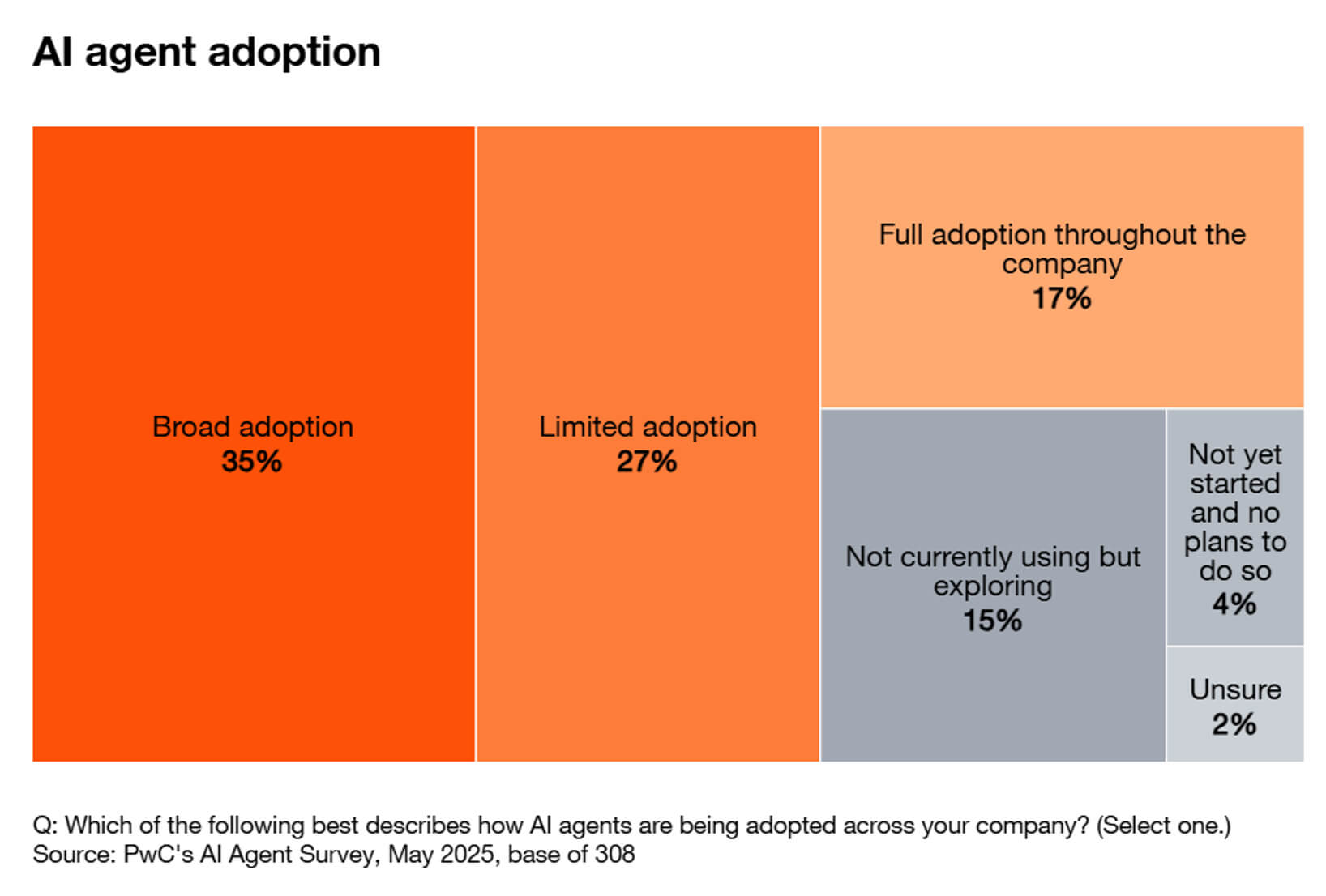

According to data obtained from industry surveys and analytics, up to 80% of companies already use AI agents in their operations and plan to expand their implementation next year.

Salesforce's Agentic Enterprise Index shows that employee interaction with AI agents grew by approximately 65% in the first half of 2025, while the volume of actions initiated by AI agents increased by approximately 76%. This indicator reflects not only the growth in the number of pilot projects, but also the scaling of operational use.

According to MarketsandMarkets, the AI agent market is valued at $7.8 billion and will grow to $52.6 billion by 2030.

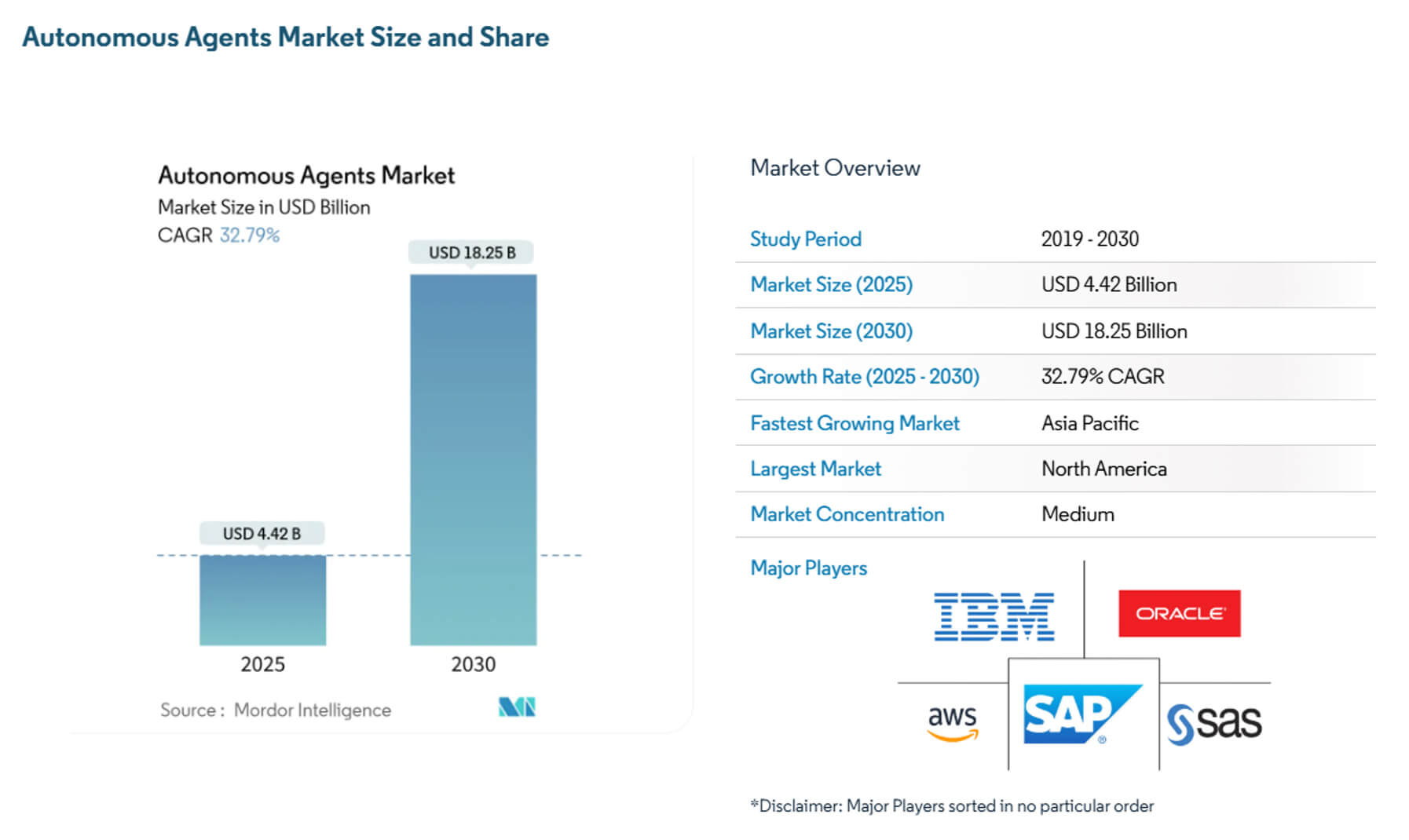

Mordor Intelligence experts have calculated the current market capitalization at $4.4 billion, with growth to $18.3 billion over the next five years.

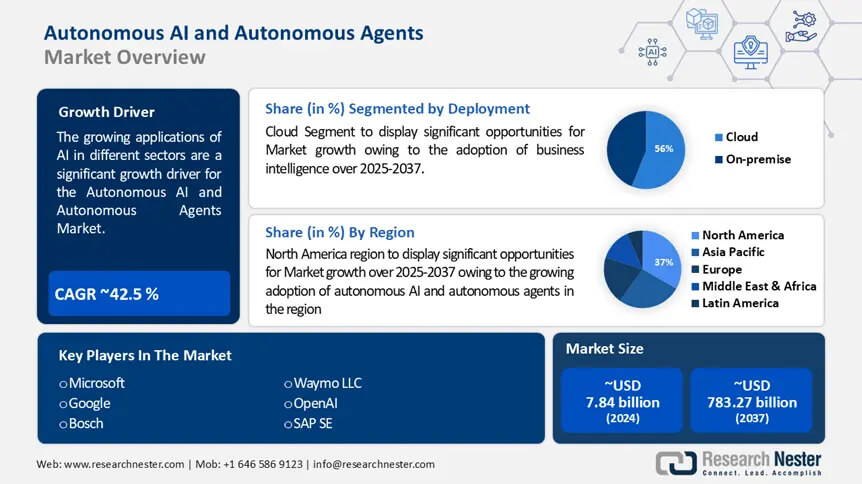

According to ResearchNester orecasts, the AI agent market capitalization is $8.6 billion and will grow to $263.9 billion over the next 10 years.

The use of AI-based agent systems has a wide range of applications:

- Customer service and support organization – agency systems can engage in dialogue, assess customer needs, send requests to back-end systems, and perform various actions, such as issuing loans, opening tickets, or planning deliveries, which significantly minimizes the human factor. Thus, as early as 2025, some banks piloted the use of their own AI agents to automate multi-step services and decision-making;

- Marketing and development operations – AI agents conduct campaign experiments, create creative briefs, segment audiences, and even run A/B tests across connected marketing stacks, allowing marketers to focus on strategy and creative direction;

- Software development and IT automation – AI agents automate sorting, run test suites, create tickets, and suggest or apply fixes. Preliminary tests show that agents reduce the average time it takes to resolve routine issues and speed up developers' workflows.

By 2026, a significant proportion of pilot projects will be specifically implemented in the finance, telecommunications, retail, and corporate IT sectors.

Language and generative AI

Key capabilities of generative artificial intelligence:- content creation – marketing agencies, media companies, and small business content managers use generative text tools to create blogs, product descriptions, social media posts, and advertising copy;

- Data synthesis and augmentation – when training ML models in areas with data shortages (healthcare, law, specialized sciences), synthetic data and augmented datasets created by generative models help reduce privacy concerns and improve performance.

- Translation and multilingual understanding – this is an effective aid in translation and cross-language natural language processing tasks.

- Multimodal generative AI combines text with images, audio, or video, enabling the application of artificial intelligence in design, virtual content creation, marketing campaigns using multimedia elements, and even creative work.

In 2026, generative AI and language models will continue to evolve rapidly, improving context understanding, creating higher-quality text, images, and video, and becoming more useful in real-world applications.

Below are key trends and predictions for 2026.

| Metric | Value/Rating | Source |

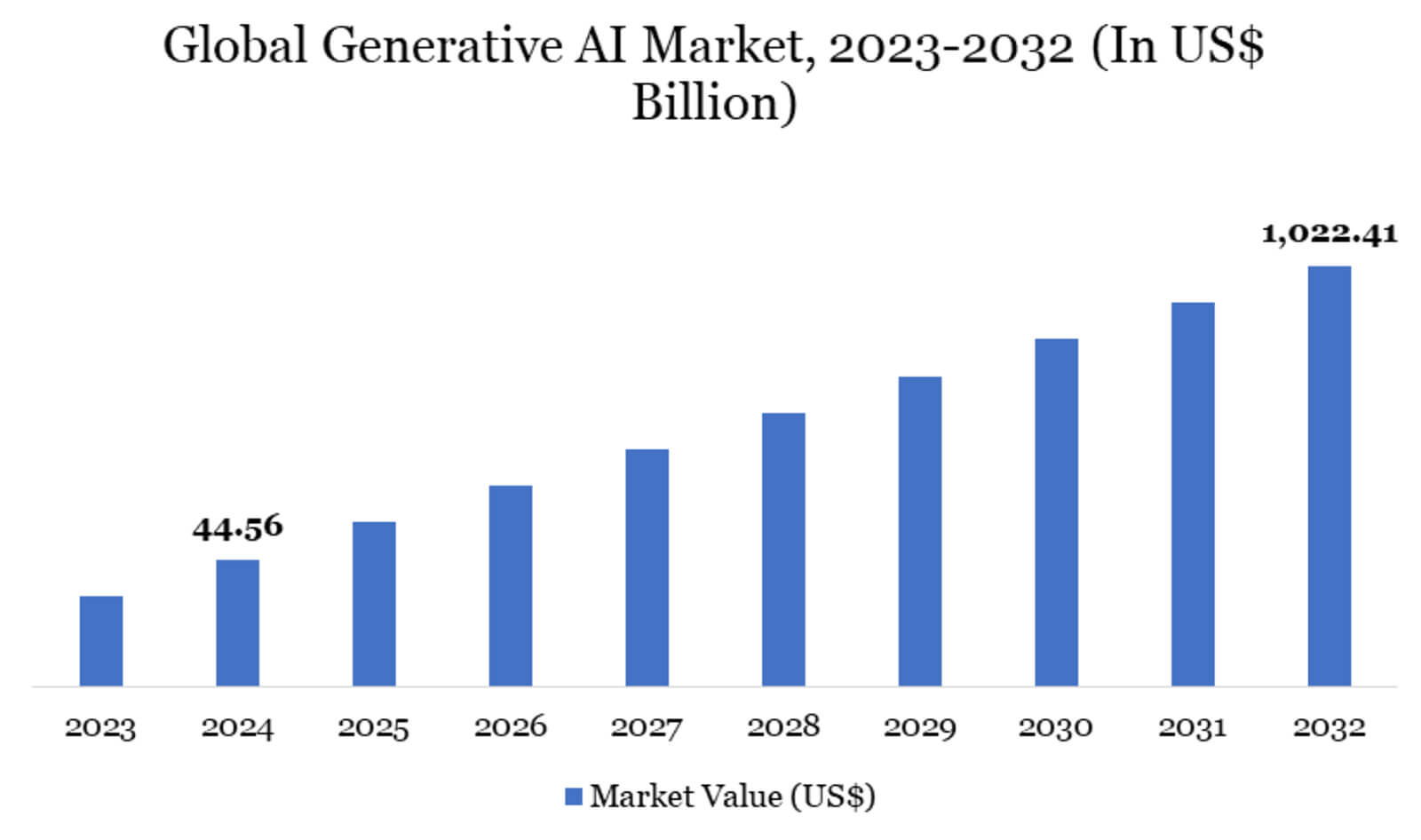

| Global Generative AI Market | $45.56 billion | Datamintelligence report: «Generative AI Market Size, Share, and Growth for 2025–2032» |

| Projected CAGR of the Global Generative AI Market (until 2032) | 47,5% | Datamintelligence report: «Size, Share, and Growth of the Generative AI Market for 2025–2032» |

| Estimated market size of generative AI in 2025 | $37.89 billion | Datamintelligence report: «51 statistics on generative AI for 2025» |

| Market share by geography | North America – 41% Europe – 28% Asia and the Pacific – 22% |

Datamintelligence report: «51 statistics on generative AI for 2025» |

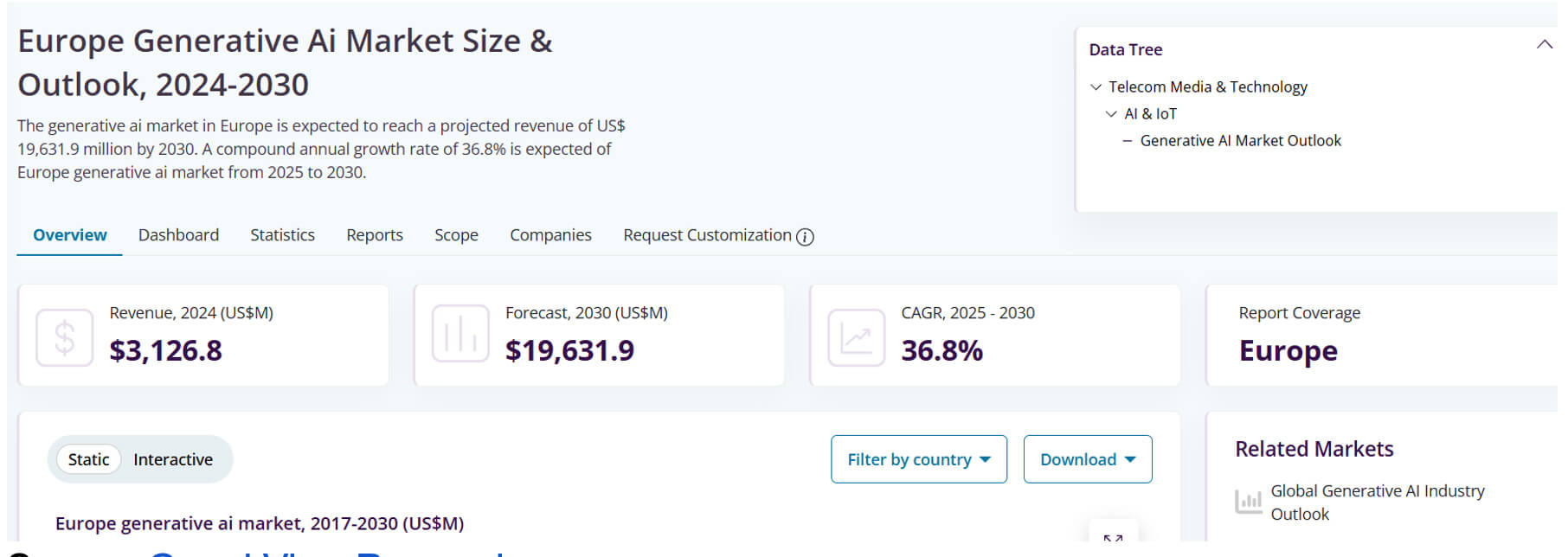

| Revenue from generative AI in Europe in 2024 | $3.13 billion | Grand View Research: The size and prospects of the European generative AI market |

| Compound annual growth rate of generative AI in Europe in 2024-2030 | 29,9% | Grand View Research: The size and prospects of the European generative AI market |

The data presented indicates both the high current level of technology use and adoption, as well as expectations for rapid growth in the coming decade. According to research forecasts, the scaling of generative AI will grow rapidly by 2032.

AI in everyday life

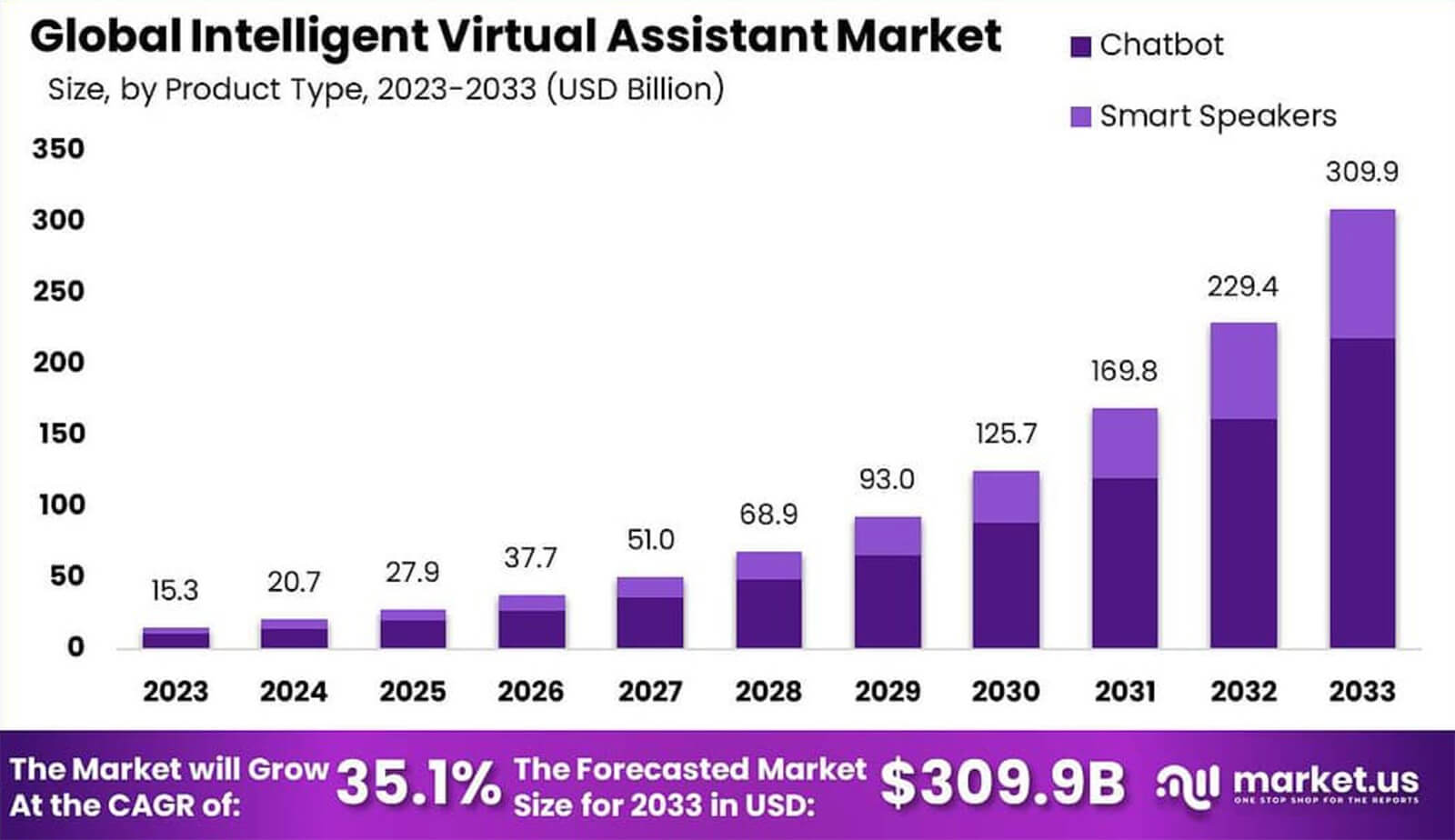

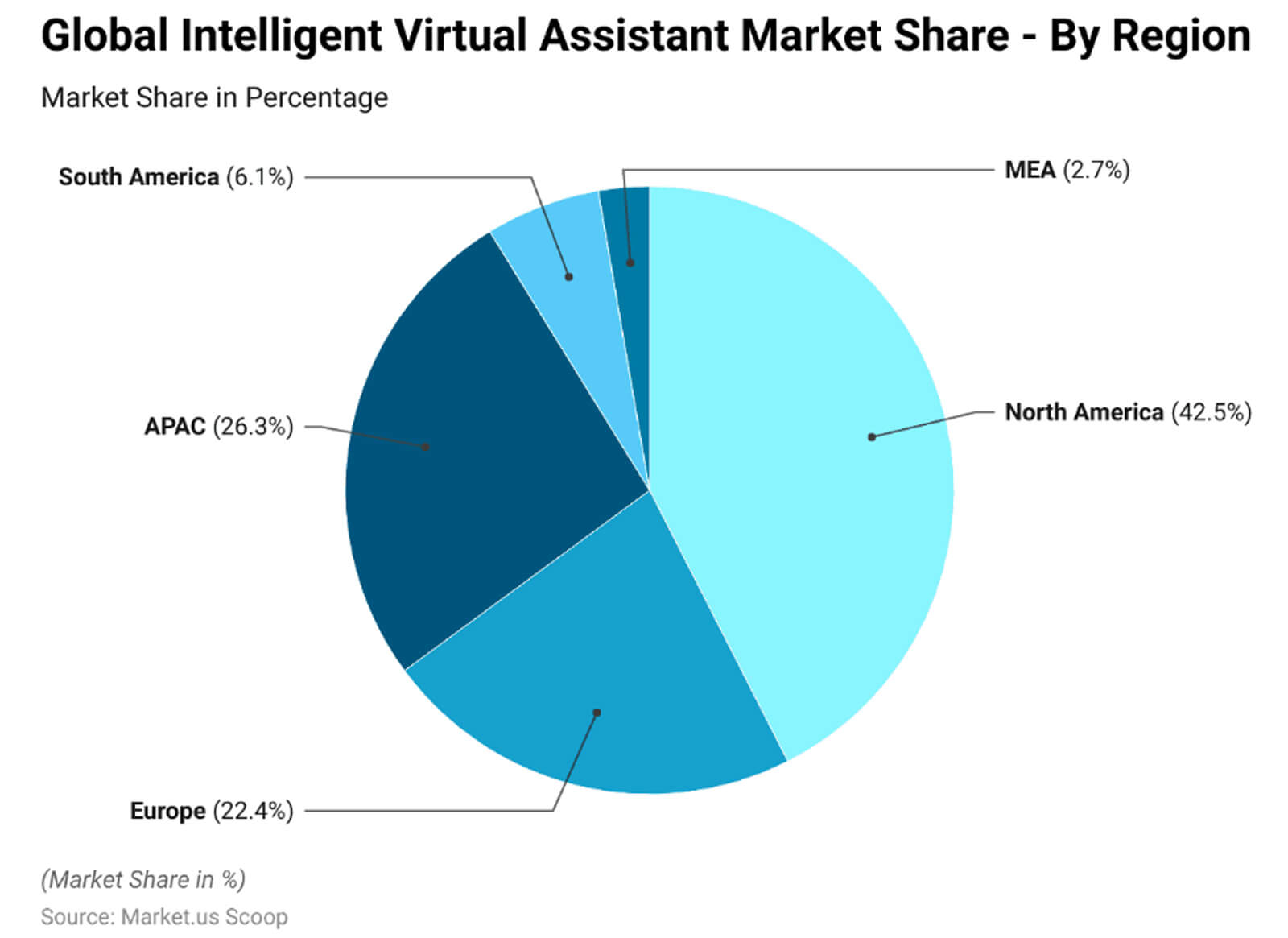

Artificial intelligence is rapidly becoming part of everyday life and a convenient feature of modernity. Technologies are being integrated into gadgets and home appliances, helping people make their daily lives more convenient and efficient.According to expert forecasts, the global market for intelligent virtual assistants will grow to $27.9 billion this year, with North America already accounting for almost 42.5% of that total.

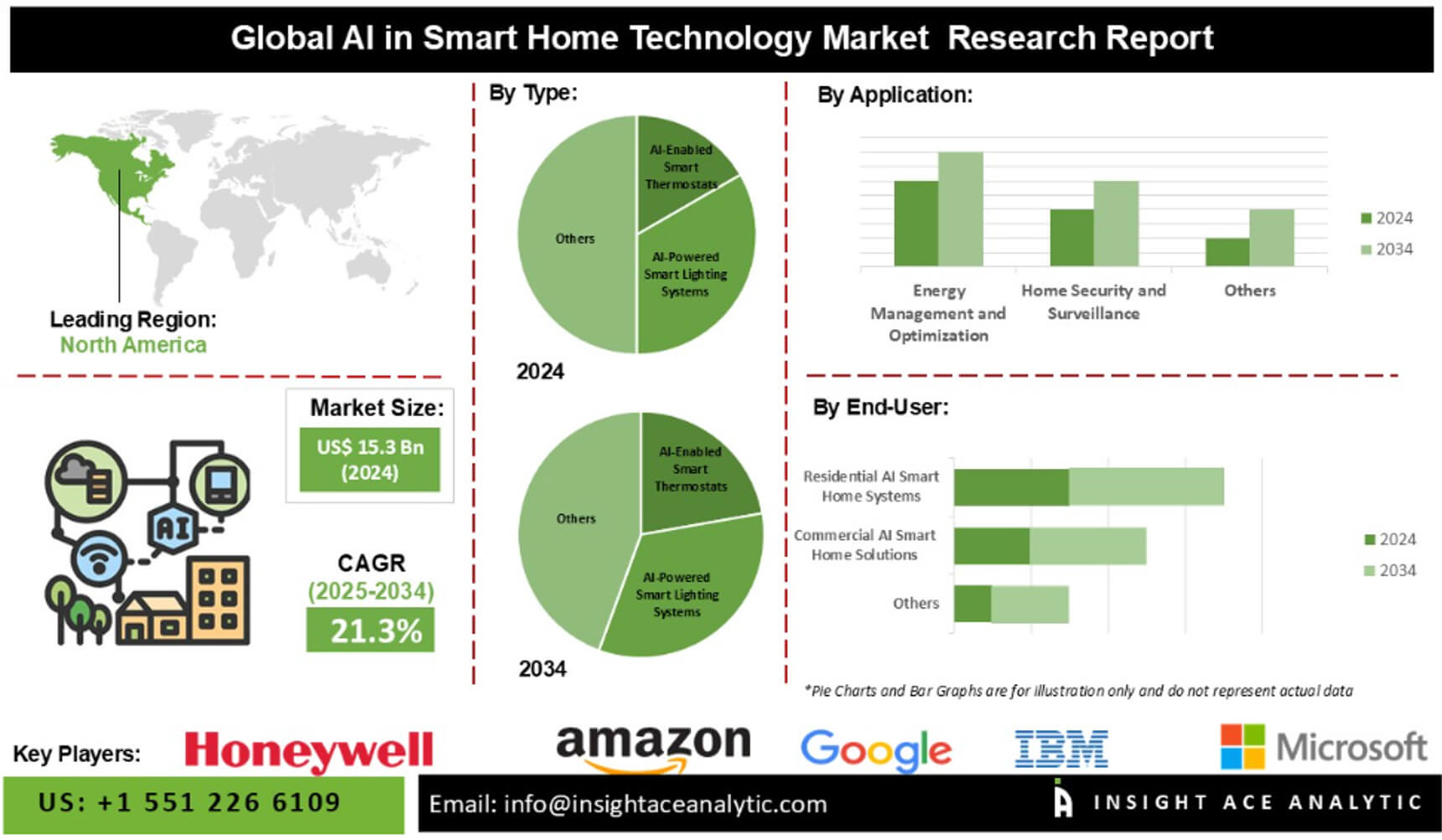

The AI segment in smart homes was worth $15.3 billion at the end of 2024, and by 2034, it will grow to $104.1 billion, with an expected average annual growth rate of 21.3%.

In 2025, 38% of US households already had smart video surveillance cameras installed, 33% had video intercoms, and 22% had smart locks.

According to Blueprism, 86% of healthcare organizations report widespread use of AI. For example, 12% of the adult US population report that their healthcare providers use artificial intelligence for diagnosis, treatment, and communication.

Areas and ways of using AI in everyday life:

- Virtual assistants in smartphones, tablets, car control, and home technology (Siri, Google Assistant, Alexa, etc.) – for many people, asking for directions, setting reminders, controlling smart lighting, or even finding a recipe with the help of AI is becoming commonplace. More than 110 million users in US regularly use assistants for everyday tasks;

- Smart homes—security cameras, video intercoms, smart locks, etc.—are becoming increasingly common and are now equipped with artificial intelligence. This not only improves automation, but also increases security and convenience, as well as saving energy;

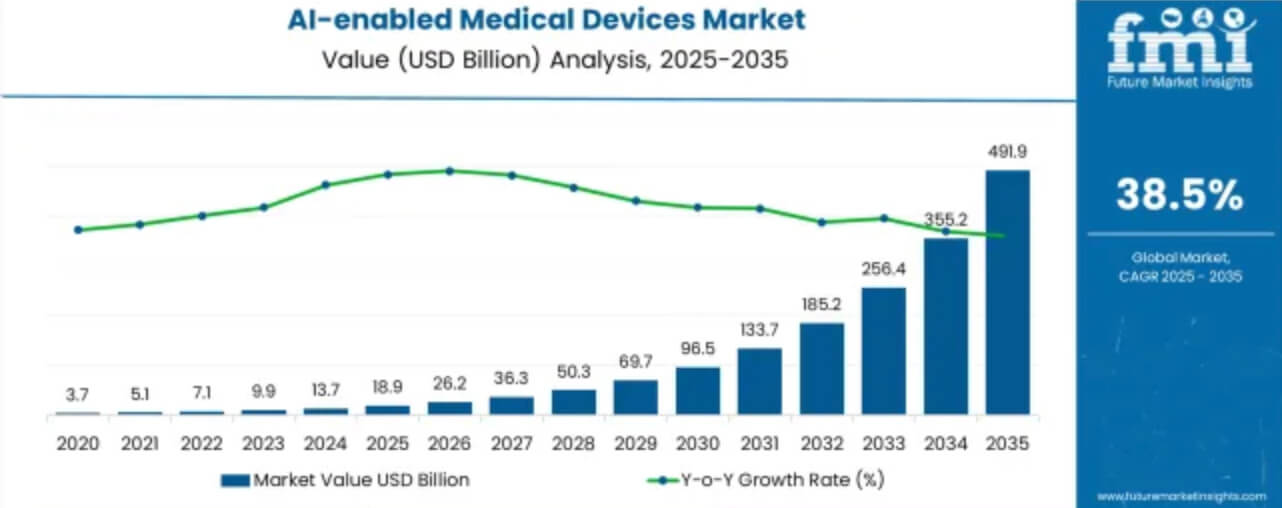

- AI-based medical devices (visualization, diagnostics, patient monitoring) – the market for AI-based medical devices will be worth around $18.9 billion in 2025 and is forecast to continue growing rapidly.

Companies use AI to automate routine tasks (such as planning and processing customer requests), freeing up employees to perform strategic tasks. In education, AI tools are used for tutoring, creating exercises, summarizing content, and assisting with language learning.

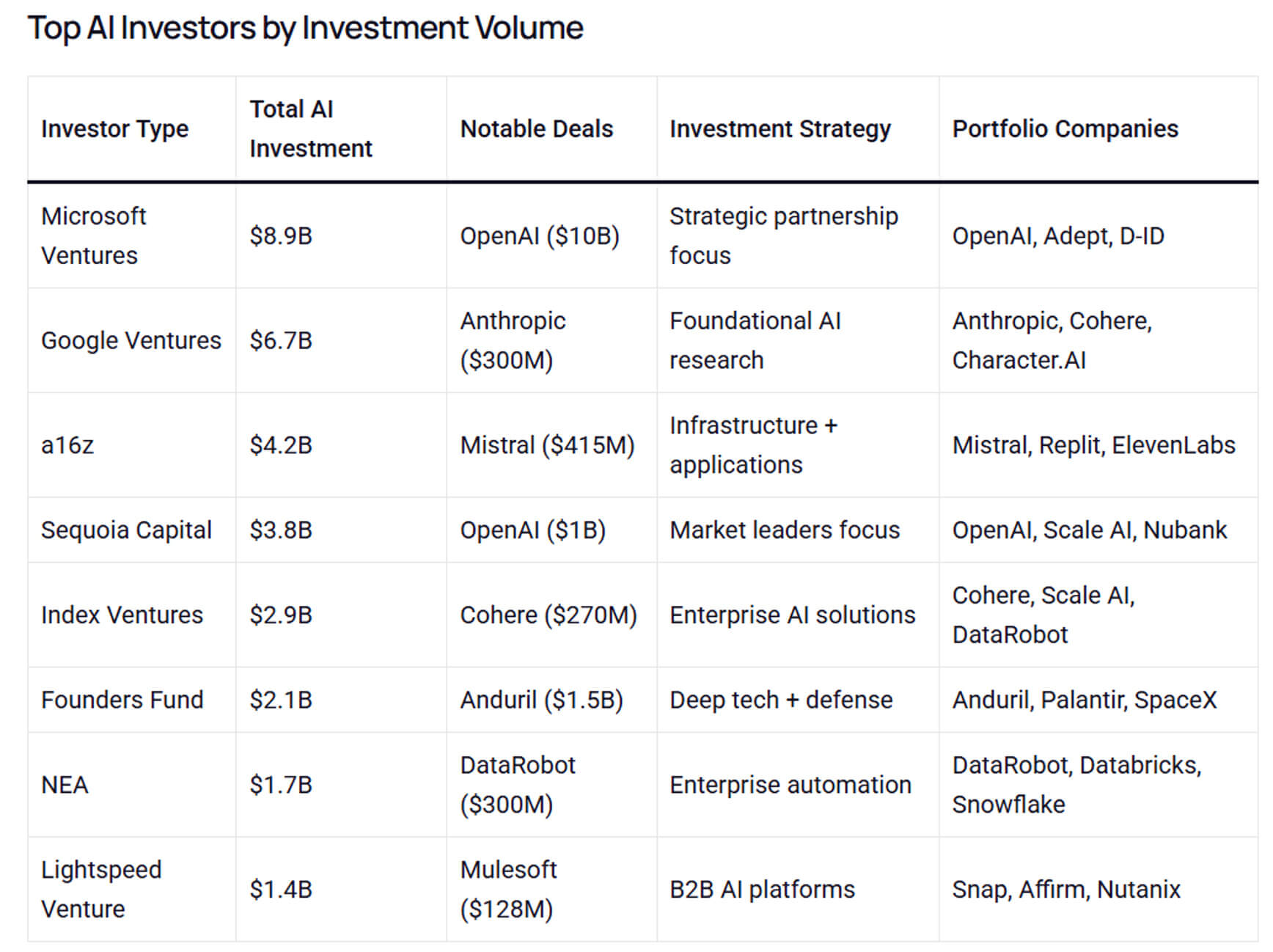

Trends and investments in artificial intelligence

In 2025, the global artificial intelligence market, including hardware, software, and services, is estimated at $391 billion, and by 2030, it could grow to $1.81 trillion.Corporate investment in the AI sector in 2024 amounted to $252.3 billion, a record high. Private investment during the same period amounted to $109.1 billion.

According to McKinsey & Company, nearly 92% of executives at companies investing in AI expect spending on these technologies to increase over the next three years.

Venture capital interest in artificial intelligence is growing, with analytical reports citing figures of $60-80 billion in capital raised for the development of American startups. Leading technology companies such as Microsoft, Google/Alphabet, Amazon, Meta, and OpenAI continue to allocate approximately 15-25% of their research budgets to fundamental AI, model development, and infrastructure (computing power, graphics processors/tester processors, specialized chips).

Key trends driving investment in artificial intelligence development:

- the use of API-based platform solutions and the provision of AI as a full-fledged service;

- the specialization of artificial intelligence in specific areas and spheres of life;

- peripheral AI and local intelligence;

- sustainable development, energy efficiency, and model compression.

The future of AI

Looking ahead to 2026 and the near future, several key scenarios can be identified for the impact of AI on business, society, and technological progress. The most powerful factor is the provision of deep autonomy through the use of agent systems, as well as the introduction of generative and language models for close communication with humans.When talking about the future development of artificial intelligence, we can identify the following important trends:

- increased autonomy and decision-making efficiency;

- more powerful fundamental models;

- industry changes and deep specialization;

- synergy between humans and AI, trust and controllability;

- impact on the economy and the workforce.

Gartner predicts that by the end of 2022, 70% of organizations will be using AI, designed to operate autonomously. This is an important milestone, indicating that agent systems are moving from cutting-edge to mainstream. In addition, small domain-specific models (SLM) are expected to play a more important role than before in agent systems themselves, thanks to their efficiency, cost, and specialization in many repetitive agent tasks.

Measuring AI Success

Artificial intelligence is actively transitioning from pilot projects to mission-critical systems, making the question of how to measure its success one of the most important strategic challenges. In the US and Europe, various metrics are used that reflect not only the accuracy of models, but also their impact on business, efficiency, trust, and long-term value.More details about each of them:

- technical metrics (AI model performance metrics) – accuracy, reliability, completeness, F1 score (for classification tasks), BLEU / ROUGE / METEOR indices (for generation, translation, and summarization), perplexity or cross-entropy measurement (for language modeling), latency, throughput, computational cost (efficiency metrics), as well as balance indicators on standard test sets (MMMU, GPQA, SWE-bench, MMLU, HumanEval, etc.);

- adoption, usage, and effectiveness metrics – number of actions/adoptions, time/cost savings, and productivity gains; workflow consistency and error correction speed; depth of adoption or retention;

- business and financial impact metrics (ROI, value realization, normalized cost of AI (LCOAI).

Today, a multidimensional metric is being actively implemented in practice, combining four axes of model evaluation:

- Technical performance;

- Ease of use and compliance with user requirements;

- Safety/reliability;

- Economic/commercial value.

This approach helps to bridge the gap between ideal benchmarks and the complex, iterative interaction between humans and AI in practice.

Global prospects for AI development

The use of AI varies across different regions of the world, depending on the specifics of infrastructure, regulation, investment prospects, and human resources. Europe and the US are leading the global AI market, creating high competitive pressure.Goldman Sachs experts predict, that by the end of 2025, global investment in AI could reach $200 billion, with the US accounting for almost half of that.

The United States is a major player in AI funding, R&D, and infrastructure development. The public and private sector budget for investment in artificial intelligence is expected to exceed $470.9 billion.

The UK with a share of £21 billion is the leader in AI development in the European market. Italy ranks second, showing active growth in the AI sector. Over the past year, the market volume has increased by approximately 58%, reaching €1.2 billion.

According to the study «Attitudes toward AI adoption and risks in 2025» many company executives around the world believe that artificial intelligence is used in customer service (36%), document summarization (35%), and email composition (32%).

In their survey, «AI Agents 2025» PwC experts note that 88% of senior executives say they plan to increase their AI budgets over the next 12 months.

BCG study indicates that executives around the world cite AI as a top strategic priority and emphasize the transition from experimentation to measurable results.

Key factors accelerating the globalization of AI:

- Growing investment in infrastructure and computing power.

- Development of regulatory frameworks and governance.

- Utilization of talented professionals and human capital.

- Industry specialization and increased competition in regions.

Education and training in AI

The success of the new wave of automation using AI technologies will be determined by the quality of education and professional training. Therefore, the priority tasks for companies are to improve digital literacy in the field of AI and to develop in-depth technical skills among employees.

Demand for courses on generative artificial intelligence is growing every day. For example, Coursera blog already has 700 courses in the Generative AI segment for the current year.

Analysis of data from the LinkedIn social network demonstrates the popularity of training within organizations. Thus, in 2025, AI training programs will be increasingly held in 32% of cases.

According to Microsoft's «AI in Education 2025», 86% of educational companies use generative artificial intelligence.

Research conducted by McKinsey and WEF shows that half of company employees will need AI skills in the next two years, which is encouraging employers to allocate budgets for training and retraining their staff.

In 2025-2026, the main areas of training will be as follows:

- basic AI literacy for all company employees – how to use assistants (co-pilots) safely and effectively, recognize errors/hallucinations, and act within the framework of corporate policy;

- development of applied skills for narrow specialists – working with content generation tools, business process automation, prompt engineering, implementation of AI tools in everyday tasks (marketing, sales, support);

- developing deep technical competencies for engineers – machine learning, data preparation, MLOps, model optimization/quantization, data security and privacy, building training and deployment pipelines;

- soft skills and ethics – critical thinking, interpretation of AI results, ethics, regulatory requirements (especially important for Europe – GDPR + AI Act).

The main investors in AI education:

- Global giants such as Microsoft, Google, AWS, Meta are scaling up their training programs and offering free or paid certificates integrated into corporate cloud products, such as Copilot courses and Google AI Certificates;

- On educational platforms such as Coursera, edX, Udacity and corporate LMS systems, you can find many courses dedicated to GenAI, with micro-certificates issued (based on the results of a short training program of up to 12 weeks);

- European government and academic initiatives include retraining programs, subsidies for the development of AI courses at universities, etc.

In 2026, experts expect corporate budgets for staff retraining to increase. In addition, a growing number of employers will pay for short courses and certification to improve the effectiveness of employees in achieving their targets. Artificial intelligence will be integrated into university curricula as a separate subject.

AI workloads and the cloud

As artificial intelligence systems become increasingly ambitious by processing multimodal input data, outputting it in real time, orchestrating agents, and large pipelines that only work with output, the requirements for computing resources, scalability, flexibility, and cost management are rapidly increasing.In the US and Europe, cloud platforms have become indispensable solutions for companies to deploy, scale, and operate workloads.

Experts predict that by the end of 2025, the global cloud computing market will be valued at more than $912.8 billion, of which public cloud spending will account for up to $724 billion.

According to a Google Cloud study, nearly 98% of companies are actively exploring generative AI, and 39% are already using it in a production environment, demonstrating an active transition from pilot projects to real-world systems.

According to MarketsandMarkets, the average annual growth rate of the AI market could reach 30-36% by the end of this decade. Today, the global artificial intelligence market is estimated at $390 billion.

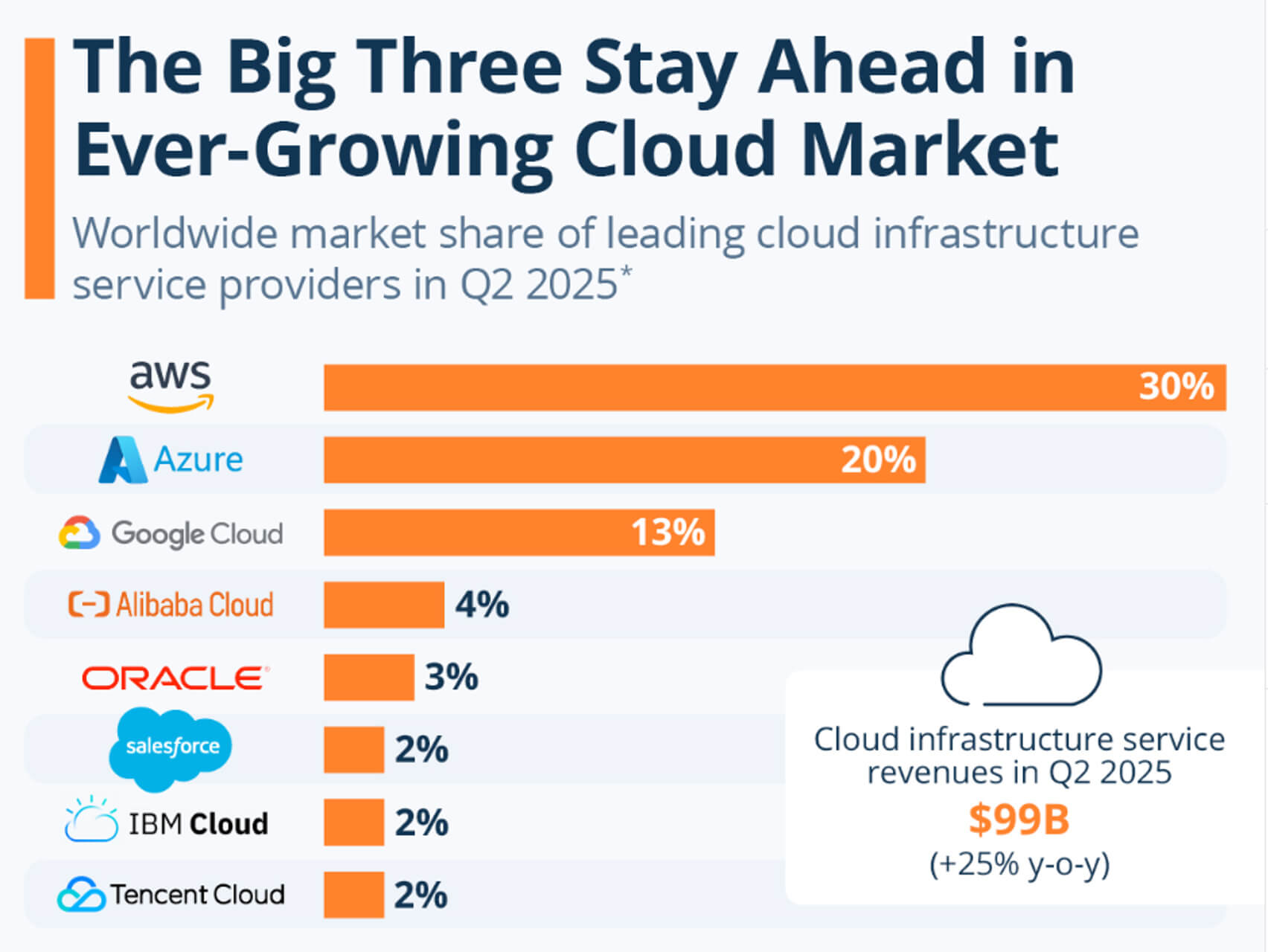

The three largest and most hyper-scalable operators in the world are AWS, Microsoft Azure, and Google Cloud, which already account for nearly 60% of the global cloud infrastructure market. As such, they influence where most corporate AI workloads are executed.

The key role of the cloud in artificial intelligence workloads is determined by the following factors:

- elasticity for peak training and inference loads;

- managed multi-tasking operations (MLOps) and end-to-end pipelines;

- access to specialized accelerators and stacks;

- global regions for compliance and data residency.

According to Google's «State of AI Infrastructure» report, there will be more managed agent services in 2026. Cloud solution providers will expand agent orchestration and security levels (policy control, audit logs) to support agent workloads in production environments.

Hybridization of edge and cloud solutions is becoming an increasingly popular approach. Real-time applications (AR/VR, automotive systems, industrial control systems) will use hybrid models: compact models on the device + a backup cloud for complex reasoning or updates.

AInvest experts believe that prices and agreements on dedicated graphics processor capacity will become more transparent. All companies will negotiate among themselves on dedicated graphics processor capacity and prices for the predictable cost of training models.

Transparency and trust in AI

As AI systems become more capable and autonomous, transparency, explainability, fairness, and accountability are becoming not just nice-to-haves, but fundamental requirements, especially in regulated markets (healthcare, finance, public administration) and in jurisdictions such as the US and Europe, where users, regulators, and stakeholders demand clarity. The focus is now on developing tools, standards, metrics, and practices that will ensure the reliability of AI in the real world.Examples of AI use in subject areas where transparency is paramount:

- Healthcare (clinical decision support) – physicians need explanations to understand and trust the model's results. Transparent AI helps to obtain regulatory approval (FDA, EMA) and make decisions about implementation;

- financial and credit scoring – lending decisions are regulated: applicants who are denied credit must be provided with explanations. Interpretability tools help solve the problem of biased lending;

- public sector (government and justice) – use in predictions (e.g., recidivism, resource allocation) requires full transparency to prevent unfairness and ensure oversight and auditability;

- recruitment and human resources management systems – AI tools for recruitment or performance evaluation should provide explanations to avoid accusations of discrimination and strengthen employee trust.

The EU AI Act, adopted in 2024 and phased in between 2025 and 2026, requires providers of high-risk AI systems to implement robust transparency and explainability mechanisms. Gartner estimates that by 2026, 70% of AI projects in Europe will include clear requirements for governance and auditing.

By 2026, transparency and trust will cease to be regulatory factors and become competitive advantages. Organizations that are unable to demonstrate honesty, explainability, and accountability risk losing market access, especially in the EU. Conversely, companies that implement responsible AI systems will achieve higher adoption rates and consumer trust.